Two of the most closely watched regulatory bodies in American finance are operating with skeleton crews. The Securities and Exchange Commission has three of its five commissioner seats filled — all by Republicans.

The Commodity Futures Trading Commission has just one sitting commissioner. Both vacancies come at a moment when the agencies are expected to take center stage in shaping the rules around digital assets, should a crypto market structure bill that has been stalled in the Senate since July 2025 finally pass.

A Nominee With Stakes In The Industry

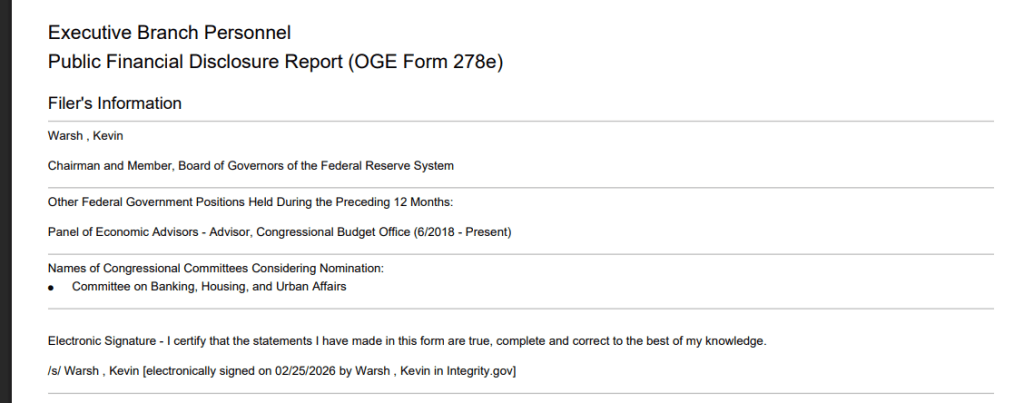

Against that backdrop, Kevin Warsh — US President Donald Trump’s pick to replace Federal Reserve Chair Jerome Powell — filed a financial disclosure last week that revealed personal investments in crypto and artificial intelligence companies.

Based on reports, Warsh’s filing with the US Office of Government Ethics lists holdings in Compound, Dapper Labs, and Kinetic on the crypto side, alongside AI firms including Delphi, Conversion, Factory, and Glue, among others.

Source: US Office of Government Ethics

His total disclosed assets top $100 million. The largest single entry is more than $50 million in something called the Juggernaut Fund. Another major line item: more than $10 million in consulting fees from the Duquesne Family Office, the investment firm run by billionaire Stanley Druckenmiller.

None of his crypto and AI investments included a value range in the disclosure. It is unclear why. The ethics office’s rules do not require reporting assets valued under $1,000, which may explain the omission — though the gap leaves open questions about the full scope of his exposure to sectors the Fed’s interest rate decisions directly affect.

BTCUSD trading at $73,929 on the 24-hour chart: TradingView

Powell’s Clock Is Running Out

Time is short. Powell’s second four-year term ends May 15. Trump first floated Warsh’s name in January, then formally sent his nomination to the Senate in March, following months of public pressure on Powell to cut interest rates. As of Tuesday, the Senate Banking Committee had not announced a hearing date, but reports indicated a vote could come as early as next week.

Whoever takes the Fed chair position wields enormous influence over US financial policy — most visibly through decisions on federal interest rates, which ripple through every corner of the economy, including the crypto and AI sectors where Warsh holds investments.

Featured image from Real Estate News, chart from TradingView