In July of last year, we conducted a detailed analysis of Meteora's operational strategy. The highly consensual community philosophy indeed provided significant assistance for our own project operations. (Related reading: How to Build a Powerful LP Army Like Meteora?)

Now, amidst the bull and bear market transition, compared to other products in the same sector, Meteora can still maintain relatively stable liquidity and revenue.

Reviewing Meteora's product iteration approach might give us a more intuitive understanding of the qualities a product needs to possess to weather bull and bear markets.

I. The Capital Efficiency Revolution: The Structural Issues Meteora Aims to Solve

Meteora's core lies in optimizing liquidity and capital efficiency. Traditional AMMs suffer from issues like fragmented liquidity, high slippage, and limited returns. Meteora addresses these through the DLMM (Dynamic Liquidity Market Maker) and dynamic AMM mechanisms.

For example, DLMM divides liquidity into multiple "bins" based on price and can adjust fee rates in real-time: when market volatility increases, fees rise, offsetting LP losses in volatile markets. This design of dynamic fees and precise liquidity concentration allows for near-zero slippage within the same bin, significantly improving trading efficiency and LP returns.

Meteora's Dynamic AMM product also automatically deploys a portion of assets to lending protocols in the background, generating additional yield and avoiding sustainability issues reliant solely on mining incentives. In summary, through technological upgrades and incentive mechanisms (such as fee sharing, MET points, etc.), Meteora greatly enhances capital efficiency and LP profit potential.

II. DLMM: How the Dynamic Liquidity Model Reshapes Market Making Logic on Solana

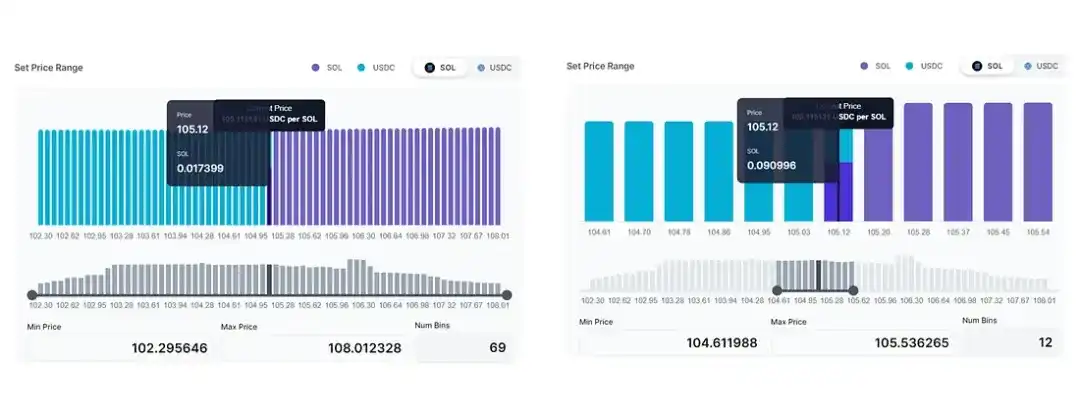

DLMM is Meteora's most core innovative product, which can be seen as a "segmented concentrated" liquidity pool. Unlike traditional constant product pools, DLMM allocates a trading pair's liquidity across multiple price bins, allowing LPs to choose different volatility distributions based on their strategies.

When trading within each bin, liquidity is precisely concentrated, resulting in almost zero trading slippage. LPs can maintain higher capital utilization even with high trading volumes. Furthermore, DLMM dynamically adjusts fee rates based on market volatility: increasing fees during high volatility to offset LPs' impermanent loss and lowering fees during calm periods. LPs in DLMM not only earn basic trading fees from providing liquidity but also gain volatility fees and liquidity mining rewards.

DLMM also衍生出 a Launch Pool model specifically designed for new token launches, enabling tokens to quickly aggregate liquidity and become tradable on routers like Jupiter in their early stages. In short, DLMM creates more profit opportunities for LPs through high capital efficiency, flexible volatility strategies, and dynamic fee mechanisms.

DLMM organizes liquidity by price bins. Each bin maintains sufficient funds, achieving "zero slippage" trading within the bin.

The core algorithm includes a base fee rate and a maximum fee mechanism, automatically increasing fees when market volatility rises and decreasing them to attract more trades during calm periods. Slippage control is achieved through discrete bin filling: trades within each price bin only occur at that bin's price, avoiding impact from fragmented depth.

Meteora also designs various strategies for different market conditions, such as the "Curve Strategy" concentrating liquidity near the current price, and the "Buy/Sell Bin Strategy" hedging against extreme volatility.

For stable trading pairs like USDC/USDT, most trading is concentrated within a narrow range, leaving a large amount of capital idle in traditional AMMs. Under the DLMM design, LPs can concentrate more liquidity into this narrow range, thereby earning more fees and achieving a significant improvement in capital efficiency.

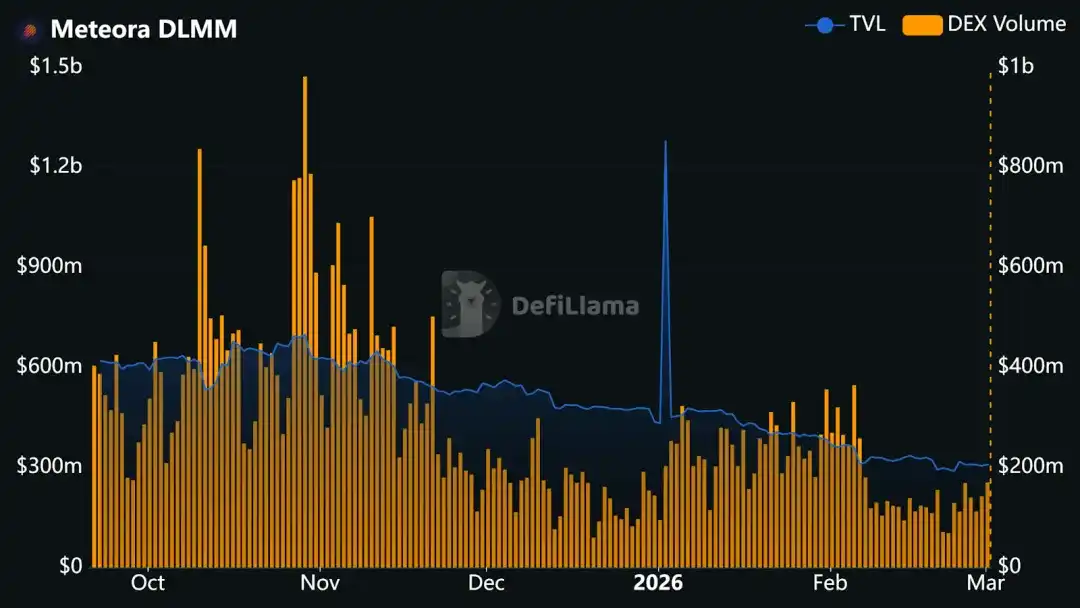

More importantly, DLMM is not just about price bin distribution; it can also automatically adjust fees based on actual trading activity and volatility. This "on-demand fee" mechanism is unachievable in traditional fixed-fee AMMs. Because fees are linked to volatility, LPs receive higher fee compensation during high volatility periods, fundamentally mitigating the risk of Impermanent Loss and increasing profit potential. Data-wise, as DLMM gets integrated into aggregator routers like Jupiter, participation in Meteora's DLMM pools continues to grow.

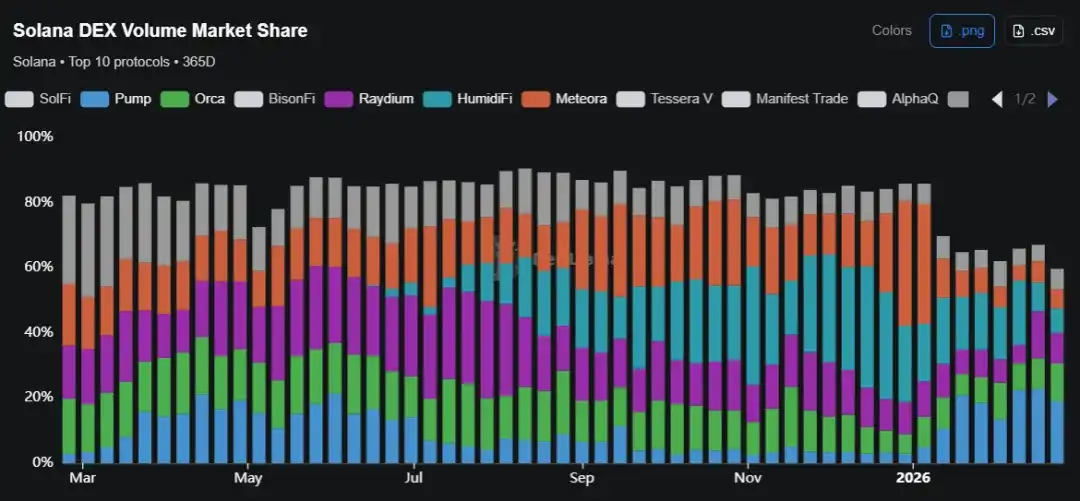

As of early 2026, the total value locked (TVL) in DLMM reached approximately $300 million, generating tens of billions of dollars in trading volume over the past 30 days, occupying an important position in the Solana DEX ecosystem landscape.

III. From DAMM v1 to v2: Two Key Transitions in Meteora's AMM Mechanism

Meteora's Dynamic AMM (DAMM) series of products are similar to traditional constant product pools but integrate more flexible features.

DAMM v1 was Meteora's first AMM, where LPs could earn trading fees and additionally gain lending yield. In DAMM v1, user-deposited assets are automatically allocated to backend Dynamic Vaults and deployed to lending protocols, earning extra interest and rewards.

This mechanism reduces reliance on single mining incentives, allowing LPs to simultaneously earn trading fees, lending interest, and mining rewards. LPs can also choose to permanently lock their liquidity to boost community confidence; locked assets can still continuously produce yield, especially suitable for dynamic fee configurations in memecoin pools.

DAMM v2 is a new generation AMM, compatible with Solana Token2022 tokens, and offers richer features. Its characteristics include: optional fixed or dynamic fee mechanisms, the ability to set higher dynamic fee caps on-chain, built-in anti-snipe mechanisms, and the ability to partially concentrate liquidity (Position NFT).

DAMM v2 also supports the creation of single-asset liquidity pools (similar to DLMM's single-sided pools) and builds mining mechanisms directly into the contract, improving efficiency.

Compared to DLMM, DAMM v2 has lower creation costs (creating a single pool costs ~0.022 SOL, while DLMM requires ~0.25 SOL) and offers flexible fee collection and locking options. These designs allow projects to conduct token launches more conveniently and provide LPs with more autonomy and profit tools.

IV. The Evolving Protocol: Strategic Intent Behind Functional Iterations

Since 2024, Meteora has continuously iterated new features to enhance user experience and protocol activity.

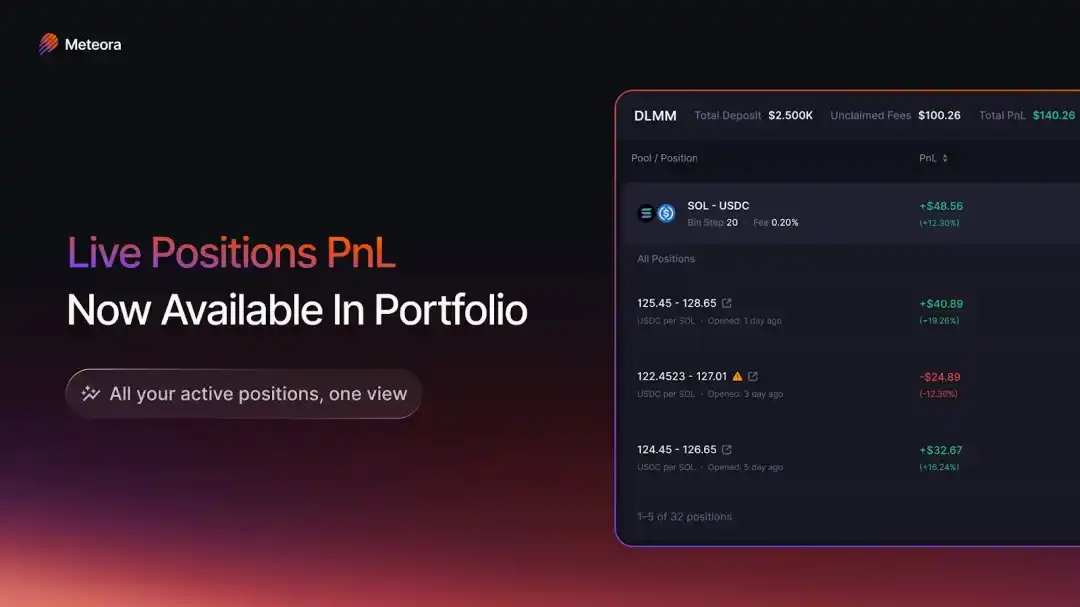

For example, one-click Rebalance and one-click Ape In functions allow LPs to quickly adjust or invest during market volatility or new token launches; the PnL analysis dashboard enables real-time tracking of profit status; the Pool Discovery page helps users quickly filter high-yield liquidity pools; the Merge Positions function allows users to combine multiple positions in the same pool, reducing management costs; Auto-Compound automatically reinvests earned rewards back into liquidity; the LP Points Leaderboard quantifies liquidity provision and contribution behavior into points, incentivizing long-term participation.

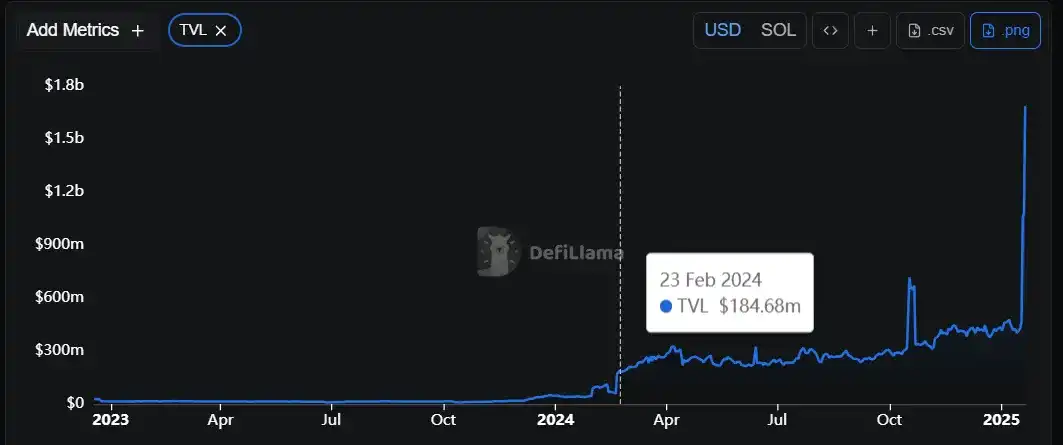

After each feature release, community feedback has been positive, with noticeable growth in user numbers and TVL. According to official data, the points incentive system launched in early 2024 directly drove TVL from ~$40 million to ~$160 million. After the features went live, community discussions were enthusiastic, and the usage rate of new features steadily climbed, further consolidating Meteora's leading position among Solana protocols.

V. LP Army: How Meteora Turns Liquidity Providers into "Combat Units"

Meteora's operations are education-driven at their core, cultivating loyal LPs through the "LP Army" system.

Its centerpiece is the regularly held LP Army Bootcamp: a two-day free training camp for入门 learning LP basics and conducting hands-on exercises. Participants are required to invest ≥$100 in liquidity for a specified non-stablecoin trading pair on the first day and hold it for ≥1 hour. After passing a profit and operation exam on the second day, they receive an NFT graduation certificate and "LP Army Private" status.

After completing the training and becoming正式成员, LPs not only receive protocol airdrop points and community status but also unlock advanced courses, exclusive Discord channels, and a series of strategy analysis tools (such as profit trackers and Dune dashboards).

Community co-building tools are abundant: Metlex provides a professional dashboard for DLMM LPs, offering real-time analysis of position performance; Ultra LP acts as an LP's "partner," aggregating all收益 and PnL; GeekLad's DLMM Profiler helps LPs optimize strategies; MetEngine enables one-click position creation and copying top strategies through channels like Telegram.

Furthermore, the community implements a one-on-one mentorship system, where experienced LPs guide newcomers, covering content like liquidity strategies and impermanent loss management. In terms of governance, user behavior is closely tied to incentives: Meteora has established a MET points system where LPs can earn points by providing liquidity and inviting friends. Points can be redeemed for future MET token airdrops or community privileges. For example, after the system launched, TVL rapidly increased from $40 million to $160 million, showing significant incentive effects.

Ultimately, this multi-layered incentive of "points + tokens + honor" ensures rewards are distributed to long-term contributors, not short-term "pump and dump" behavior. The upcoming MET token release will be further linked to the points system, providing more governance and economic incentives for early community members.

VI. Survival Model in a Bear Market Cycle: Analysis of Meteora's Pressure Resistance Mechanisms

Since 2023, the overall crypto market entered a deep bear market cycle, with DeFi protocols普遍 facing structural pressures like TVL contraction, decreased trading activity, and user attrition.

However, Meteora's on-chain performance showed a relatively robust recovery curve. This "resilience" is not a sporadic market windfall but the result of the synergistic effect of multiple strategies at the incentive design, product architecture, risk control, and community organization levels.

On the incentive level, Meteora not only attracts long-term user participation through traditional locking rewards and fee sharing but also creatively introduced a Stake2Earn model. The design初衷 of this mechanism is to transform the memecoin ecosystem, which could otherwise lead to rapid sell-offs, into an收益 system based on "staking competition."

In traditional token economics, memecoin projects often experience strong selling pressure shortly after launch, as holders tend to sell quickly after short-term arbitrage. This behavior intensifies, especially in late bull markets or bear markets. Stake2Earn's construction logic goes completely against this trend. It allows token holders to stake MEME tokens into designated Stake2Earn contracts to participate in the sharing of trading fees. The core value of this mechanism lies not in short-term speculation but in encouraging holders to lock tokens into the protocol long-term to earn fees generated by liquidity pool trading.

Participation in Stake2Earn does not require holding LP tokens; it only requires users to stake the native memecoin. This design has two significant implications: First, users do not bear the specific impermanent loss risk associated with LPs because they are staking a single token, not LP tokens. Second, stakers have the opportunity to directly participate in the protocol's fee revenue, directly linking personal利益 with protocol growth, mechanistically incentivizing users to become long-term supporters rather than short-term arbitrageurs.

Specifically, the Stake2Earn mechanism allocates users a leaderboard ranking based on the staked amount. Only the top stakers (e.g., Top 5 to Top 100, configurable range) can enjoy fee-sharing收益. The higher the rank and the larger the staked amount, the more fee share the user receives from liquidity pool trading. The system updates the leaderboard in real-time and dynamically distributes income based on current rankings. This "real-time收益 growth" design not only incentivizes users to continuously increase their stake but also prompts participants to constantly compete to retain their收益 eligibility.

The reward structure of Stake2Earn is also very unique, employing a dual reward method: after meeting the ranking conditions, users can claim fee收益 in the form of quote tokens (e.g., SOL, USDC, or other stablecoins). Simultaneously, memecoin stakers also receive additional memecoin rewards, which are automatically added back to the user's total staked amount, effectively auto-compounding the rewards. This compounding mechanism not only enhances long-term returns but also alleviates market selling pressure on the memecoin, thereby enhancing overall market stability during bearish phases.

Furthermore, to prevent malicious rapid withdrawal behavior, Stake2Earn implements a cooldown period mechanism for unstaking. When a staker requests to unbind, their memecoins enter a preset waiting period (e.g., a minimum of 6 hours). During this time, these tokens do not participate in收益 calculations. If the staker changes their mind and cancels the unstaking request, these tokens are immediately重新计入收益 eligibility. This design ensures reward fairness while also guaranteeing liquidity stability, preventing short-term gaming from affecting the system's收益 distribution.

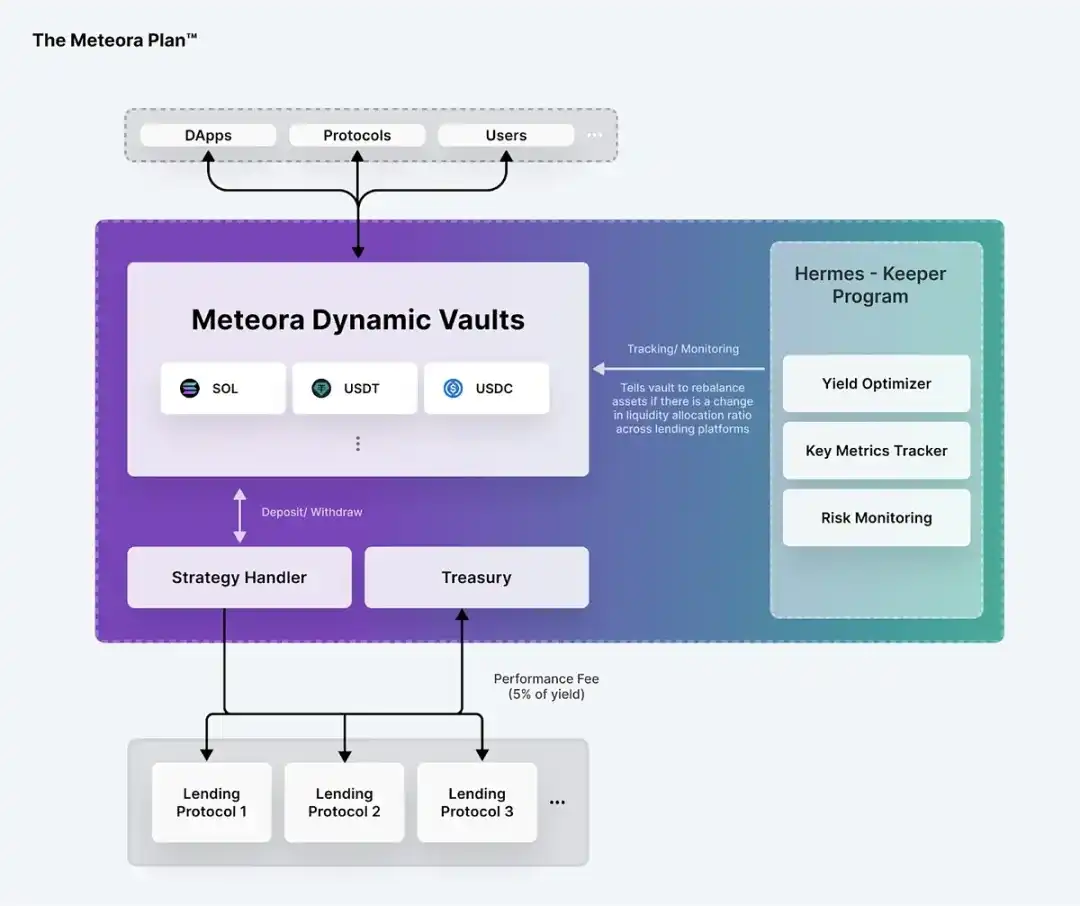

If the incentive system locks in user behavior, then the continuous evolution of the product architecture ensures capital efficiency and safety. Between 2023 and 2024, the team successively released key modules like Dynamic Vaults and the dynamic AMM, further strengthening the protocol's capital appeal in a bear market environment. The Dynamic Vault system employs a minute-level auto-rebalancing mechanism, allocating funds between multiple lending protocols in real-time to find the optimal yield path. When a lending platform's utilization rate is too high or risk indicators are abnormal, the system automatically withdraws funds and reallocates assets, thus protecting LP funds. This structure is not simple yield aggregation but introduces risk parameter judgment and fund dispersion logic, building a dynamic risk buffer layer. Related mechanisms have been audited by institutions like Quantstamp and Halborn and have withstood the test in volatile market environments, enhancing user trust.

The dynamic AMM automatically connects LP-provided funds to the Dynamic Vault system, allowing liquidity to earn not only trading fees but also lending interest and liquidity mining rewards, forming a multiple收益叠加 structure. Capital no longer sits statically in the pool but achieves yield maximization under controlled risk. Simultaneously, Meteora延续 and optimized the multi-asset stable pool technology from its predecessor Mercurial, allowing non-homogeneous assets to be efficiently aggregated in the same pool, such as混合 liquidity structures for Allbridge or Wormhole bridged assets with SOL/USDC. This design improves the liquidity efficiency of cross-chain stable assets and maintains a high capital turnover rate even in market environments with declining overall trading volume.

On-chain data observations confirm that this dual structure of product and incentives has indeed produced practical effects. After the points system launched in early 2024, TVL jumped from approximately $40 million to $160 million in a short period and subsequently entered the hundreds of millions of dollars range. During the same period, compared to Solana's mainstream DEX Raydium, Meteora's TVL decline was relatively smaller, and its recovery速度 was faster. In terms of trading activity, its 30-day trading volume remained at the billions of dollars level, indicating that liquidity did not significantly流失 due to the bear market. The lock-up structure and auto-compound mechanism reduced the speed of capital outflow, while dynamic fees and capital efficiency optimization enhanced the motivation for capital retention.

Overall, Meteora's survival and growth in the bear market do not rely on a single "流量红利" or short-term subsidies. Instead, it has built a sustainable flywheel model through product mechanism innovation, incentive structure reconstruction, real yield driving, and community协同 governance. The biggest启示 for other projects in a bear market cycle is: Rather than using high emissions tokens to exchange for短暂 TVL, it's better to build cash flow capabilities around real trading demand; Rather than amplifying market sentiment, it's better to optimize the internal value capture path of the protocol; Rather than worrying about user流失, it's better to transform users from "liquidity mercenaries" into "interest community members" through long-term locking, profit sharing, and behavior binding mechanisms.

The bear market truly tests not fundraising ability, but whether the product and mechanism can self-sustain. Meteora's practice shows that only when protocol revenue, user收益, and token value form a closed-loop联动 can a project possess the structural resilience to weather cycles. This strategy, prioritizing efficiency, real收益, and sustainable incentives, provides a clear evolution direction for all DeFi projects in a bear market: reduce external输血, strengthen internal circulation, and buy time with mechanisms, not subsidies.

VII. The Liquidity Battle: Different Offensive Paths of DeFiTuna and HumidiFi

Within the Solana ecosystem, competition围绕 liquidity and order flow continues to heat up. Besides Meteora, DeFiTuna and HumidiFi are争夺 market share through截然不同的 paths. The former emphasizes product structure and functional innovation, attempting to attract professional users with more complex on-chain trading tools; the latter adopts a "Prop AMM" model, establishing advantages in quality of execution and trading efficiency through internal capital高效周转 and deep routing integration.

DeFiTuna (TUNA) positions itself as an advanced concentrated liquidity DEX on Solana, employing a hybrid AMM architecture and integrating on-chain lending capabilities into the same protocol framework. Its mechanisms support both Orca AMM and native DeFiTuna AMM dual-path liquidity, and it率先 introduced链上限价单 (limit order) functionality in the Solana ecosystem, allowing users to execute more refined trading strategies without custody.

Furthermore, DeFiTuna deeply integrates leveraged trading with its lending system, enabling leveraged management within the same protocol, providing an integrated capital efficiency solution for LPs and borrowers. This structural innovation gives it certain appeal among professional traders and high-frequency strategy users. However, in terms of scale, its liquidity is still in the development stage. According to DefiLlama data, DeFiTuna's current TVL is approximately $4.1 million, with a近 30-day trading volume of about $115 million. Compared to leading protocols, its market depth and brand recognition仍有提升空间, and the long-term retention effect of its new features remains to be verified over time.

In contrast, HumidiFi (WET) takes a completely different route. As a proprietary market maker model (Prop AMM) on Solana, all of HumidiFi's liquidity is provided internally by professional market making teams. It is not open to the public, and there are no external LPs in the traditional sense. The protocol has no official front-end interface and is primarily accessed through router aggregators, with deep integration with Jupiter being particularly crucial. Relying on its private liquidity pool structure, HumidiFi can achieve tighter spreads and lower slippage, especially suitable for large-volume trading needs. Since its launch in mid-June 2025, its transaction volume has rapidly climbed, exceeding $15 billion in the past 30 days, and it once handled 35%–40% of Solana's trading volume. In statistical terms, its TVL is often recorded as 0 due to the absence of publicly locked assets, but this does not affect its actual liquidity depth at the execution level.

Essentially, HumidiFi is closer to a "dark pool" trading model, sacrificing openness and visible liquidity for better execution efficiency and capital turnover rate; whereas DeFiTuna represents an extension of the open DeFi architecture, attempting to提升 the complexity and capital efficiency of on-chain trading through structural innovation. The two切入 from the dimensions of "product capability" and "capital efficiency" respectively, jointly intensifying the competition for liquidity and order flow on Solana and also presenting more diversified and targeted challenges for Meteora.

Conclusion

Looking at the overall experience, in Meteora, I see both technological ambition and community cohesion. From DLMM, DAMM to Dynamic Vaults and liquidity locking, each product iteration feels like witnessing an upgrade in capital efficiency firsthand; "Meteora distinguishes itself from traditional AMMs through dynamic fee adjustments, liquidity configuration, and mechanisms designed for fair launches." Transforming from a liquidity tool to an ecological hub, making itself indispensable within the ecosystem—this is likely the key to its achieving stable profitability.