On June 19th, Aave founder Kulechov positioned the upcoming Aave V4 as an on-chain alternative to Wall Street securities financing, targeting the U.S. daily markets of approximately $12.6 trillion in repo, $4.6 trillion in securities available for lending, and margin financing. He proposed three product types: securities-backed loans, repo (atomic settlement), and securities lending. Its institutional-grade RWA lending market, Horizon, has accumulated about $440 to $550 million in deposits since its launch in August 2025, with a target of exceeding $1 billion by 2026. This upgrades the narrative from "RWA as collateral" as a single product to "on-chain securities financing infrastructure."

Using the three-layer framework, the essence of this lies in the third layer—composability. V4 does not change the credit of any underlying assets, nor does it directly create liquidity mismatches; what it does is uniformly connect any issues from the first two layers to on-chain leverage and liquidation. In other words, it transforms the composability layer we have consistently highlighted, from a risk point, into the backbone of the system.

Aave is qualified to do this. By the end of 2025, it commanded about 61.5% of the active lending market share and held over half of the total TVL in the entire lending sector. Its engineering is also more prudent than typical DeFi—Horizon uses Chainlink's NAV oracle for net asset value pricing, employs LlamaRisk and Chaos Labs for risk parameters, makes aTokens non-transferable, and maintains non-custodial contracts. These aspects should be acknowledged, not dismissed outright.

However, one design choice warrants closer examination. V4's "centralized liquidity Hub + multiple Spokes" architecture, along with Horizon's shared liquidity pool, reflects the same orientation—prioritizing capital efficiency. The shared pool allows new assets to immediately access deep liquidity upon listing, resulting in more stable interest rates, which is an advantage; the trade-off is the loss of risk isolation: if collateral of a certain type encounters problems during stress periods, it draws from the same stablecoin pool shared by all other collateral types. While enhancing efficiency, the shared pool expands the risk exposure of the composability layer from a single asset to the entire market. This is the other side of the trillion-dollar TAM narrative that is often overlooked.

This risk is not hypothetical. In April 2026, an attack on a third-party cross-chain bridge resulted in approximately 116,500 unbacked rsETH being deposited as collateral into Aave, creating bad debt—this is precisely the template for "collateral integrity issues → bad debt," unrelated to whether the underlying asset defaults.

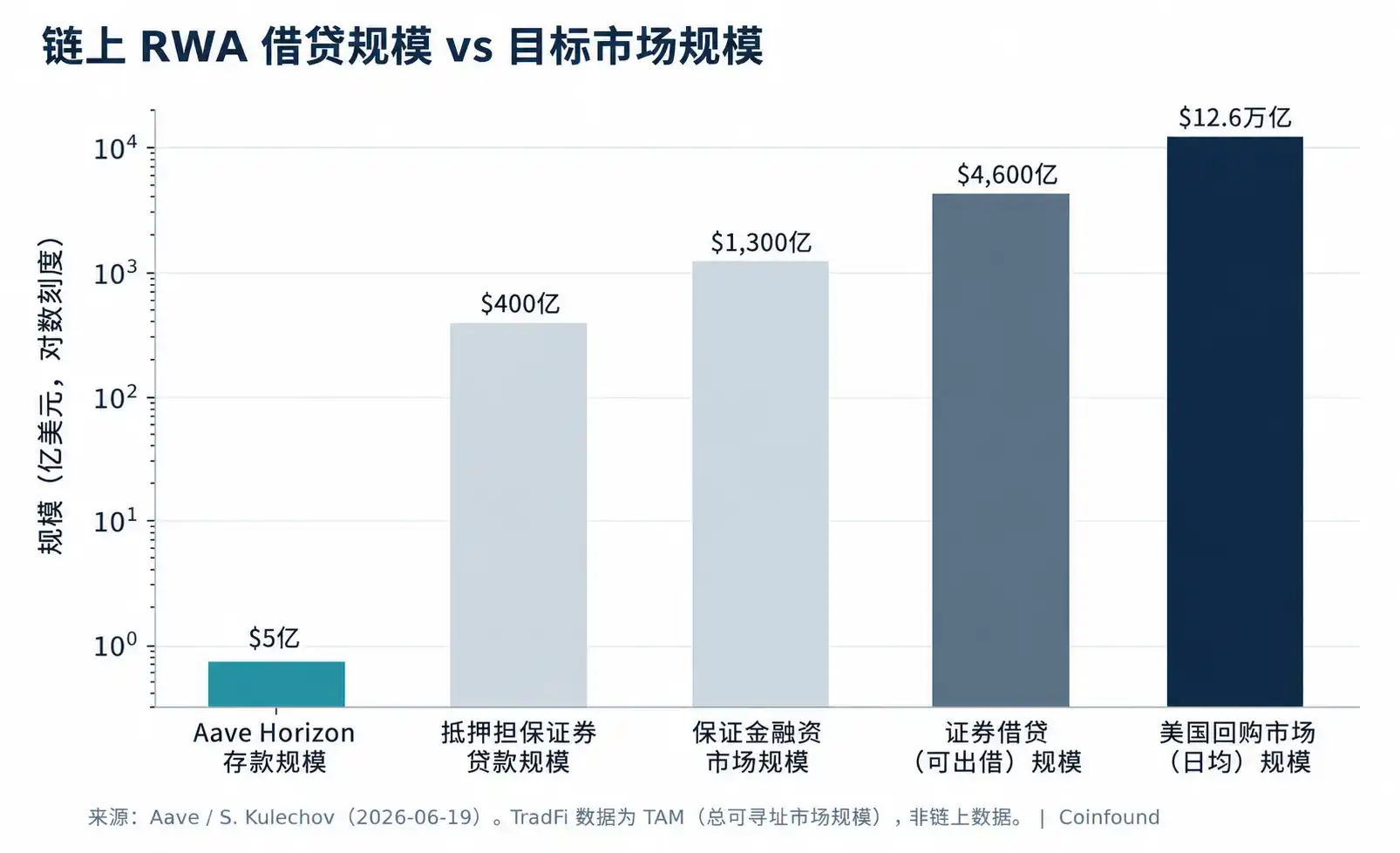

In terms of scale, Horizon's current ~$500 million and target of $1 billion is just a starting point relative to the $12.6 trillion repo market it aims for (see chart below); precisely because of this, this mechanism for uniformly levering various RWAs has not yet been tested in any genuine credit or liquidity stress scenario. Combined with our previous estimate of 5%–10% NAV drift for CLO-like tokens during stress periods, leveraged positions might be wiped out before the NAV is rebalanced. We tend to believe that the first scaled bad debt or forced liquidation for RWA collateral will be triggered by a dislocation between the price/NAV of the collateral token during stress, rather than by underlying asset default—manifesting as a liquidation or loss distribution in an institutional-grade RWA lending market, while the underlying credit does not default.

The implications differ for various parties: Institutions supplying collateral to such markets should set discounts based on the "NAV vs. on-chain price" gap during stress, not just credit. Lenders supplying stablecoins to these markets must understand they are exposed to a shared pool and to every type of collateral within it, not just the specific type they favor. For risk service providers and protocols, the choice between isolated pools and shared pools is a trade-off between risk isolation and capital efficiency. Within our three-layer framework, this article, along with the concurrent stablecoin discussion (the assets being borrowed) and the previous CLO discussion (the assets being collateralized), point to the same main theme—the market still primarily focuses on the credit layer, while tokenization repeatedly creates new risks in the latter two layers. Independently pricing the liquidity and composability risks of collateral tokens is precisely Coinfound's position.

Chart: On-chain RWA lending remains minuscule relative to the traditional securities financing market it targets (Source: Aave / Kulechov, 2026-06)

Disclaimer: This article is for informational purposes only and does not constitute any investment advice; data may be delayed or contain errors, please refer to official disclosures.