Author: IreneDu

This is article 2.5 in the series analyzing Stripe's AI strategy.

The series originated from observing that Stripe Sessions 2026 announced 288 products on April 30. I noted that Stripe is attempting to become the economic infrastructure for the AI Agent era.

The first article, Stripe is Not a Payments Company, aimed to answer "Why Stripe?"—its DNA dictates its capability for this role.

The second article, KYC is Dead: The Agent Economy is Rewriting the Foundation of Financial Regulation, intended to dissect the future Stripe is betting on—what the Agent Economy truly looks like and why traditional payment infrastructure will fail completely in its presence.

However, while writing the second article, I received a comment from a colleague:

I completely agree with the first half. Neither AB 316 nor any sovereign state's laws will recognize "Agent as a legal entity" in the short term—the ultimate defendant will always be a specific person. Know Your Agent cannot and will not change this fact.

But I have reservations about the second half—"The only change is the efficiency of payment and settlement." The issue is not with the conclusion, but with the default framework: it views KYA as merely an upgrade to the existing payment system.

This is precisely what I believe merits an additional article for discussion.

First, let's return to the muscle memory of a former payment practitioner:

Payment forms are driven by scenarios, not designed from within the payment system itself.

Every true leap in payments—online banking, mobile wallets, QR code scanning—was not because someone created a better product at the payment layer, but because a new transaction scenario emerged, shattering the underlying assumptions of the old payment system.

New payment forms "emerge" from the infrastructure demanded by that scenario, not "optimized out" of existing systems.

I once worked on payment innovation at Ant Group. Within a platform that was an absolute industry leader, having pioneered "Quick Pay," "Mobile Payment," and "QR Code Payment," the greatest joy and pain was contemplating: What is the next generation of payment?

We developed watch payments (and heartbeat authentication as an alternative to facial recognition), NFC payments (the original tech behind "touch to pay"), participated in drafting several "next-generation" payment protocols, and even attempted to secure leadership support for exploring metaverse payments.

Most of these projects didn't succeed.

Looking back, the reason was the same: we attempted to define new payments at the payment layer, but the scenario driving payment transformation hadn't arrived yet—without the scenario, the infrastructure it needs cannot emerge, and no amount of clever design at the payment layer can support it.

The Agent Economy is precisely that new scenario I was waiting for.

KYA is the layer of infrastructure currently emerging.

KYA is not a product within the payment layer; it is an infrastructure layer for the Agent Economy.

The five layers of KYA I defined in the previous article—Agent Identity, Authorization Scope, Intent Signing, Liability Chain Audit, Credit Rating—only the Authorization Scope and Liability Chain Audit layers reside on the payment chain. The other three (Identity, Intent, Credit) are not within payments at all.

- The Identity layer serves all scenarios requiring Agent identification: cross-platform calls, regulatory filing, internal corporate audits—payment is just one of them.

- The Intent layer serves the broader issue of AI alignment—payment is just one of its many verification scenarios.

- The Credit layer serves any system needing to assign permissions and quotas to Agents—payment is again just one user of it.

Therefore, my colleague's assertion that "the only change is the efficiency of payment and settlement," translates into infrastructure terms as: viewing KYA as a subsystem of payments.

My judgment is the reverse: payments are a subsystem of KYA.

This reversal is the core of this discussion.

Stripe's investment actions at the industry frontline serve as empirical evidence.

Patrick Collison used the term not "AI payments" but "economic infrastructure for AI" at Sessions 2026. This is not marketing language; it's a positioning choice. It indicates Stripe doesn't intend to lock itself into the identity of a "payments company"; it's betting on being the foundation for the Agent Economy.

Regarding specific product positioning:

The Agentic Commerce Protocol (ACP), jointly built by Stripe and OpenAI, now used by Microsoft Copilot, Meta, and Google Gemini (who joined in April)—it is essentially an identity and session protocol, not a payment protocol.

Shared Payment Token, which separates the Agent from the real card number, functions at the authorization layer, not the settlement layer.

Stripe acquiring Bridge for stablecoin infrastructure, acquiring Privy for embedded wallet capabilities, building the Tempo blockchain as a settlement pipeline—this entire portfolio doesn't fit within the "payment efficiency optimization" framework.

This investment portfolio only makes sense under the judgment that "KYA is the infrastructure layer." If the Agent Economy were merely a payment efficiency issue, Stripe wouldn't need stablecoins, embedded wallets, or its own L1. What it's doing is occupying positions across those five KYA layers.

Data provided by Stripe's Head of Data, Emily Glassberg Sands, in an Every interview this April, corroborates this from another angle: a major AI client had 250,000 fraudulent free trials blocked weekly; she saw an AI company spending $25 on compute per free trial with a 4% conversion rate, meaning losing $625 per paying user acquired; overall free trial abuse has increased 4x in the past six months.

These numbers collectively indicate one thing: in the AI economy, the judgment determining whether a transaction can proceed or is worth pursuing no longer occurs at checkout—it happens upstream in questions like "who is this, what do they intend to do, are they worth the resources." This is why Stripe is moving its risk control Radar from the "moment of transaction" to the "entire user lifecycle." It's not about making old risk control faster; it's about shifting the focus from "is this payment problematic?" to "is this user/Agent's overall behavior problematic?" The former is a payment layer issue; the latter belongs to the KYA layer.

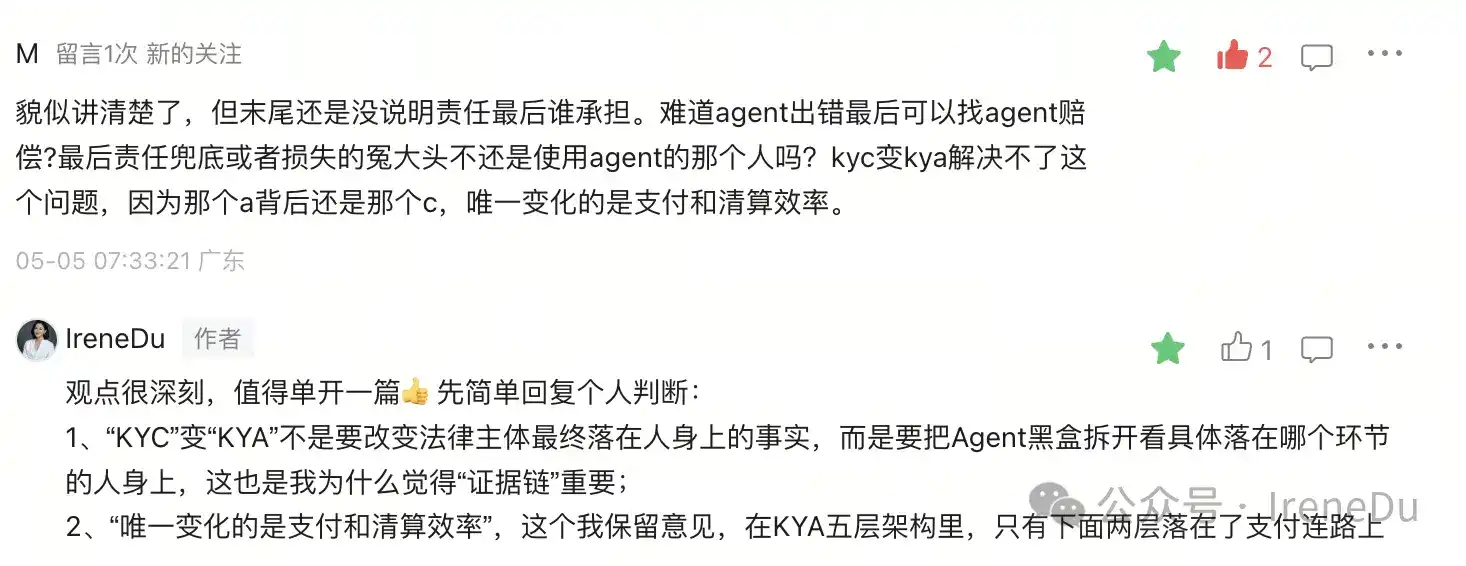

Returning to the colleague's question: who ultimately bears the liability?

He is right—the ultimate legal entity remains a person. AB 316 has codified this legally.

But this is precisely the real problem KYA must solve: when the liability chain becomes distributed, the act of finding "which specific person in which specific link" is something the KYC era didn't need to do but the KYA era must.

In the KYC era, the liability chain was linear (user → payment/bank → merchant). When a transaction had issues, you intuitively knew who to look for.

In the KYA era, the liability chain is a network (user → Agent platform → model provider → payment protocol → bank → merchant, potentially calling other Agents in between). Even if the law says "find a person, not an Agent," you still wouldn't know which person—because liability is now distributed across 5–7 entities.

KYA cannot change the legal finality of liability. But it can, within a networked chain, cryptographically solidify the role and actions of each entity—who authorized what, who executed what, who settled what, who fulfilled what. Transforming "no evidence to find" into "evidence can be found"; "which link failed is unverifiable" into "verifiable."

This is not a payment efficiency enhancement.

This is the first time liability traceability can exist within an Agent network.

Therefore, the statement "the only change is the efficiency of payment and settlement" confuses infrastructure with function.

What's truly happening is:

- Because a new type of economic actor (Agent) has emerged, a new layer of infrastructure (KYA) is forced to grow.

- This infrastructure layer redefines "who is on the other side, what can they do, who to find if something goes wrong." Upon this layer, payments will reorganize themselves into a form we cannot fully envision today.

What exactly is the next generation payment form? The new species Stripe is attempting to define is still unclear.

But in this world of uncertainty, one thing I am sure of—it will not be designed within the payment layer.

It will emerge from the scenarios, once the KYA infrastructure layer is laid.