Original Title:Game Theory on Polymarket: The 5 Formulas tested on 72 million trades,Author:Movez(@0xMovez)

Compiled|Odaily Planet Daily(@OdailyChina);Translator|Asher(@Asher_ 0210)

On the Las Vegas Strip, the average return rate of slot machines is about 93%, meaning for every dollar invested, you only get back an average of $0.93; on Polymarket, however, traders voluntarily accept returns as low as $0.43, using $1 to bet on outcomes with odds even worse than those in a casino.

This is not a metaphor, but based on real data. Researcher Jonathan Becker analyzed all settled markets on Kalshi, covering 72.1 million trades with a total volume of $18.26 billion. The patterns he discovered also apply to Polymarket—same mechanisms, same biases, meaning the same opportunities. The data's conclusion is straightforward: approximately 87% of prediction market wallets end up losing money, but the remaining 13% don't win by luck; they master a set of mathematical methods that most traders aren't even aware of.

This article will break down the 5 game theory formulas that separate the winners from the losers, each accompanied by its mathematical principle, real-world examples, and runnable Python code. Some traders already applying these methods in practice include:

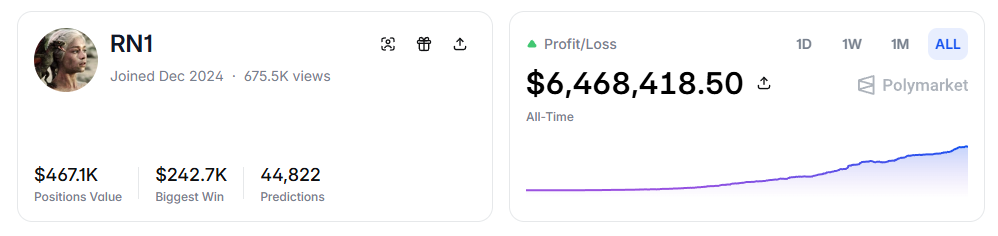

- RN(Polymarket address:https://polymarket.com/profile/%40rn1): A Polymarket algorithmic trading bot that has achieved over $6 million in total profit in sports markets using the models described here.

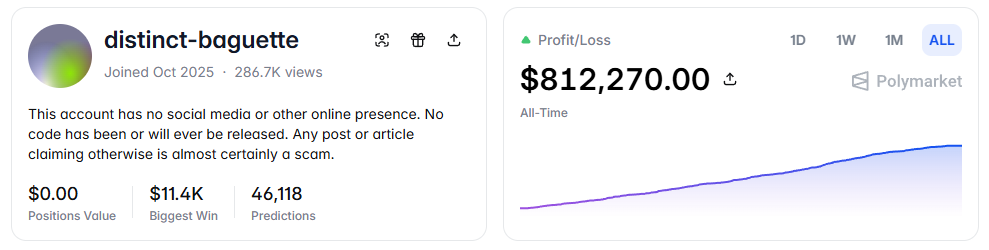

- distinct-baguette(Polymarket address:https://polymarket.com/profile/%40distinct-baguette): Turned $560 into $812,000 through market making in UP/DOWN markets.

I. Expected Value: The Core Formula

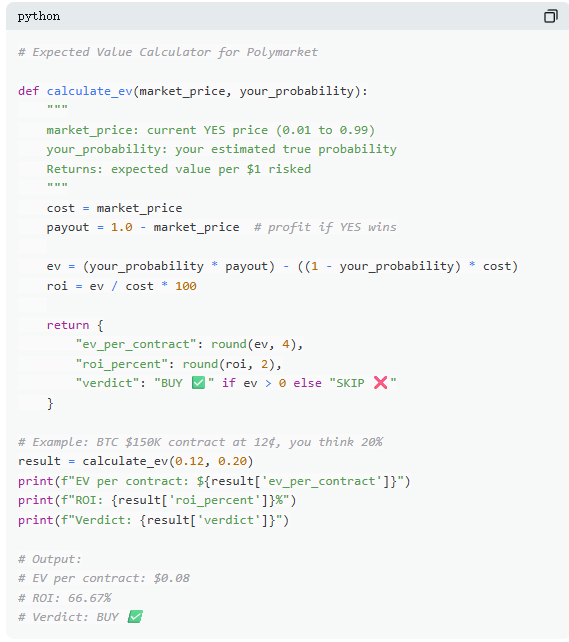

On Polymarket, every trade is essentially a judgment of expected value. Most traders rely on intuition, while the 13% of winners use mathematics to make decisions. Expected Value (EV) measures not a single outcome, but the average return over many repetitions, used to judge whether a trade is worth making.

Take a real market as an example: "Will Bitcoin reach $150,000 before June 2026?" The current YES price is 12¢, implying a market probability of 12%. If, based on on-chain data, halving cycles, and ETF flows, you judge the true probability to be around 20%, then this trade has positive expected value. Calculated this way, each contract bought at 12¢ can yield an average profit of 8¢ in the long run; buying 100 contracts, costing $12, has an expected profit of $8, a return rate of approximately +66.7%.

But the data shows that most prediction market traders do not perform such calculations. In a sample covering 72 million trades, takers (those who market buy) lost an average of about 1.12% per trade, while makers (those who place limit orders) profited an average of about 1.12% per trade. The difference between them lies not in information, but in patience—makers wait for positive EV opportunities, while takers are more prone to impulsive trading.

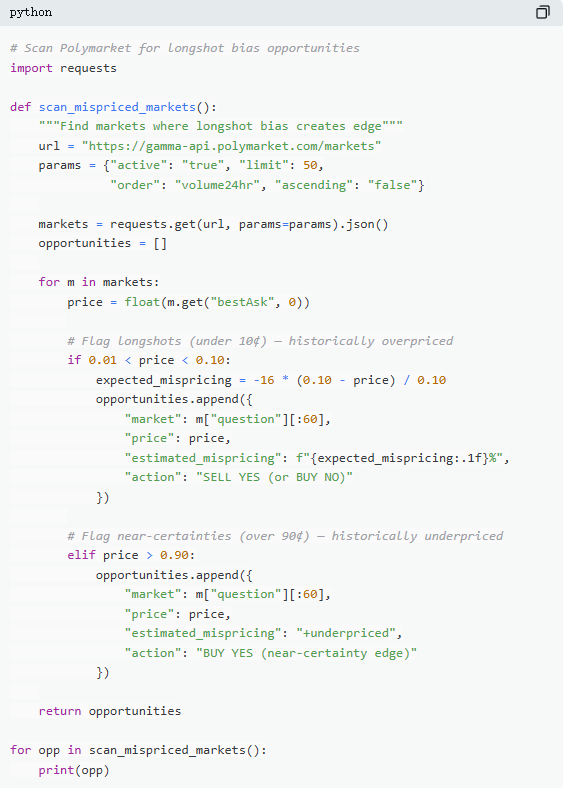

II. Mispricing: The Low-Price Contract Trap

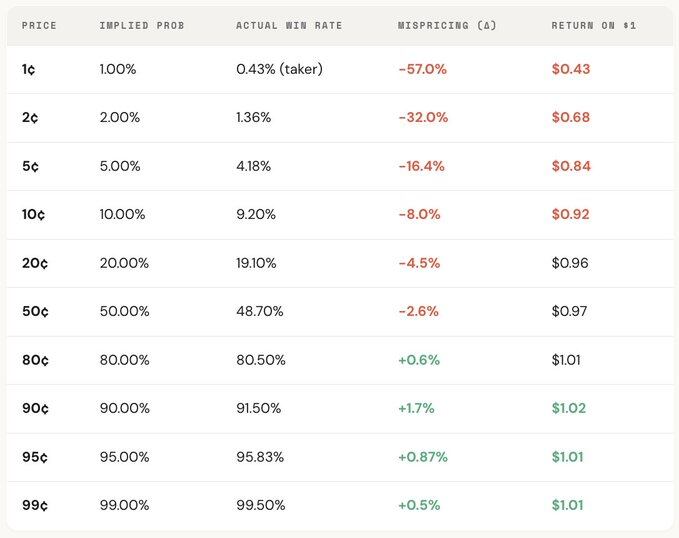

"Long-shot bias" is one of the most expensive mistakes in prediction markets. Traders systematically overestimate low-probability events, paying too high a price for seemingly cheap contracts. A contract priced at 5¢ should theoretically have a 5% win rate, but on Kalshi the actual win rate is only 4.18%, a pricing deviation of -16.36%; in more extreme cases, a 1¢ contract should have a 1% win rate, but for takers, the actual win rate is only 0.43%, a deviation of -57%.

Looking at the overall distribution, the market is relatively accurate in the middle range (30¢–70¢), but shows significant deviations at the extremes: contracts below 20¢ generally have actual win rates lower than their implied probability; contracts above 80¢ often have win rates higher than their price-reflected probability.

In other words, market inefficiency is concentrated at the extremes, and these are precisely where emotional trading is most concentrated. Specifically, there are two formulas:

Formula 1: Mispricing (δ)

Mispricing measures the deviation between a contract's actual win rate and its implied probability. Taking the 5¢ contract as an example: across all settled markets, assume there were 100,000 trades executed at 5¢, of which 4,180 ultimately resulted in YES. The actual win rate is 4.18%, while the price implies a probability of 5.00%. The difference is -0.82 percentage points, a relative deviation of about -16.36%. This means that for every 5¢ contract bought, one is effectively paying a premium of about 16.36%.

Formula 2: Gross Excess Return per Trade (ri)

If mispricing reflects the overall bias, then the gross excess return per trade reveals the actual return structure of each individual trade, and it is here that behavioral biases become clear. When buying a 5¢ contract, two outcomes are possible: if the contract hits, the gain can be +1900% (~20x return); if it misses, the loss is 100%, the entire 5¢ invested is lost.

This is why the "long-shot bias" is so attractive—the potential for extremely high returns if it hits is easily remembered, amplified, and shared. But overall, its actual hit rate is lower than the probability implied by the price, and the asymmetric structure between "total loss" and "extremely high gain" creates negative expected value over many trades, essentially equivalent to buying an overpriced lottery ticket.

Looking at the overall distribution, this bias has a clear price gradient: the lower the price, the worse the return. For example, as a taker, for every $1 invested in 1¢ contracts, one gets back only about $0.43 on average; for 90¢ contracts, every $1 invested yields about $1.02 on average. The cheaper the price, the worse the actual trading conditions.

Further breaking down by role reveals an almost mirror-image relationship: the losses of takers in the low-price range (up to -57%) correspond almost exactly to the gains of makers in the same range; the overall market pricing bias lies between them. In other words, almost every cent lost by takers is gained by makers.

From a game theory perspective, low-probability contracts are systematically overestimated, while high-probability contracts are often underestimated. The real strategy is not to chase long shots, but to sell them and buy high certainty.

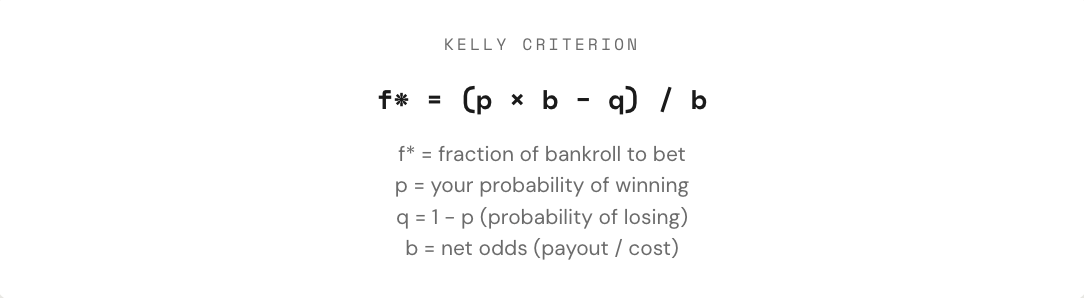

III. Kelly Criterion: How Much to Bet

When you find a trade with positive expected value, the real question just begins: how much should a trader bet? Bet too much, and one loss could wipe out weeks of gains; bet too little, and even with an edge, growth is too slow to be meaningful. Between "all-in" and "not betting at all," there is a mathematically optimal betting fraction: the Kelly Criterion.

The Kelly Criterion was proposed by John Kelly Jr. in 1956, initially to optimize signal-to-noise ratio in communications, but later proven to be one of the most effective position sizing methods in gambling, trading, and even prediction markets. Professional poker players, sports betting experts, and Wall Street quant funds almost all use some form of Kelly strategy.

In prediction markets, since contracts are binary (resulting in $1 or $0) and the price itself represents probability, the application of the Kelly Criterion is more direct. The key is understanding the odds (b): if you buy a YES contract for 30¢, you are essentially risking $0.30 to win $0.70, corresponding to odds of 0.70 / 0.30 ≈ 2.33; at a price of 50¢, the odds are 1; at 10¢, 9; at 80¢, only 0.25. The higher the odds, the larger the bet fraction Kelly suggests, assuming an edge exists.

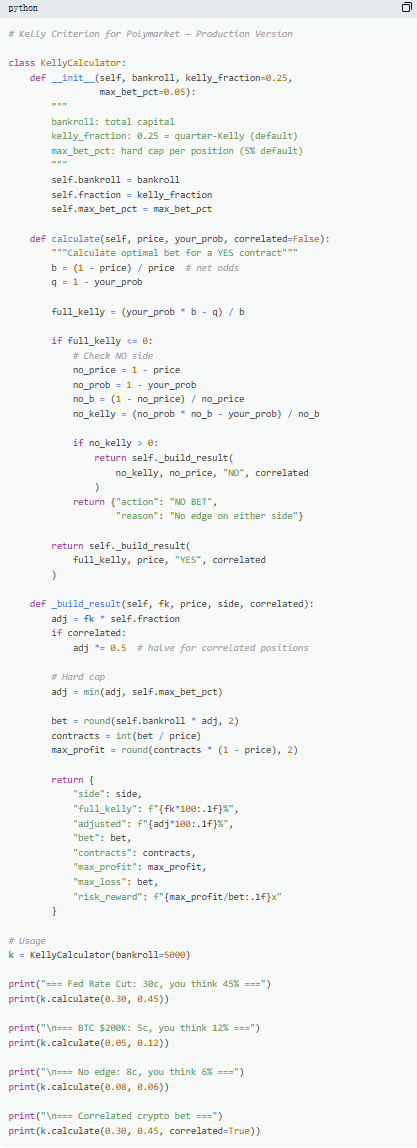

But a key principle is not to use full Kelly. While mathematically full Kelly maximizes long-term growth rate, in practice its volatility is extreme, with drawdowns often exceeding 50%. It might have the highest returns over a very long period, but the severe volatility along the way often makes it unsustainable for most people. Therefore, a more common practice is to use fractional Kelly (e.g., 1/2 or 1/4 Kelly). For example, under stable win rate conditions, full Kelly, while ultimately having the highest equity curve, is very volatile; 1/4 Kelly grows more smoothly with controllable drawdowns; 1/2 Kelly falls somewhere in between.

Essentially, the Kelly Criterion provides a framework of discipline: first determine if an edge exists (i.e., subjective probability is higher than market-implied probability), and then decide how much capital to allocate. Only when both "whether to bet" and "how much to bet" are constrained by rules does trading truly move from gambling to strategy.

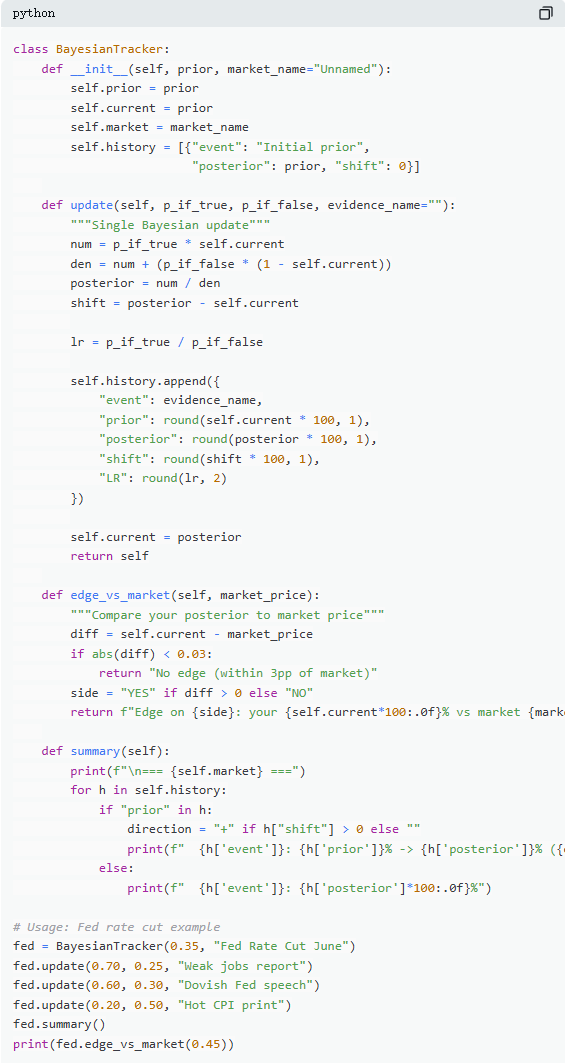

IV. Bayesian Updating: Changing Your Mind Like an Expert

Prediction markets fluctuate essentially because new information constantly arrives. The key is not whether the initial judgment was correct, but how to adjust beliefs when evidence changes. Most traders either ignore new information or overreact, while Bayesian updating provides a mathematical method for "how much adjustment is reasonable."

Its core logic can be simply understood as new judgment = degree of evidence support for the original hypothesis × original judgment ÷ overall probability of that evidence occurring. In practical application, it is usually expanded via the law of total probability into a more calculable form.

Take a typical market: "Will the Fed cut rates at the June meeting?" The current market price is 35¢, implying a 35% probability, serving as the initial judgment. Then the non-farm payroll data is released, showing only 120k new jobs (expected 200k), with rising unemployment and slowing wage growth. In this scenario, if the Fed is indeed going to cut rates, the probability of weak employment data is high, estimated at 70%; if it is not going to cut rates, the probability of such data is lower but still possible, estimated at 25%.

Substituting into Bayesian updating, the new probability is approximately 60.1%, meaning a one-time upward revision from 35% to 60.1%, an increase of about 25 percentage points. This shows that one key piece of information can significantly alter market judgment.

In practice, you don't need to calculate the full formula every time. A more common method is the "likelihood ratio." The same piece of information (e.g., LR = 3) has different impacts depending on the initial judgment: starting from 10%, it might increase to about 25%; from 50%, to 75%; from 90%, to only about 96%. The higher the uncertainty, the greater the impact of information.

The traders who consistently outperform in prediction markets long-term are not necessarily those who are most accurate initially, but those who can adjust their judgments the fastest and most reasonably when new evidence appears. The Bayesian method essentially provides the scale for this "speed of adjustment."

V. Nash Equilibrium: The "Poker Formula" in Prediction Markets

In poker, bluffing is never a gut decision, but a strategy that can be precisely calculated. Theoretically, there is an optimal bluffing frequency; once deviated, skilled opponents can exploit it. The same logic applies to prediction markets. On Polymarket, "bluffing" corresponds to contrarian trading—choosing to stand against the majority when market pricing is biased; while "folding" is akin to being a passive taker, continuously paying a premium for market sentiment.

On Polymarket, makers and takers form a similar adversarial relationship. Contrarian trading (against market consensus) is akin to "bluffing," while trend-following trading (following mainstream judgment) is akin to "value betting." From an equilibrium perspective, the market should make marginal participants indifferent between "being a maker" and "being a taker." This state corresponds to the Nash Equilibrium in prediction markets.

But this equilibrium is not fixed; it adjusts dynamically with changes in participant structure. Data shows that different market categories correspond to different optimal strategies: in areas with more rational information and efficient pricing (e.g., financial markets), the contrarian space is smaller; in areas with stronger emotions and more concentrated irrationality (e.g., entertainment, sports), the market is more prone to pricing biases, thus providing opportunities for contrarian trading.

More importantly, this equilibrium has changed significantly over time. In the early days (2021–2023), takers were actually the profitable group, and the optimal strategy leaned towards active taking. But after the trading volume explosion in Q4 2024, professional market makers entered in large numbers, the market structure changed, and the equilibrium strategy shifted towards being a maker (about 65%–70%). This is a typical result of game theory: when participant structure changes, the optimal strategy evolves accordingly. Strategies that were effective in a "novice environment" may quickly become ineffective against "professional opponents," and the market's "playbook" thus constantly iterates.

Summary

87% of prediction market wallets end up losing money, not because the market is manipulated, but because these traders never truly did the math. They buy long-shot contracts at prices than worse slot machines, decide position sizes by feel, ignore new information, and pay for "optimistic sentiment" with every market order.

The 13% who consistently profit are not luckier; they use these 5 formulas as a complete methodology, forming a full process from judgment to execution, with each step built upon 72.1 million real trades.

This window won't last forever. As professional market makers enter, bid-ask spreads are rapidly compressing. In 2022, takers still had an advantage of about +2.0%; now it has turned into -1.12%.

The only question is, will you evolve with the market, or continue buying $1 lottery tickets for a $0.43 return.