Author: Bao Yilong

Investors are turning their eyes to Asia, searching for the next breakthrough in the global stock market rally.

Driven by the AI wave, South Korea's stock market led the world in gains this month, attracting a large influx of capital. The implied volatility in the options market has climbed to extreme levels, with derivatives strategists competing to recommend long structures.

All these signals point to the same conclusion: Asia's upward trend may have just begun.

According to Wind Trading Desk, Morgan Stanley's Asia-Pacific team has recently repeatedly emphasized that the underlying drivers of Asia's industrial cycle are shifting from traditional real estate and general manufacturing inventory replenishment to AI and its infrastructure, energy security and transition, defense, and supply chain resilience investments.

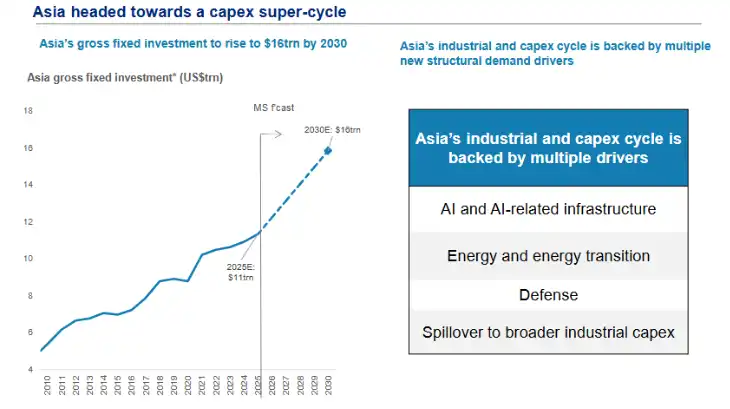

(Asia's total fixed investment is set to grow to $16 trillion by 2030)

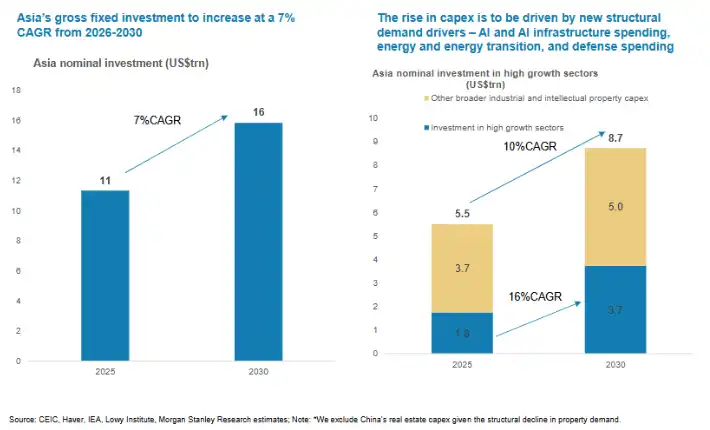

Morgan Stanley expects Asia's fixed asset investment scale to rise from about $11 trillion in 2025 to $16 trillion in 2030, with a nominal compound annual growth rate (CAGR) of about 7% from 2026 to 2030, significantly higher than recent levels.

(Asia's total fixed capital investment will maintain a 7% CAGR between 2026 and 2030)

The Underlying Logic of the 'Super Cycle': Asia's Capital Expenditure Is Set to Accelerate Significantly

The most core difference in this round of Asia's industrial cycle is that AI has pushed capital expenditure back to the forefront.

Over the past two years, market discussions on AI focused more on models, applications, and the US 'Magnificent Seven.' However, from an Asian perspective, the real meaning of AI is: the comprehensive expansion of chips, memory, servers, optical modules, data centers, power systems, and cloud infrastructure.

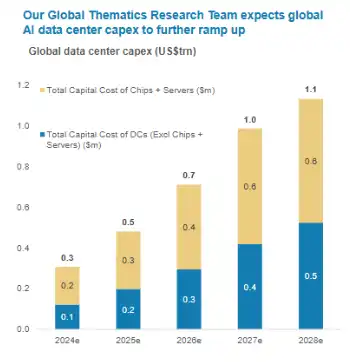

Morgan Stanley mentioned that the proportion of global CIOs listing AI as their top priority has risen to 39%. Correspondingly, global AI data center investment is expected to reach about $2.8 trillion from 2026 to 2028, with an annual growth rate of about 33%.

(Capital expenditure related to data centers in the global AI field will increase further)

Asia is at the center of the AI hardware supply chain: from TSMC, Samsung, SK Hynix to semiconductor, server, optical communication, and cloud infrastructure companies in Mainland China, all will benefit from this investment cycle.

The report also expects capital expenditure by major chip companies to potentially rise from about $105 billion in 2025 to about $250 billion annually by 2028. This means AI is a capital-intensive race.

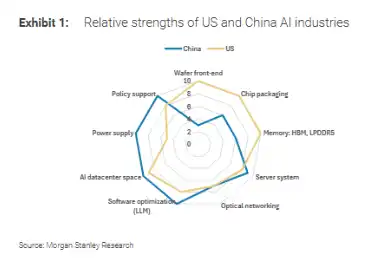

China's role is particularly noteworthy.

Morgan Stanley believes China's AI competition is about complete system capabilities: computing power determines speed, cloud platforms determine scale, token usage determines cost-effectiveness, and application scenarios determine value capture.

Amid ongoing external chip restrictions, the linkage between domestic AI chips, local cloud platforms, and the large model ecosystem is becoming a new investment theme in Chinese technology.

(The relative advantages of the AI industry in China and the US)

Their analysis shows that China's AI chip market could reach $67 billion by 2030, with domestic self-sufficiency potentially rising to 86%.

Whether this prediction materializes fully remains to be seen, but the direction is clear: domestic computing power has gradually shifted from a policy imperative to a commercial one.

The Export Story of 'Made in China' Is Expanding from the 'EV Trio' to Robotics

In recent years, the brightest spots in China's export structure were the 'new three'—electric vehicles, lithium batteries, and photovoltaic products.

The report suggests that the new growth driver for Chinese manufacturing in the next stage could come from robotics, especially industrial robots and humanoid robots.

Morgan Stanley points out that China has already captured about half of the incremental global demand for industrial robots. Global humanoid robot shipments in 2025 are estimated at about 13,000 to 16,000 units, with about 90% coming from Chinese manufacturers. In contrast, markets like the US and Japan remain more in the prototype or early validation stages.

More interestingly, the report draws an analogy between current Chinese robotics exports and electric vehicle exports around 2019: back then, EV exports hadn't entered an explosive growth phase, but the supply chain, policy support, and manufacturing capabilities were largely in place.

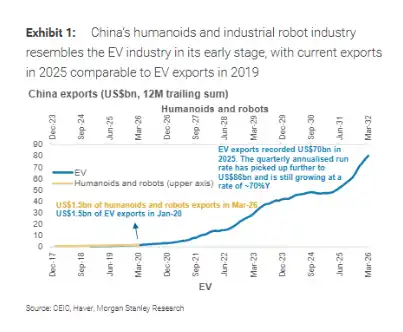

(China's humanoid and industrial robotics industry is at a development stage similar to the early phase of the electric vehicle industry)

Today, the robotics industry exhibits similar characteristics—the market size is still not large, but the industrial chain is expanding rapidly.

Looking at the data, China's 12-month rolling scale of humanoid robot and robotics-related exports reached about $1.5 billion in March 2026, similar to the level of Chinese EV exports in early 2020.

In the following years, EV exports expanded rapidly, reaching about $70 billion for the full year 2025, with the quarterly annualized run rate further rising to about $86 billion.

Of course, whether robotics can replicate the EV curve depends on cost reductions, application scenarios opening up, and overseas regulatory environments. But China's advantages in components, complete machine manufacturing, supply chain synergy, and rapid iteration are beginning to show.

Energy Security and Defense Spending Are Providing the Second and Third Growth Engines

The flip side of AI data center expansion is the enormous demand for power and energy infrastructure. The more intensive the computing power, the greater the importance of electricity, cooling, grid, and energy storage.

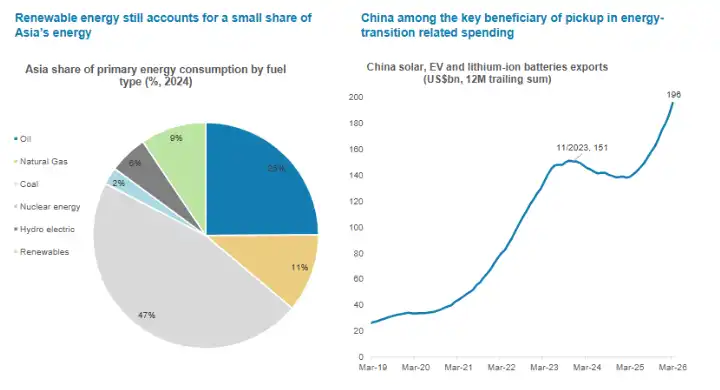

Morgan Stanley believes energy shocks will catalyze Asia's investment in energy security, and the share of renewable energy in Asia's primary energy consumption remains low, meaning significant room for subsequent investment.

(The proportion of renewable energy in Asia's energy mix remains small, and China benefits significantly from increased spending related to the energy transition)

China has industrial advantages in areas like photovoltaics, electric vehicles, and lithium batteries. The 12-month rolling scale of its related exports has approached the $200 billion level, making it a key beneficiary in this round of energy transition capital expenditure.

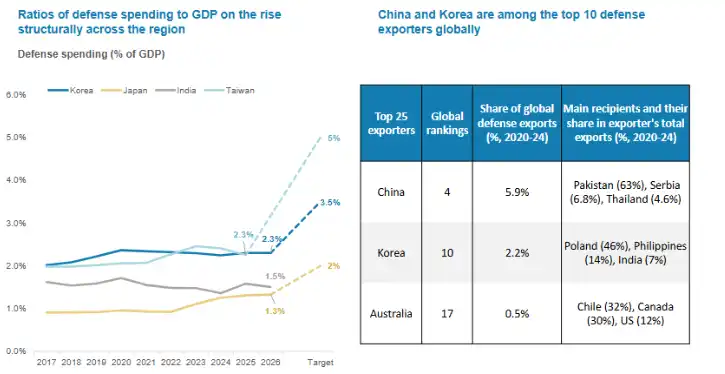

Meanwhile, defense spending is also showing a structural upward trend in multiple Asian economies.

The share of defense expenditure in GDP has risen in Japan, South Korea, India, and other places. China and South Korea are also among the world's top ten defense exporters.

(Across the region, the ratio of defense spending to GDP is trending upward)

For capital markets, this means that demand in industrial chains like high-end manufacturing, materials, electronic components, and precision equipment may receive longer-term support.

In other words, AI provides computing power demand, energy provides infrastructure constraints, and defense and supply chain security provide 'resilience investment' under the backdrop of geopolitics. The combination of the three constitutes the foundation of Asia's super cycle.

Who Benefits Most? China, South Korea, and Japan Are at the Core of the Value Chain

In terms of regional beneficiary order, Morgan Stanley highlights China, South Korea, and Japan.

Mainland China excels in industrial chain completeness, manufacturing scale, engineering capabilities, and emerging export categories like new energy and robotics.

South Korea holds advantages in memory, HBM, batteries, and some equipment materials; Japan still possesses deep accumulation in semiconductor equipment, materials, precision manufacturing, and industrial automation.

The proportion of capital goods exports also illustrates the point. The report shows: Thailand ~38%, China ~36%, Japan ~35%, South Korea ~30%. This means that when the global economy enters a new round of equipment investment cycles, the external demand elasticity of these economies will be more pronounced.

Finally, from a capital market structure perspective, these markets have higher weightings in industrial, tech hardware, and materials-related sectors, making it easier for macro capital expenditure cycles to be reflected in stock market performance.

This also means the pricing logic of Asian markets may change in the coming years, focusing on which companies in the capital expenditure chain have orders, technological barriers, and profit elasticity.

Risks That Cannot Be Ignored: Overcapacity, Profit Margins, and Geopolitical Friction

The super cycle narrative is attractive but does not mean all industries and companies will benefit simultaneously.

First, capital expenditure expansion may bring temporary supply pressure.

China's new energy industry has proven that scale advantages can quickly open global markets but may also be accompanied by price competition and profit margin volatility. Industries like robotics, AI hardware, photovoltaics, and energy storage may face similar issues in the future.

Second, technology restrictions and export controls remain variables.

The space for AI chip localization is vast, but gaps still exist in advanced process nodes, HBM, EDA, equipment, and materials. The report also notes that while there is still a gap between domestic chips and top-tier US chips, competitiveness can be enhanced through system optimization, advanced packaging, and software adaptation.

Third, employment structures will also be affected by AI.

Morgan Stanley's 'Future of Work' research estimates that about 90% of occupations will be affected to varying degrees by AI automation and augmentation. In its sample of companies, early AI adoption has brought over 11% productivity gains but also accompanied an average net job reduction of about 4%, with significant differences across countries and industries.

For China, advancing retraining and job transitions while improving efficiency will be a crucial medium- to long-term policy and corporate management challenge.

Fourth, market volatility may increase. The report also cautions that the widening gap between bull and bear scenarios in regional markets means investor divergence over expectations for AI capital expenditure, export orders, and profit realization will persist.