Author: Matt Hougan, Chief Investment Officer of Bitwise

Compiled by: Saoirse, Foresight News

The greatest excess returns (Alpha) in financial markets often come from behavioral biases. Investors always make mistakes, and if you can exploit these mistakes, you can achieve substantial returns.

One of my favorite behavioral biases to exploit is anchoring: people cling to the first piece of information they receive and are reluctant to change. This is why retailers price items at $9.99 instead of $10.00—you remember the '9' first, and your brain struggles to let go.

Anchoring was one of the reasons I decided to dive into the crypto industry full-time in 2018.

At that time, most people still viewed cryptocurrency as a joke. They first learned about it through the 2013 Silk Road scandal, the 2014 Mt. Gox exchange collapse, and witnessed its extreme boom-and-bust cycles.

Fortunately, a few people I trusted urged me to take crypto seriously.

When I looked beyond the surface, to see it for what it truly is rather than what people thought it was, I was completely astonished. The technology was far more mature than most people realized, and the opportunities were much greater. Yet people were still stuck with the old impressions from 2014.

Right now, I feel like I'm back in that moment.

The Whole World Is Shouting at You

Look around, Wall Street is loudly proclaiming: the financial industry is moving on-chain. Not just a small part, but all of it.

Last July, SEC Chairman Paul Atkins launched the 'Crypto Project,' a committee-wide initiative aimed at modernizing securities regulation. In his words, it's about enabling the U.S. financial markets to 'run on-chain.' And indeed, the markets have already started moving on-chain:

- In October, BlackRock CEO Larry Fink publicly stated that we are at the starting point of tokenizing all assets. Two weeks ago, BlackRock launched the BUIDL tokenized treasury fund on Uniswap, the world's largest decentralized exchange; it has already grown to over $2 billion in size. As part of the collaboration, BlackRock also invested in Uniswap's native token, UNI.

- Apollo, a credit institution managing $700 billion, partnered with Securitize to tokenize its diversified credit fund and list it on six public blockchains. Since January 2025, the product has attracted over $100 million. The company recently also announced plans to acquire a 9% stake in the leading global decentralized lending protocol, Morpho.

- JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo are in talks to jointly launch a stablecoin.

At the same time, JPMorgan issued a deposit token on Coinbase's Base network; Fidelity is hiring a head of decentralized finance treasury... Similar moves are emerging one after another.

The scale of the related markets is enormous: the ETF market is $30 trillion, the stock market is $110 trillion, and the bond market is $145 trillion.

In contrast, the current total global tokenized market is only $20 billion.

If Larry Fink is right—'every stock, every bond... will eventually be tokenized'—this means the market has tens of thousands of times more room to grow.

The Disconnect in Perception

Yet traditional investors just can't hear it.

They can't hear it because of anchoring.

When they think of cryptocurrency, the image that comes to mind is still that of the tattooed, punk, skateboarding figure. They don't realize that this person has long shaved his beard, put on a suit, and is building the infrastructure that will support the next generation of capital markets.

Amusingly, crypto investors themselves also seem unable to hear it.

They suffer from 'wolf cry' syndrome. Having heard promises of 'institutions are coming' for so long, now that they are actually here, they feel numb and unresponsive.

But the data doesn't lie.

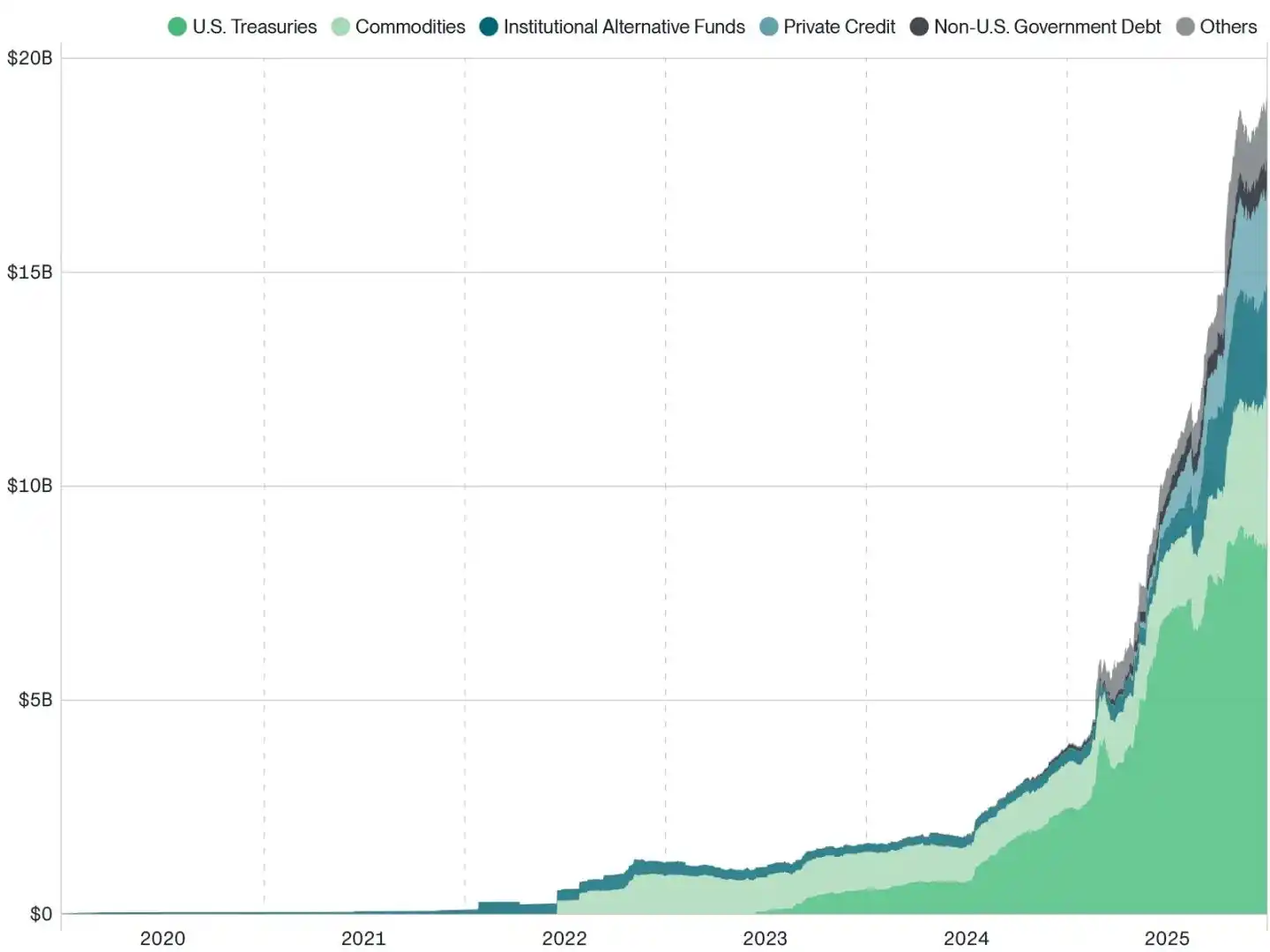

Look at the growth curve of tokenized real-world assets (RWAs)—it's as steep as Mount Everest.

Value of Tokenized Real-World Assets (RWAs):

Source: Bitwise Asset Management, data from RWA.xyz. Data timeframe is from January 1, 2020, to December 31, 2025.

Note: Stablecoin issuers like Circle and Tether are intentionally omitted.

Seizing the Opportunity

The challenge is that it's difficult to know precisely how to profit from this.

Because the crypto industry still has a series of key questions unanswered, such as:

- Will the value created by tokenization flow to underlying protocols like Ethereum and Solana, or is the underlying block space becoming commoditized?

- If value settles on the underlying public chains, will new quasi-private chains like Canton Network and Tempo outperform public chains?

- As institutions like BlackRock and Apollo embrace DeFi en masse, will DeFi tokens explode, or will the economic model challenges of DeFi tokens themselves be difficult to overcome?

- If the value ultimately flows to the builder companies rather than the blockchain itself, will the beneficiaries be traditional giants like BlackRock and JPMorgan, or crypto-native institutions?

I have my own judgments on these questions and will share them in articles over the coming months. But honestly, for most of these questions, the answer right now is: no one knows.

The only thing I am certain of is:

There is a huge gap between what people think the crypto market is and what the crypto market actually is.

In my view, this gap represents a major opportunity—not to rush to pick winners in advance, but to broadly position across the entire sector while the market is still mispricing this structural shift.

The greatest opportunities for alpha often arise when market consensus is outdated, reality has moved forward, and investors are still anchored to the old narrative.

The crypto industry is at that point right now.

If you can see it for what it is, opportunities abound.