Author: Robert Hackett

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: According to data from the a16z Crypto brief, weekly trading volume in prediction markets surpassed $14.4 billion for the first time last week, setting a new all-time high for the third consecutive week. At the beginning of the year, this figure was only around $5-6 billion. Even more noteworthy is the non-sports category—covering politics, economics, geopolitics—which reached $3.6 billion in a single week, exceeding the total weekly volume (including sports) for the entire market last year. While the World Cup has driven attention and funds, the growth has long extended beyond sports betting.

Last week, weekly trading volume in prediction markets surged to $14.4 billion for the first time. At the start of the year, this number was still around $5-6 billion. The previous all-time high (approximately $10 billion) was set just a week prior.

Aggregated across all platforms, current trading volume is over 10 times higher than it was a year ago.

Caption: Trend of weekly trading volume in prediction markets, reaching $14.4 billion last week, compared to around $5-6 billion at the start of the year.

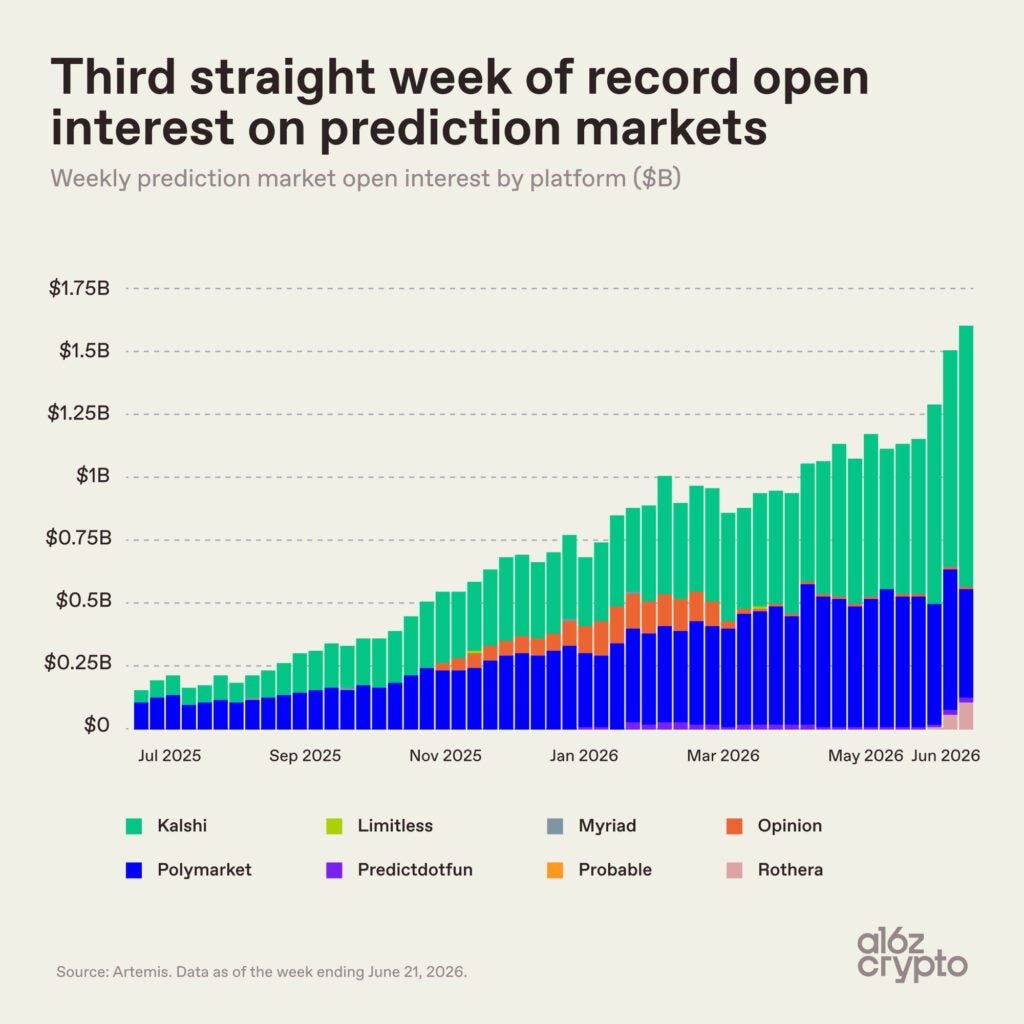

Open interest (the total value of unsettled positions) reached $1.6 billion last week, setting a new weekly record for the third consecutive week.

Unlike trading volume, open interest only increases when the rate of new positions being opened outpaces the settlement of old ones. Therefore, an upward trend in this curve indicates that more real money is being committed to these markets.

Since last fall, this curve has been steadily climbing. During this period, open interest has increased approximately eightfold, rising from less than $200 million to $1.6 billion.

Caption: Open interest has grown about 8 times since last fall, increasing from under $200 million to $1.6 billion.

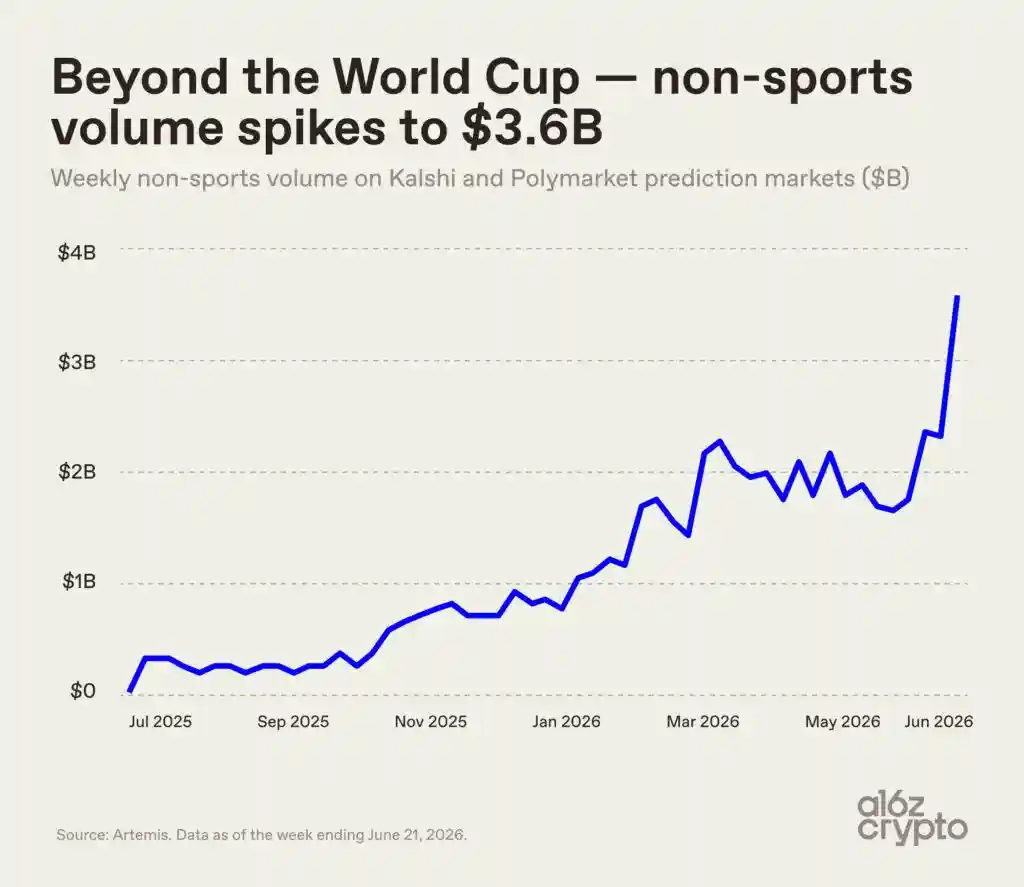

While the World Cup has absorbed significant attention and capital, other sectors have also risen alongside it. Non-sports trading volume—encompassing categories like politics, economics, geopolitics, and current events—reached $3.6 billion last week combined on the Kalshi and Polymarket platforms. This figure is larger than the total weekly volume for the entire prediction market (including sports) last year.

In July 2025, weekly non-sports trading volume was only around $200 million. It has since grown approximately 18-fold, with the slope of the curve noticeably steepening this month.

Acknowledgments: Data and charts provided by Ryan Holloway and Robert Hackett (a16z crypto special feature editor and head of special projects).