Author: CryptoSlate

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: ETF outflows, institutional wait-and-see, AI capturing investor attention... Bitcoin has grown too large to be moved by retail investors alone. CryptoQuant founder Ki Young Ju did the math: In 2011, $2.7 million could push BTC up 550 times; now, it takes $101 billion to double it. Whether the next bull market arrives depends on whether wealth advisors, corporate treasuries, banks, and sovereign funds are willing to treat BTC as a long-term allocation rather than a short-term trade.

Bitcoin's next major rally may no longer depend on whether investors believe in the asset, but on how much major capital is willing to participate with real money.

The latest analysis from CryptoQuant CEO Ki Young Ju shows that the world's largest cryptocurrency has matured into a market too large to be easily propelled as it was in early cycles. According to him, each bull cycle requires more capital to produce smaller percentage gains, a shift that raises the threshold for another parabolic rally.

This is particularly relevant now as BTC is in a prolonged bear market, having fallen to around $63,000, down 50% from the peak above $126,000 recorded last October.

This pullback tests the institutional adoption that helped push the asset into mainstream portfolios. The core question now is whether Bitcoin can attract enough persistent capital to offset its declining price sensitivity.

A Larger Market Changes the Cycle Math

Bitcoin's early rallies were built on a much smaller base, allowing small amounts of new money to produce massive price changes. This relationship has diminished as the asset has matured.

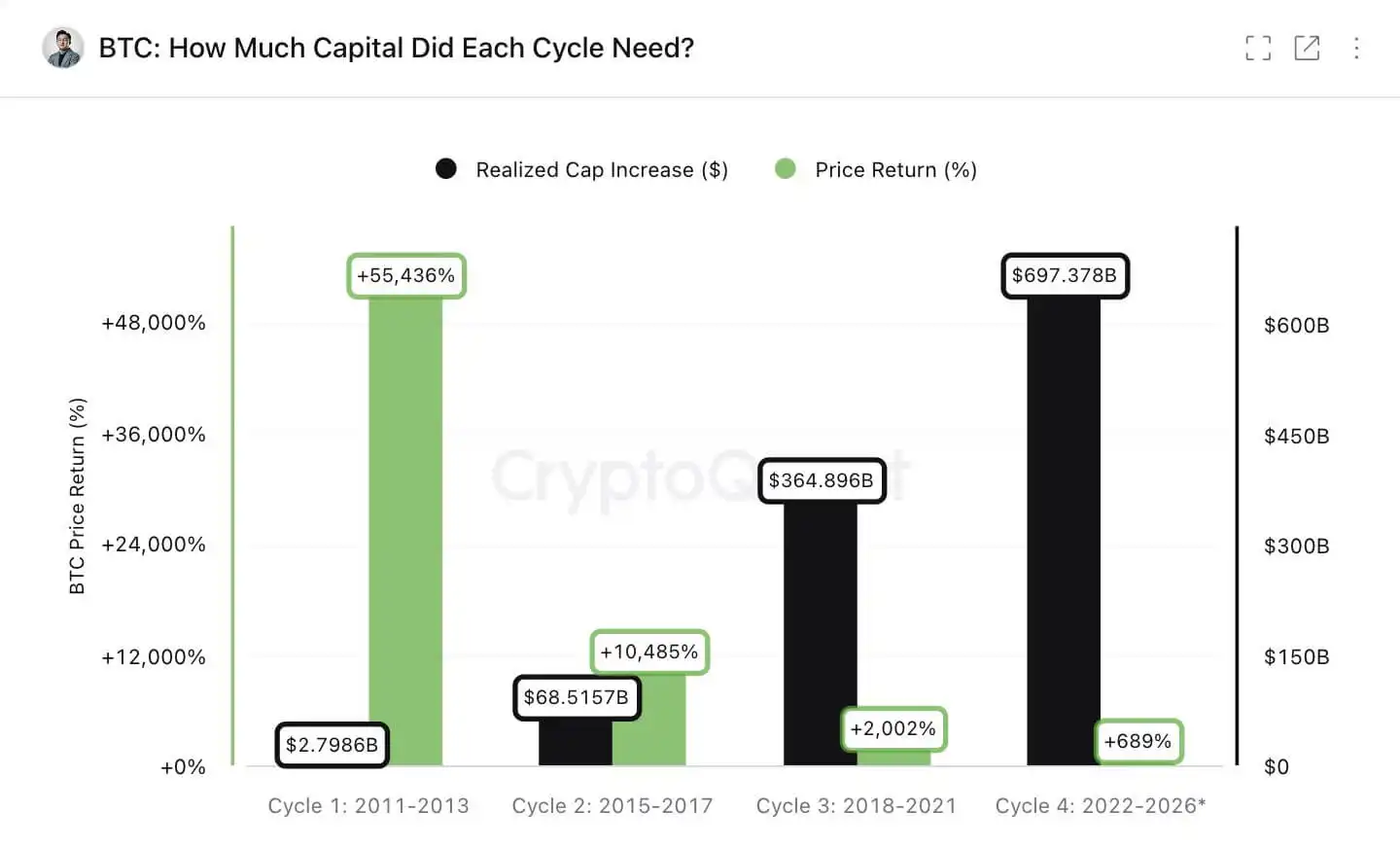

Ju's analysis compares the growth in Bitcoin's realized capitalization across several bull cycles with the subsequent price gains. Realized capitalization calculates coins at their last on-chain move price, making it a common proxy for the amount of capital absorbed by the network.

Ju said that in the 2011 cycle, roughly $27 million in net capital inflow was associated with a roughly 55,000% price gain.

The current cycle has absorbed about $697 billion, producing about a 689% gain, highlighting how much more capital is needed to generate smaller gains as the asset scales.

Figure: Bitcoin Price Returns vs Realized Cap Gains

Source: CryptoQuant

The same pattern appears in smaller increments. Ju said that around $5 million in new money was enough to double the Bitcoin price in 2011. In the current cycle, that figure is around $101 billion.

While this doesn't end the bullish thesis around BTC, it changes the type of demand needed to sustain it.

Ju argues another major rally is still possible if Bitcoin becomes a deeper macro allocation. "Bitcoin needs to become a core macro asset," he wrote, adding that the market can no longer rely solely on retail-dominated ETF trading.

This perspective frames Bitcoin's next cycle as a test of financial market integration. Supply shocks from halvings still reduce new issuance, but the growth trajectory increasingly depends on whether capital allocators treat Bitcoin as a recurring portfolio position rather than a tactical trade.

ETF Outflows Weaken the Near-Term Setup

This test arrives as the market's most visible institutional vehicle hits a rough patch.

U.S. spot Bitcoin ETFs helped broaden access following their 2024 launch, offering advisors, hedge funds, and traditional investors a regulated path to the asset. But recent flows have turned negative, undercutting the argument that institutional demand is already deep enough to support another major rally.

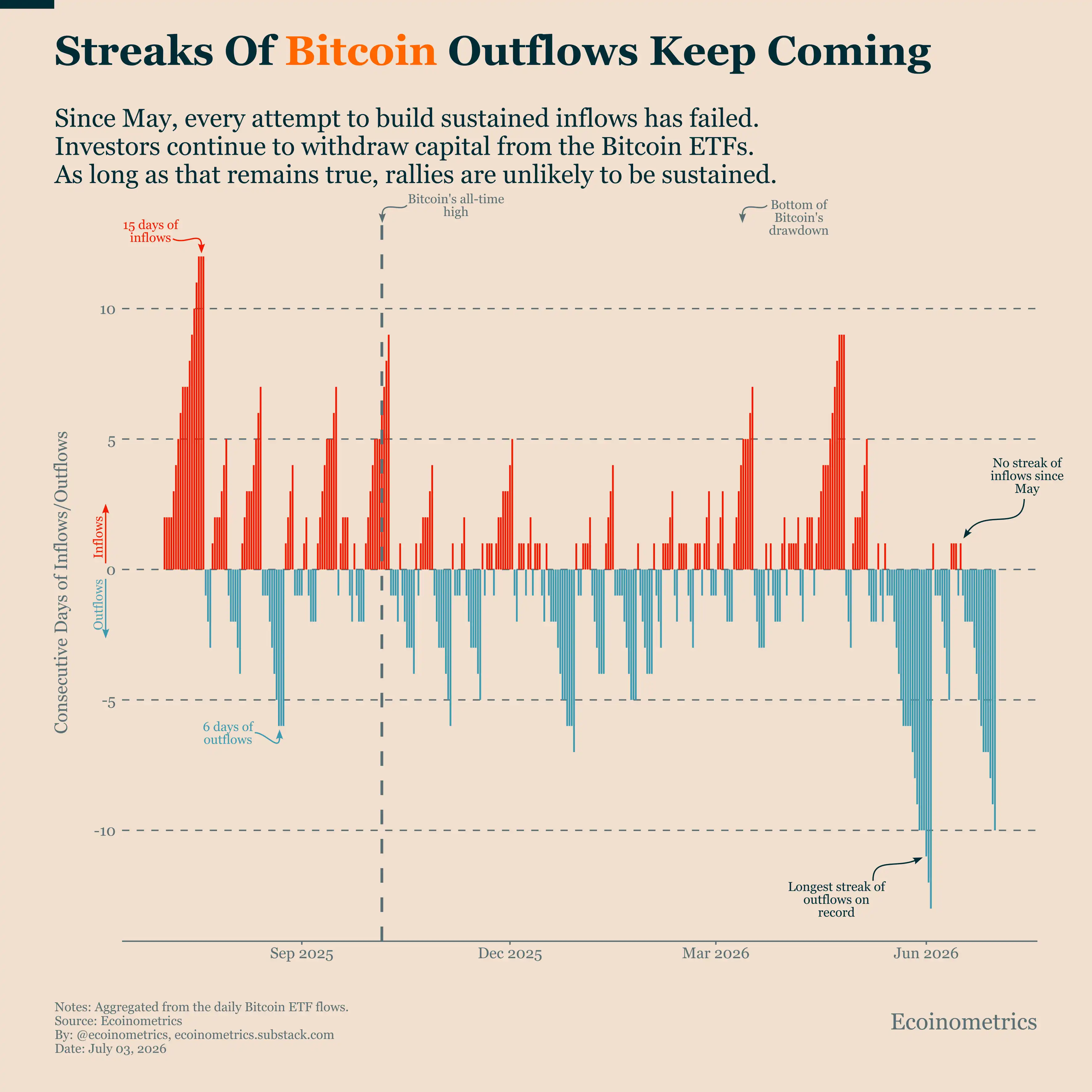

Data from Santiment shows nearly $10 billion in outflows from Bitcoin ETFs since early May, with the 12 products currently on an eight-week streak of outflows.

Addressing these numbers, the BTC-focused analytics platform Ecoinometrics said:

"The pattern since May has been very one-sided. Every attempt to rebuild buying momentum almost immediately stalls. Bitcoin ETFs have failed to achieve more than a single day of inflows, while outflow streaks repeatedly last for days, culminating in the longest outflow streak since the ETFs launched."

Figure: Bitcoin ETF Outflows

Source: Ecoinometrics

These outflows complicate a rapid return to highs. Bitcoin's October record came during a period when investors were still rewarding ETF access and treating the asset as a beneficiary of friendlier policies, institutional participation, and broader links to global markets.

Now, the ETF weakness suggests access alone is insufficient. The next phase of adoption requires steadier allocations across wealth platforms, model portfolios, corporate balance sheets, and other capital pools that move more slowly than retail traders but can deploy at larger scale.

For Bitcoin, this creates a demand landscape that is higher quality but harder to win. Institutions may bring bigger checks, but they also require liquidity, risk controls, custody standards, portfolio mandates, and compliance approval before allocations become durable.

Institutions Are Still Engaging, But With Stricter Standards

Despite these substantial outflows, survey data from Coinbase suggests institutional interest hasn't vanished.

A January 2026 survey of 351 institutional decision-makers by Coinbase and EY-Parthenon found nearly three-quarters plan to increase crypto allocations, while 74% expect crypto prices to rise in the next 12 months.

The same survey found 49% are placing more emphasis on risk management, liquidity, and position sizing.

This combination matters for Bitcoin's capital problem. Institutions don't approach crypto with the same behaviors that defined early retail-led cycles.

They are more likely to demand regulated products, clear governance, operational resilience, and defined exposure limits.

The survey found 66% of respondents already have exposure through spot crypto ETFs or exchange-traded products, while 81% prefer spot exposure through registered vehicles.

These findings support the view that regulated wrapper products remain central to the next adoption phase.

However, they also show why the recent ETF outflows are a pressure point. If ETFs are the primary institutional on-ramp, sustained weakness in these products could slow the broader allocation process.

Thus, Bitcoin's capital-efficiency problem cuts both ways. Its larger scale may make the asset more acceptable to traditional finance.

But that scale also means marginal buyers must be larger, more consistent, and less speculative than those driving early cycles.

Bitcoin's Next Buyers Must Compete With the Rest of Wall Street

This makes Bitcoin's next cycle dependent on a broader set of investors than the retail traders and crypto-native funds that powered early rallies.

Michael Saylor, executive chairman of MicroStrategy, argues Bitcoin's next decade will be less driven by miner issuance and more by capital flows across financial markets. MicroStrategy is the largest corporate holder of Bitcoin, making Saylor one of the most visible advocates for treating the asset as a balance-sheet tool rather than a speculative trade.

According to him:

"Over the next decade, Bitcoin's trajectory will be less driven by miner issuance and more by capital flows. ETF flows. Corporate treasury flows. Sovereign reserve flows. Banking credit flows. Derivative flows. Insurance flows. Collateral flows. Structured credit flows. Global savings flows. Halvings tighten supply. Capital flows set the growth trajectory. This is the next phase of Bitcoin adoption: not just more buyers, but more balance sheets."

The emphasis is that Bitcoin's supply story is no longer novel. Its issuance schedule is known, halving cycles are understood, and the asset already trades at a scale that requires larger pools of capital to move it meaningfully.

Therefore, any new repricing must come from demand channels capable of absorbing a market valued over $1 trillion.

This means ETF demand is only part of the shift. A stronger cycle may require advisors adding Bitcoin to model portfolios, companies using it more aggressively on balance sheets, banks building credit products around it, insurers and asset managers viewing it as a macro allocation, and sovereign entities considering exposure over time.

This shift may be slower than retail momentum cycles. It will also expose Bitcoin more to rate expectations, regulatory delays, liquidity shocks, and competition with other markets chasing the same institutional capital.

Notably, artificial intelligence has emerged as one of those competitors. AI-related assets and infrastructure have absorbed a significant portion of investor attention this year, with spending and investment forecasts reaching trillions.

In earlier crypto cycles, looser speculative capital might have flowed more easily into Bitcoin. In today's market, Bitcoin must compete for the same pool of institutional capital against AI stocks, private infrastructure deals, credit products, commodities, and other macro trades.

That competition is now at the center of the Bitcoin cycle debate. The asset is large enough to enter mainstream allocation conversations, but that also means it gets compared against every other major capital use.

The views expressed in this article are those of the author alone and do not represent the views of CryptoSlate. Nothing you read on CryptoSlate should be taken as investment advice, nor does CryptoSlate endorse any projects mentioned or linked in this article. Buying and trading cryptocurrencies should be considered a high-risk activity. Please conduct your own due diligence before taking any action related to the content of this article. Finally, CryptoSlate assumes no liability for any losses incurred while trading cryptocurrencies. Please refer to our company disclaimer for more information.