Author: Khing Oei

Compiled by: Chopper, Foresight News

Recently, the markets for MSTR and STRC have experienced significant volatility. We should look beyond short-term price fluctuations and revisit the underlying logic: Bitcoin reserve companies are essentially single-asset, leveraged holding entities, with a business model closer to that of a bank rather than a software technology company.

From a valuation perspective, the market would never price a bank based solely on its total assets. A bank's loan assets are prioritized for repayment by depositors and debt holders, with common shareholders only entitled to residual equity. Therefore, the core valuation metric for banks is the price-to-book ratio (P/B), which is the value of shareholders' equity after deducting senior debt from total assets. This is also the primary reference metric for investment bank and brokerage analysts.

For Bitcoin reserve companies, the equivalent P/B metric is mNAV: it equals the company's market capitalization divided by the equity net asset value, where equity net asset value refers to Bitcoin reserves minus debt and preferred stock senior to common shares. As of the previous close, Strategy's mNAV was 1.10x. (Translator's Note: The "previous close" data mentioned in this article refers to June 24th data.) The underlying per-share fundamental is the net Bitcoin per share—the actual amount of Bitcoin owned per share after settling priority claims. This is equivalent to the per-share book value denominated in Bitcoin. The industry-wide focus—the per-share Bitcoin growth rate—represents the return on this book value. For a capital management company, this is almost equivalent to an earnings metric.

This set of metrics is not my invention; it simply applies the traditional bank financial analysis framework to a Bitcoin balance sheet:

- Market cap per unit of equity / Net asset value = Price-to-Book Ratio

- Net Bitcoin holding per share = Book value per share

- Bitcoin holding growth per share = Return on book assets

This is the valuation logic common to all leveraged financial institutions and is fully applicable to these Bitcoin reserve companies.

MSTR closed yesterday at $94.13 per share, below the total net Bitcoin value per share of $143.76, resulting in a rough total net value multiple of only 0.65x. Viewed solely through this lens, the stock trades at nearly a one-third discount to its Bitcoin asset value, making a stock issuance to buy more Bitcoin seem dilutive. However, after deducting the approximately 40% of Bitcoin equity occupied by debt and preferred stock, the current stock price represents 1.1 times the Bitcoin assets actually held by common equity. The two perspectives lead to completely opposite conclusions, and the banking valuation framework is the correct benchmark, which also determines how the company should use any new capital raised at present.

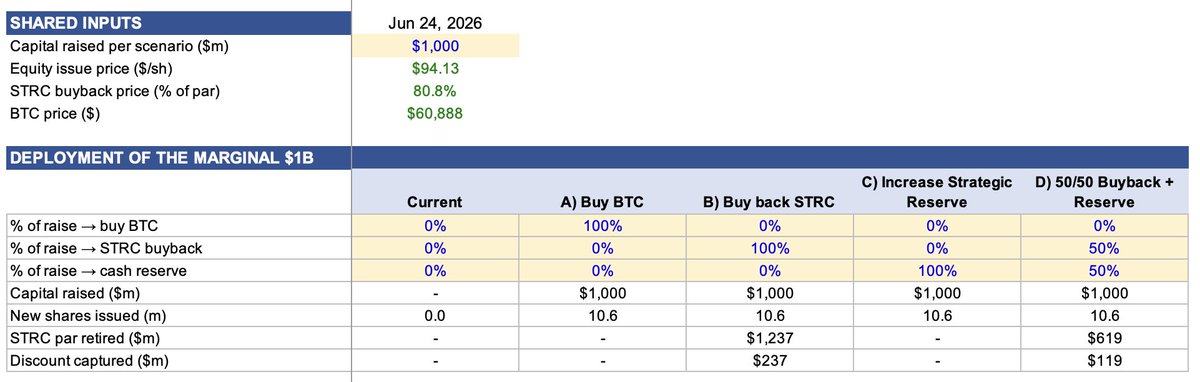

Simulating Four Use Cases for $1 Billion in New Capital

Assuming a $1 billion equity issuance at the current stock price, we simulate the effects of four potential uses for the funds: 1) Increase Bitcoin holdings; 2) Repurchase STRC; 3) Boost cash reserves; 4) A 50/50 split between repurchasing STRC and boosting cash reserves. The issuance price is $94.13 per share; yesterday's STRC closing price was $80.84, a 19% discount to its par value, translating to an actual annualized yield of 14.2%. For every $1 spent on repurchases, $1.24 of STRC at par value can be retired, simultaneously eliminating the 11.5% perpetual dividend.

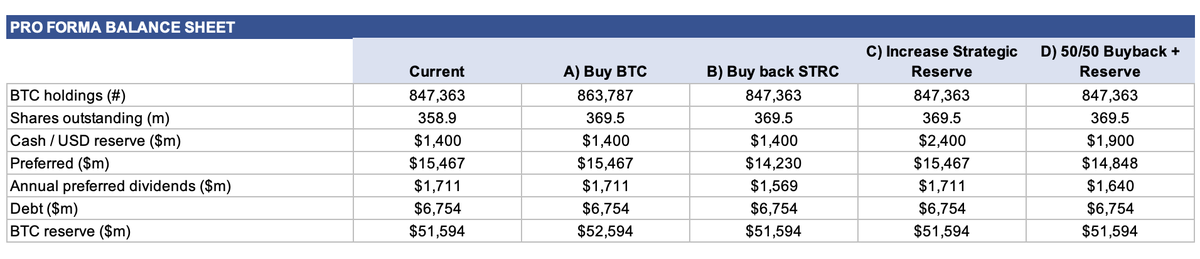

Impact of the Four Scenarios on the Balance Sheet

Three of the four scenarios do not increase Bitcoin holdings; they only adjust the structure of the senior claims layer:

Repurchase STRC: Buying back at a 19% discount, $1 billion can retire $1.24 billion of STRC at par value. Annual preferred stock dividend payments decrease from $1.711 billion to $1.569 billion.

Boost Cash Reserves: Cash reserves increase from $1.4 billion to $2.4 billion, with dividend payments unchanged.

50/50 Split Scenario: Cash increases to $1.9 billion, dividend payments decrease to $1.640 billion, and $619 million of STRC at par value is retired.

Increase Bitcoin Holdings: The only scenario that increases Bitcoin reserves, raising total holdings from 847,363 BTC to 863,787 BTC. This is also the weakest choice for improving core metrics.

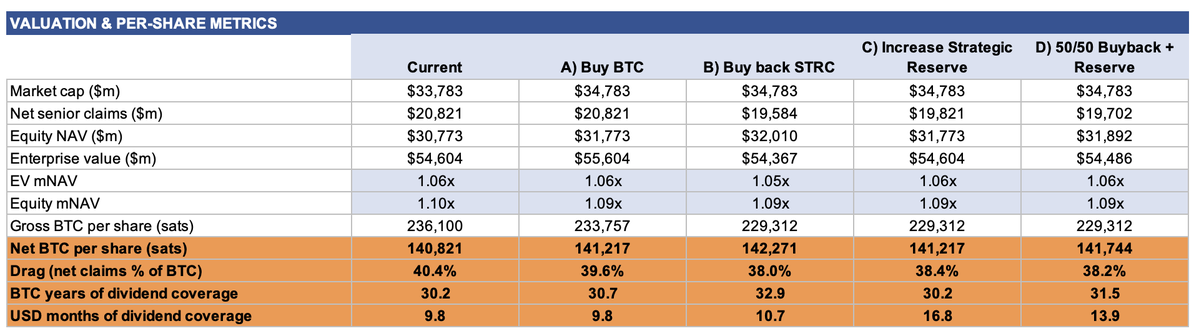

Calculating total Bitcoin value per share, all four scenarios show dilution. Even if you use the entire $1 billion to purchase Bitcoin, the per-share value decreases from 236,100 satoshis to 233,757 satoshis; in the three scenarios where stock is issued but no Bitcoin is purchased, the per-share value drops even further to 229,312 satoshis. Based on this, you would conclude: the company should do nothing.

However, in terms of net Bitcoin value per share, every option results in an increase:

- Repurchase STRC: Net Bitcoin per share rises to 142,271 satoshis (+1.0%). Debt-to-assets ratio decreases from 40.4% to 38.0%. This provides the strongest balance sheet repair.

- 50/50 Split Scenario: Net Bitcoin per share becomes 141,744 satoshis, with a debt-to-assets ratio of 38.2%. Cash coverage for debt service is significantly enhanced.

- Purely Boosting Cash Reserves or Increasing Bitcoin Holdings: Both result in 141,217 satoshis per share, showing the smallest increase.

The logic for Bitcoin purchases being the least effective is clear. You are issuing stock at 1.1 times net asset value but purchasing assets at 1 times net asset value. This only slightly increases net Bitcoin per share while diluting the widely followed total Bitcoin holdings metric. In contrast, repurchasing STRC at a discount creates immediate value.

The market's current key concern is the dividend cash coverage in months. Strategy currently has $1.4 billion in cash reserves and annual STRC dividend payments of $1.711 billion, meaning cash covers only 9.8 months of dividends:

- Increase Bitcoin Holdings: Coverage remains at 9.8 months.

- Repurchase STRC: Improves to 10.7 months.

- Purely Boost Cash Reserves: Significantly improves to 16.8 months.

- 50/50 Split Scenario: Improves to 13.9 months.

This is another core banking metric: the liquidity coverage ratio. No one pays attention during loose funding cycles, but during funding contractions, it becomes crucial for corporate survival. The fact that STRC is trading below par is a direct signal of market funding channel tightening.

Company's Own Financial Data Also Confirms This Conclusion

The above analysis is not a subjective judgment; Strategy's Q1 earnings report provides the same break-even threshold. According to the company's own framework, selling MSTR to buy Bitcoin only increases Bitcoin per share when mNAV is above 1.22x. At the current multiple of 1x, such a move directly erodes value by 48 basis points. The company's current EV is 1.06x and mNAV is 1.10x, both below its internal break-even line.

The two core assumptions behind the company's conventional expansion path have now completely failed. Previously, it was assumed that STRC could be issued at par normally and that cash reserves could cover 1.5 years of dividends. Now, STRC trades at $81 and cannot be issued at par, and cash reserves cover less than 10 months of dividends.

What Should Strategy Do?

Within the current valuation range, issuing new equity and deploying the capital into channels that tangibly optimize core financial metrics is key. Both boosting cash reserves and repurchasing STRC at a discount can increase net Bitcoin per share, reduce the debt burden, and repair the market's concern over liquidity coverage. The 50/50 split scenario can achieve all these objectives simultaneously.

Continuing to add Bitcoin at present would only optimize the superficial metrics widely followed by the public, while neglecting the core balance sheet risk of the company carrying $15 billion in priority debt amidst tightening funding channels.

Investors focused solely on the total Bitcoin holdings metric miss the positive feedback loop. Repurchasing STRC directly supports token buy-side pressure and signals confidence in liquidity safety. Once market panic subsides, STRC prices should recover toward the $100 par value; price appreciation corresponds to lower yields, and the current high yield of 14.2% would continue to narrow. A complete positive cycle thus forms: repairing the balance sheet → STRC price recovery → dividend yield declines → the previously closed channel for par-value issuance reopens.

The STRC discount is not something that can only be passively waited out for repair; the current deep discount represents the lowest-cost capital the company can access and is key to restarting other funding channels.

To evaluate Bitcoin reserve companies, one should apply banking valuation standards: price-to-book ratio, per-share book value, and debt servicing capacity under stress environments.