Author:@bobthedegen_、@samoyedscribes and@ahboyash

Compiled by: Deep Chao TechFlow

Introduction

The year 2025 was a milestone for the development of crypto cards, as they transitioned from a niche onboarding tool to an increasingly widely used payment instrument. Both in terms of deposits and spending, crypto cards demonstrated strong growth momentum this year, a trend driven by improvements in user experience, broader blockchain support, and increasing user acceptance of stablecoin-denominated spending.

This report provides an ecosystem-level overview of crypto card activity over the past two years (December 2023 to October 2025), focusing on the observable on-chain behavior of leading crypto card providers.

Executive Summary

- From Experimentation to Practical Application: In 2025, crypto cards moved from the experimental phase to practical application, showing sustained exponential growth trends in both deposits and spending.

- Deposits Dominate Spending: Stablecoins dominated deposit behavior, accounting for almost all collateral assets, further reinforcing a low-volatility spending model similar to debit cards.

- @Rain Card Usage Leads: The @Rain series of crypto cards led in usage rates, but most users still engaged in small-amount spending, indicating their primary use for everyday "top-of-wallet" behavior.

- Future Growth: This growth trend is expected to continue into 2026, with further development in profitability, interchange economics, and credit-related factors, moving beyond the singular goal of user acquisition.

Methodology and Scope

This report analyzes crypto card activity through verifiable on-chain data, prioritizing observable economic behavior over self-reported metrics.

- Card Coverage:

- Type 1 Cards: On-chain verifiable deposits and spending (e.g., Rain series cards, Gnosis Pay card, MetaMask card)

- Type 2 Cards: Only on-chain verifiable deposits (e.g., WireX card, RedotPay card, Holyheld card)

- Type 3 Cards: Cards issued by Centralized Exchanges (CEX) (e.g., Binance Card, Bybit Card, Nexo Card)→ Excluded from analysis due to limited data availability

- Analysis Methods:

- Deposit Analysis: Includes Type 1 and Type 2 cards to capture a broader picture of liquidity inflow.

- Spending Analysis: Limited to Type 1 cards, as their transaction behavior can be directly observed on-chain.

For wallet-native cards whose spending does not follow the traditional deposit process, their spending activity is treated as a deposit in the analysis to maintain consistency. Non-stablecoin balances are normalized using the average price over the past 12 months, and all transaction volumes are expressed in USD equivalent.

Deposits: How Liquidity Enters the System

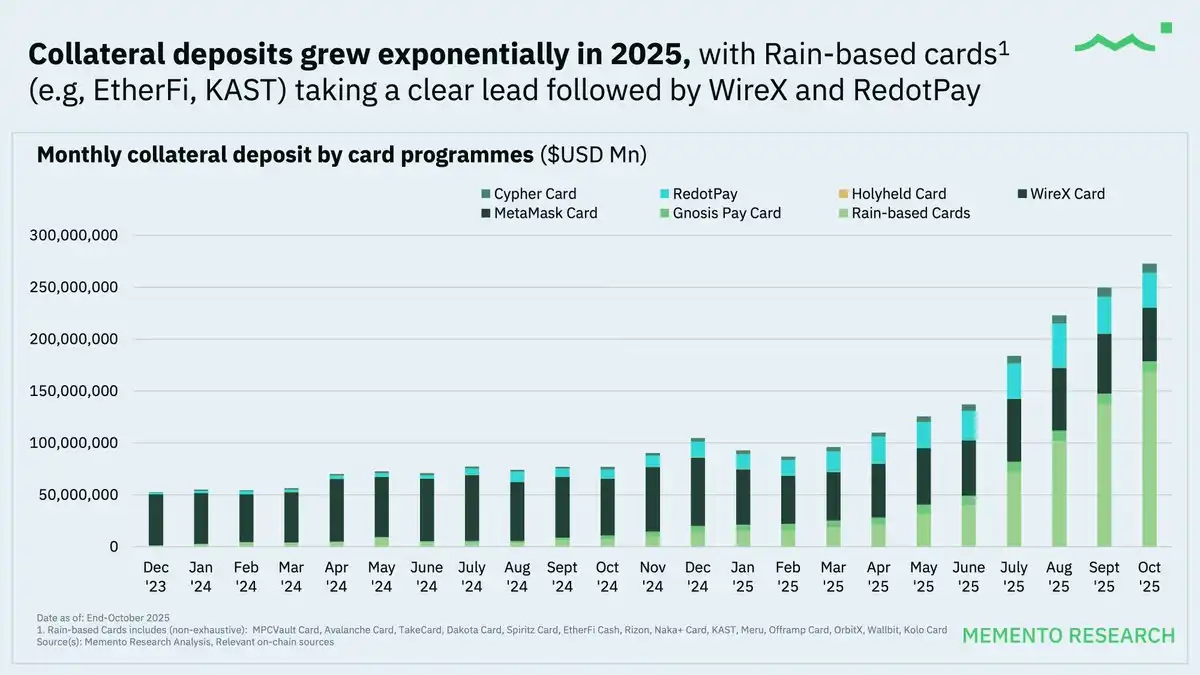

Deposits Expand First, Show Fastest Growth

Monthly collateral deposit volume for crypto cards grew exponentially throughout 2024 and accelerated further in 2025.

Card projects based on the Rain series of crypto cards consistently maintained a leading position in deposit volume, as they serve as the core infrastructure for multiple popular crypto card projects, including @ether_fi Cash, @KASTxyz, @OfframpXYZ, and the Avalanche (@avax) card.

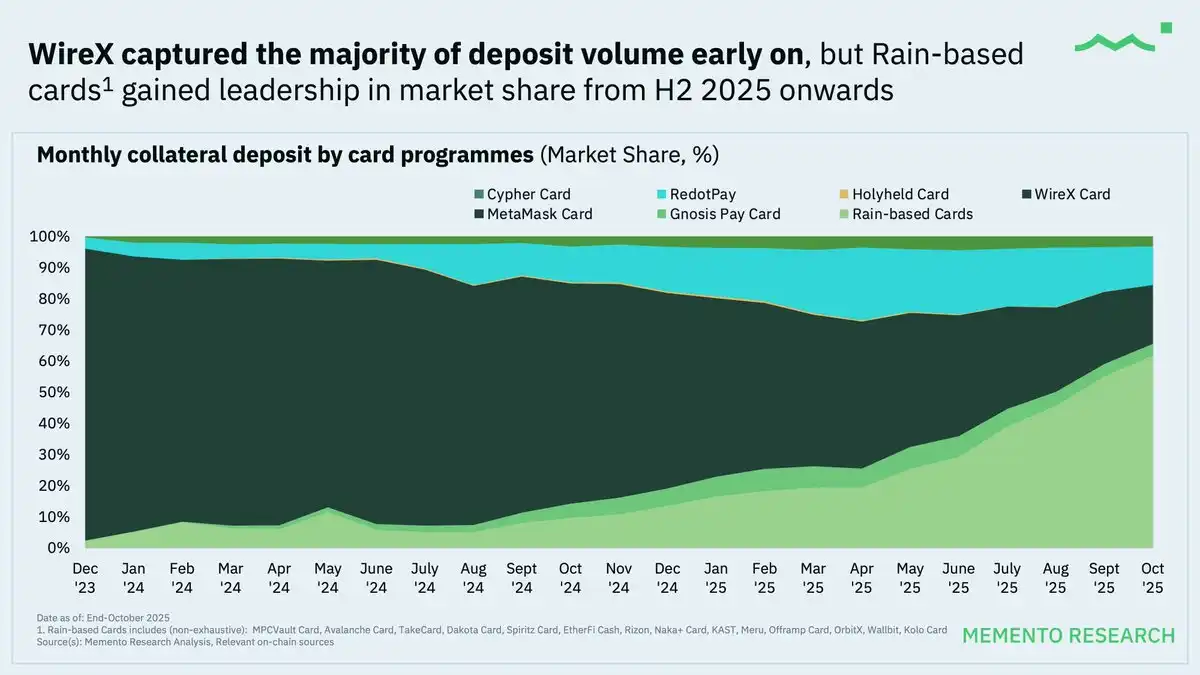

Market Share: First Concentrated, Then Diversified

@wirexapp held the majority share of deposit volume for most of 2024, but since the second half of 2025, the Rain series of crypto cards has taken the lead in market share.

Key Insight: Since the latter half of 2025, a wave of new crypto card projects has launched, choosing Rain as their core infrastructure partner. This trend has driven higher deposit inflows while accelerating new user onboarding.

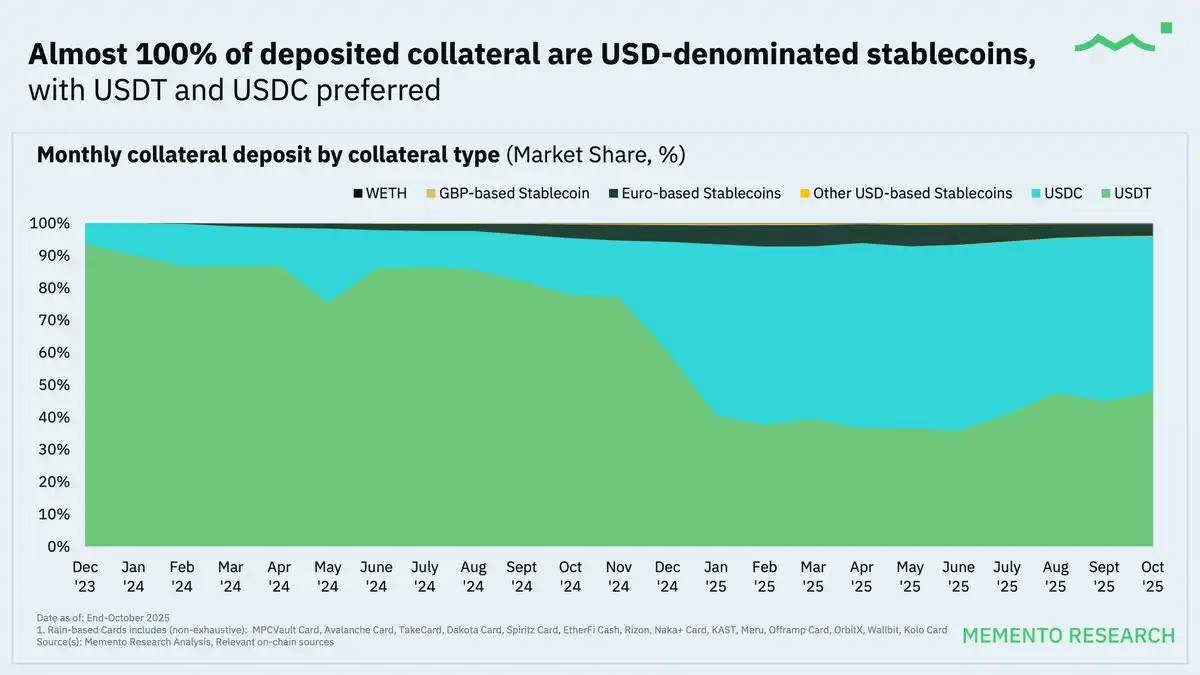

Stablecoins Dominate Almost Entirely

Throughout the dataset, almost 100% of deposit collateral assets consisted of USD-denominated stablecoins, with USDT and USDC as the main leaders.

This phenomenon further proves that current crypto cards are closer to international payment accounts rather than speculative spending tools, even for non-US users.

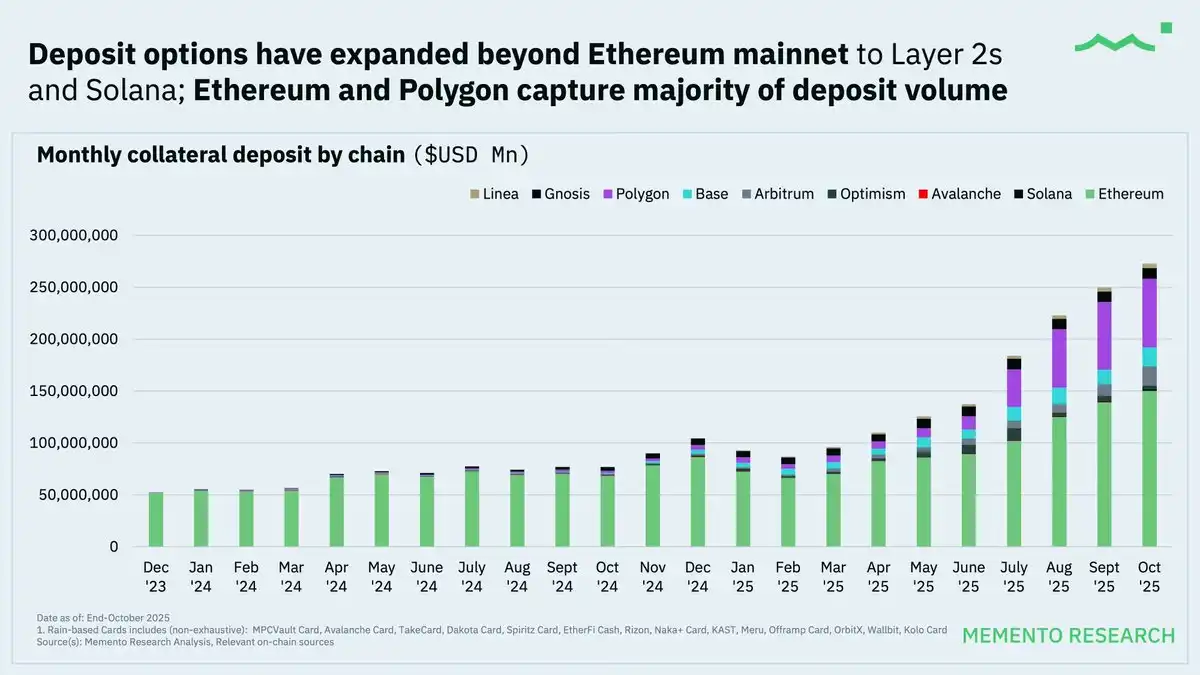

@ethereum and @0xPolygon are the Leading Deposit Chains, Multi-Chain Usage Gradually Rising

Although Ethereum (@ethereum) and Polygon (@0xPolygon) remain the primary deposit networks, other secondary chains (such as @base, @arbitrum, @Optimism, and @solana) are also steadily increasing their market share.

The rise of the multi-chain trend reflects the following factors:

- Lower Transaction Costs: Reduces the barrier for users to top up more frequently.

- Card Provider Route Optimization: Users are no longer forced to use a single chain; multi-chain deposits have gradually become a "basic feature."

Spending Behavior: How Crypto Cards Are Actually Used

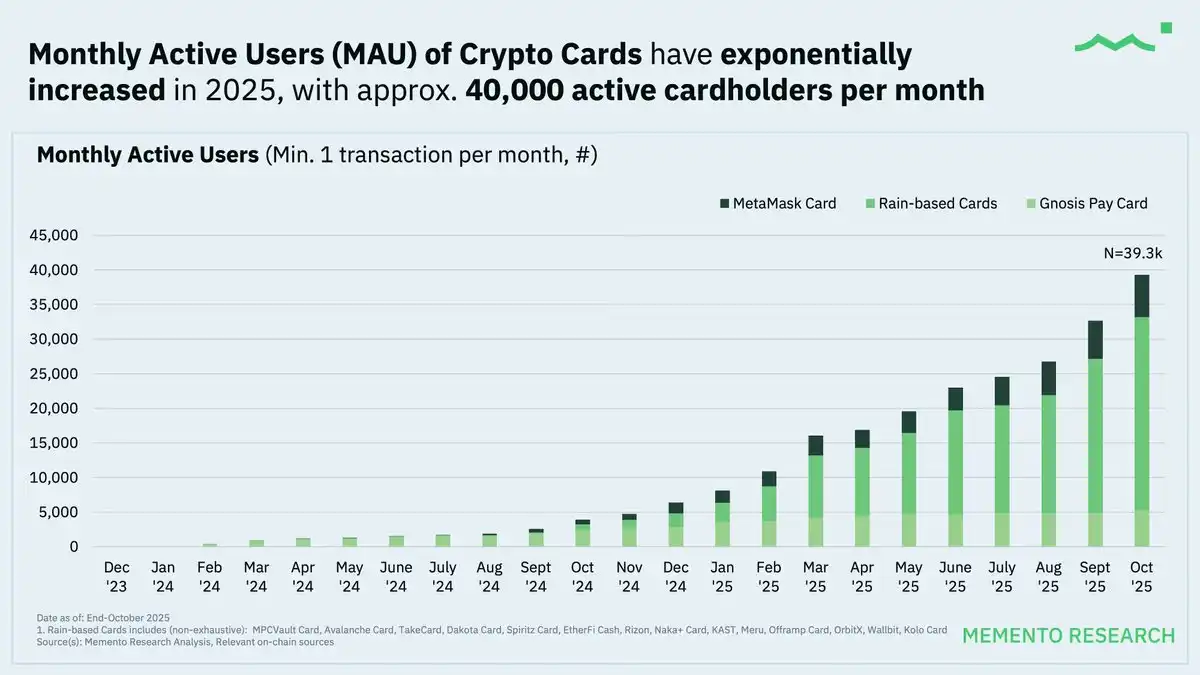

Monthly Active Users (MAU) Continued Rapid Growth in 2025

As of October 2025, the number of monthly active card users (MAU) has reached approximately 40,000, indicating rising user acceptance of crypto cards as a repeatedly used payment tool, rather than just a one-time experiment.

The crypto card industry is still in the early "user acquisition-driven" growth stage, suggesting the adoption curve is still in its infancy, with distribution and accessibility continually expanding.

The Rain series of cards, by virtue of their role as shared infrastructure (Card-as-a-Service) for multiple crypto card projects, accounts for the majority of transaction volume. Data from this Rain series is more suitable for interpretation at a trend level.

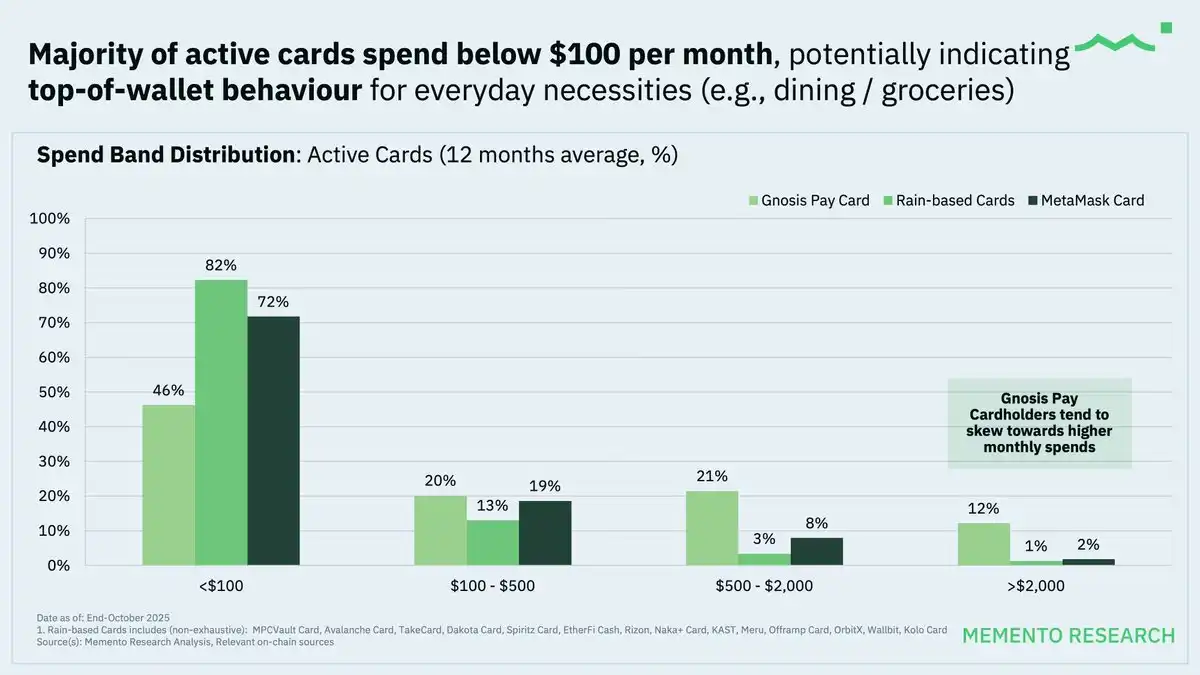

Spending amounts generally remain low, possibly indicating that crypto cards are primarily used for everyday expenses.

The low-value card usage pattern might also indicate users are utilizing crypto cards as an off-ramp tool for fiat withdrawal, directly bypassing the manual step of converting stablecoins to fiat.

Notably, @gnosispay cardholders show higher monthly spending amounts, suggesting their users are more inclined to use it as a primary payment card consistently.

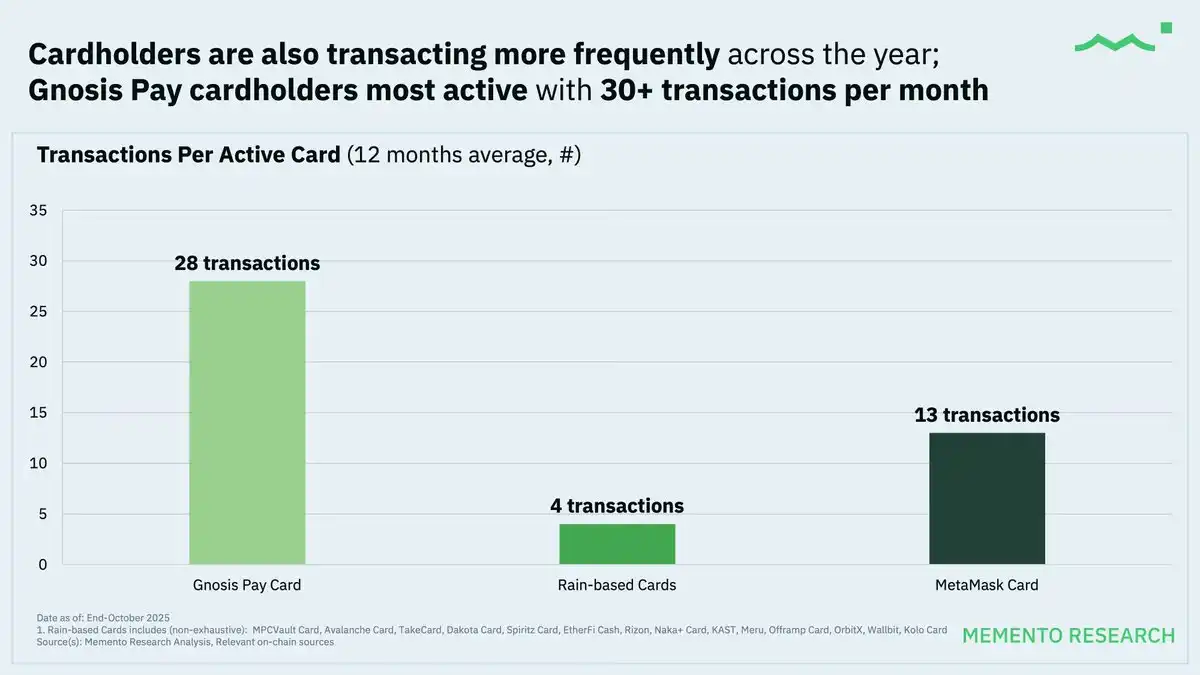

Over time, the transaction frequency of active cardholders has increased year-over-year; similar to spending patterns, @Gnosis Pay cardholders are the most active, with an average of over 30 transactions per month, fully reflecting daily payment behavior.

Key Insights

- Increasing User Activity: More people are genuinely starting to use crypto cards, not just registering, with spending and activity volumes rising steadily in 2025.

- Primarily Small Daily Expenses: Users rely more on stablecoins for small, routine expenses rather than large or speculative transactions.

- Core Role of Infrastructure Providers: Shared "Card-as-a-Service" models drive the concentration of transaction volume and dictate how the ecosystem expands.

Outlook for 2026: From Experimentation to Sustainable Scaling

Data from 2025 indicates that crypto cards have moved from the experimental phase into early adoption. Although deposits, spending, and active usage saw significant growth, user behavior remains cautious, resembling a stablecoin-centric prepaid card model rather than a full replacement for traditional credit cards.

Currently, crypto cards primarily serve as a bridge between on-chain liquidity and real-world payments, not as a complete substitute for traditional credit cards.

Looking ahead to 2026, growth is expected to be driven more by economic sustainability and product design, rather than relying solely on user acquisition momentum. As usage scales, card providers will need to balance expansion, the interchange economics of cross-border and domestic traffic, routing efficiency, and increasingly complex operational management.

Key Issues to Note:

- Privacy Concerns Persist: Transaction records are public on-chain, potentially exposing spending behavior. Once addresses are clustered or linked to centralized exchange deposit addresses, tracing ownership becomes easy based on on-chain behavioral traces (e.g., time, amount).

- The Double-Edged Sword of Public Data: Public data facilitates analysis but can also be exploited by competitors. Competitors can monitor traffic, mimic incentives, or even attack high-value users with predatory offers.

- Risks of Non-Vertical Integration: Most crypto card projects rely on issuers, payment processors, and a handful of "Card-as-a-Service" providers. This model can lead to single points of failure or be constrained by upstream compliance events or policy changes, causing sudden restrictions or shutdowns.

- High-Risk Merchant Categories: High-risk merchant categories like gaming, online casinos, and adult entertainment often face higher fraud and dispute/chargeback rates, potentially leading to stricter controls from card networks and issuers. Additionally, these categories may face harsher Anti-Money Laundering (AML) scrutiny in different jurisdictions.

- Homogenization Issue: Most crypto cards on the market currently offer similar core functionalities, with limited differentiation beyond selected cardholder rewards like cashback or points. Continued reliance on prepaid structures and a few Card-as-a-Service providers (like Rain) may pose long-term challenges for crypto card issuers seeking to compete with large traditional banks globally.

Future Trends to Watch:

- Expansion from prepaid models to credit card-related designs, similar to the @Coinbase One AMEX card.

- Stablecoins continue to dominate as the primary unit of account.

- Increased focus on profitability and unit economics as competition intensifies.

Crypto cards are gradually becoming foundational tools for embedded payments within wallets and applications. 2025 established market demand, and 2026 will determine which models can achieve sustainable scale.