In 2026, using stablecoins to purchase U.S. stocks has become a mainstream trend. However, behind the statement "buying U.S. stocks with USDT," various products, while all claiming to provide users exposure to U.S. stock markets, are actually selling completely different assets. Some products convert U.S. stock economic exposure into on-chain tokens; some offer perpetual contracts tracking U.S. stock prices; and others provide real U.S. stock buying and selling services through licensed brokers. The three categories differ entirely in terms of risk-return profiles, rights structures, and underlying logic.

I. Overview of U.S. Stock Trading Platforms

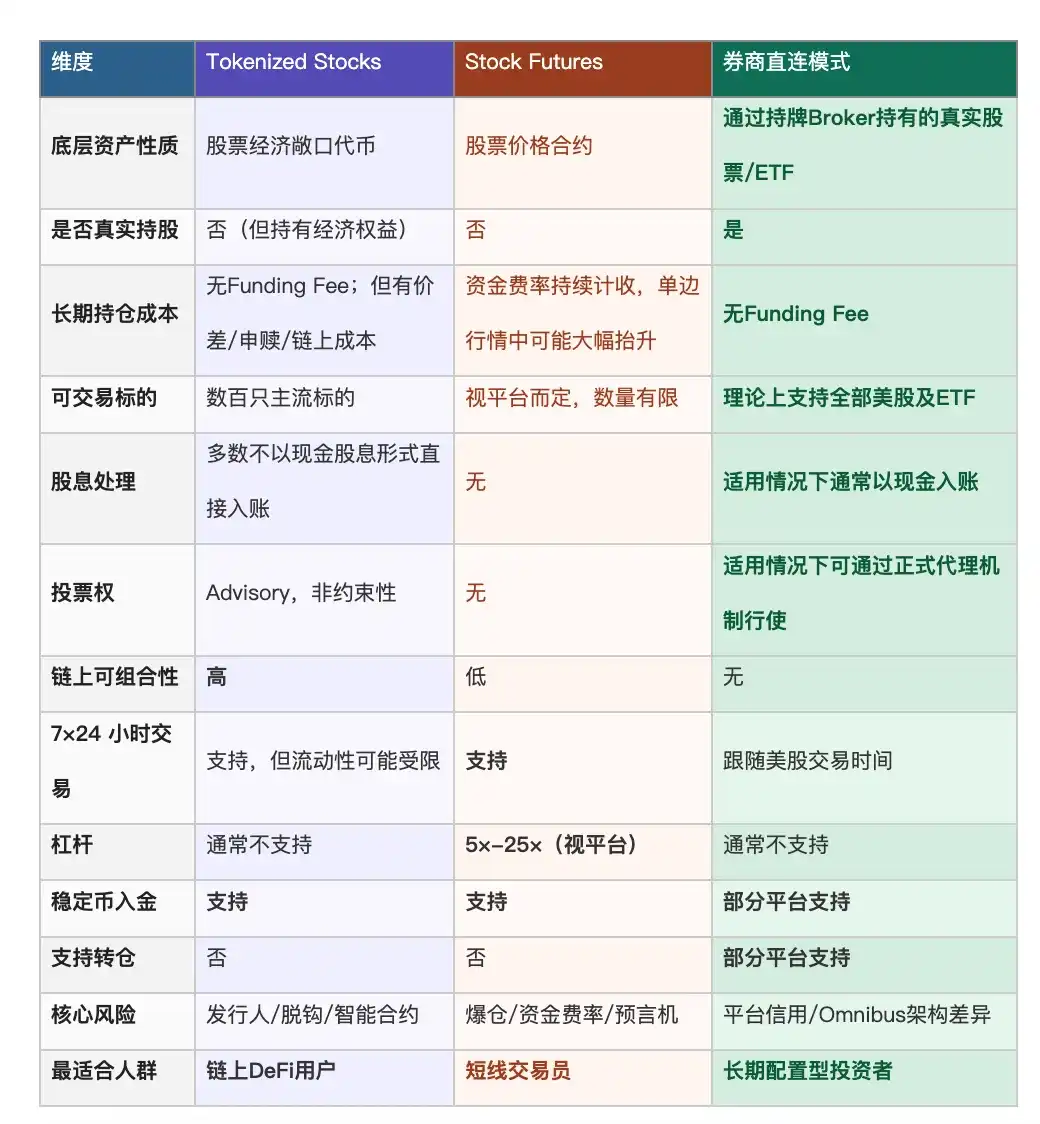

The mainstream solutions for "buying U.S. stocks with USDT" in the current market can be clearly categorized into three types: Tokenized Stocks, Stock Futures, and the Brokerage Model.

1. Tokenized Stocks

Tokenized Stocks are typically held by the issuer or its SPV/custody arrangement. Users hold the economic rights represented by the on-chain token, not the direct shareholder status in a traditional securities account. The most representative issuer, Ondo Finance, has seen its TVL surpass $10 billion, supporting over 200 mainstream stocks and ETFs; the overall market size has reached tens of billions of dollars.

2. Stock Futures

Stock Futures are the most efficient trading instruments but are the furthest from "holding U.S. stocks"—users purchase a price contract with no legal connection to stock ownership.

In 2026, many mainstream trading platforms have launched stock-related perpetual/CFD products, with significant differences in the number of underlying assets, leverage multiples, and available regions (approximately 5×-25×). On-chain platforms represented by Hyperliquid HIP-3 / Trade.xyz are also expanding the traditional asset perpetual contract market. Their core value is enabling global traders to express long/short views on traditional asset prices using stablecoins.

3. Brokerage Model

The operation logic of the Brokerage Model is similar to traditional brokers: users execute stock or ETF trades through a Broker-Dealer, and assets are held via the U.S. clearing and custody system. This is the only path among the three models that truly purchases the stock itself. However, it's important to note that significant differences exist among platforms under this model.

Source: Compiled from public information

II. Comparative Analysis of U.S. Stock Trading Products

The differences among the three models are not only evident in trading experience but also in three core dimensions: legal rights, holding cost structure, and regulatory protection.

Source: Compiled from public information

(1) Tokenized Stocks

The essence of Tokenized Stocks is an "on-chain shadow" of stocks—convenient, composable, but with incomplete rights; shareholder status remains with the issuer.

On-chain composability is the true differentiated advantage of this model: tokens can be used as collateral in DeFi lending protocols while earning additional yield, can circulate 24/7 on-chain, and can be purchased fractionally—these are capabilities traditional securities accounts lack. The limitations are equally apparent: shareholder status lies with the issuer, not the user; most platforms do not directly credit dividends in cash; voting rights are advisory expressions without legal binding force. While there is no Funding Fee, subscription/redemption spreads, on-chain Gas fees, and market maker spreads also constitute holding costs.

(2) Stock Futures / Equity Perps

Stock Futures are "price betting instruments" for stocks—efficient, flexible, 24/7, but Funding Fees continuously erode holding costs over time, and they are unrelated to actually holding stocks.

Stock Futures represent the path closest to what crypto traders are accustomed to—margin, take-profit/stop-loss orders, two-way long/short positions. The operational logic is exactly the same as trading BTC perpetuals, just with different underlying assets, operating 24/7 non-stop. The core trade-off is: Funding Fees can significantly increase during one-sided market trends, with annualized costs potentially reaching double digits or even exceeding 100%, acting as chronic bleeding for a "buy and hold" strategy; after closing the contract, there are no shareholder rights, only USDT profits or losses remain.

(3) Brokerage Model

The Brokerage Model is the path closest to "buying the stock"—rights are most complete, long-term holding costs are cleanest, at the cost of sacrificing on-chain composability and 24/7 trading.

The Brokerage Model offers the most complete rights: real stocks, cash dividends directly credited to the account, formal voting rights (where applicable), coverage of thousands of underlying assets. Main limitations are trading hours aligning with U.S. market openings, holdings not being on-chain, and inability to integrate with the DeFi ecosystem. It's important to note that differences in brokerage architecture across platforms directly affect the transmission path of user rights, warranting careful understanding of the specific compliance structure before choosing a platform.

III. How to Define "Real Purchase of U.S. Stocks"

The three paths have distinct characteristics and target audiences. However, for users who wish to conveniently use stablecoins for long-term U.S. stock allocation, the advantages of the Brokerage Model are very direct—each of its core points of difference precisely addresses the most prominent shortcomings of the first two models, including:

Advantage 1: No Funding Fee, Cleanest Long-Term Holding Cost Structure

Real U.S. stock spot holdings do not involve the concept of a Funding Fee. Holding the same underlying asset for a full year, regardless of market sentiment, will not incur additional Funding Fees.

Stock Futures can have annualized holding costs reaching high double digits during strong market trends; Tokenized Stocks have no Funding Fee but involve subscription/redemption spreads and on-chain transaction costs. In comparison, the holding cost structure for real U.S. stock spots is the cleanest among the three.

Advantage 2: Coverage Depth of Underlying Assets, Incomparable by the Other Two Models

The Brokerage Model covers thousands of U.S.-listed stocks and ETFs, far exceeding the approximately 200-260 of Tokenized Stocks and the limited selection of Stock Futures. For users needing to allocate to mid-cap companies, sector ETFs, or REITs, the Brokerage Model is a more reliable method for stablecoin funding.

Tokenized Stocks and Stock Futures primarily cover top, popular underlying assets, offering almost no choice for configuring mid-cap companies, sector ETFs, or REITs. In terms of the number of underlying assets, the Brokerage Model currently has no comparable rival.

Advantage 3: Real Shareholder Rights—A Difference in Nature, Not Degree

Holding real stocks, dividends are typically credited to the account in cash; voting rights, where applicable, can be exercised through formal proxy voting mechanisms (specific rights are subject to account structure and regional restrictions).

Stock Futures possess no shareholder attributes; the so-called voting in Tokenized Stocks is merely "expressing preference to the issuer," lacking legal binding force. The Brokerage Model is the only path among the three that entails shareholder rights at the legal level.

Advantage 4: Stablecoin Funding, Reducing Dependence on Traditional Banking Channels

Some brokerage platforms support USDT/USDC deposits and withdrawals, reducing reliance on traditional USD wire transfer paths. For users without overseas bank accounts, this represents a substantive lowering of the entry barrier.

Traditional Hong Kong and U.S. stock brokers generally require bank wire transfers, which is troublesome without an overseas account. Supporting stablecoin funding is currently the most practical advantage of platforms offering this functionality.

Advantage 5: Holdings Transferable, Open Exit Path

Under the Brokerage Model, if the platform supports standard securities transfer mechanisms like ACATS / DTC, users can directly migrate positions to other licensed brokers without first selling and then re-establishing positions. This means the exit path is open; users are not passively locked in due to platform changes.

Tokenized Stocks can only be redeemed for stablecoins; after closing a futures contract, only USDT remains—neither offers the option of position transfer. The ability to transfer holdings means users are not passively tied to a single platform.

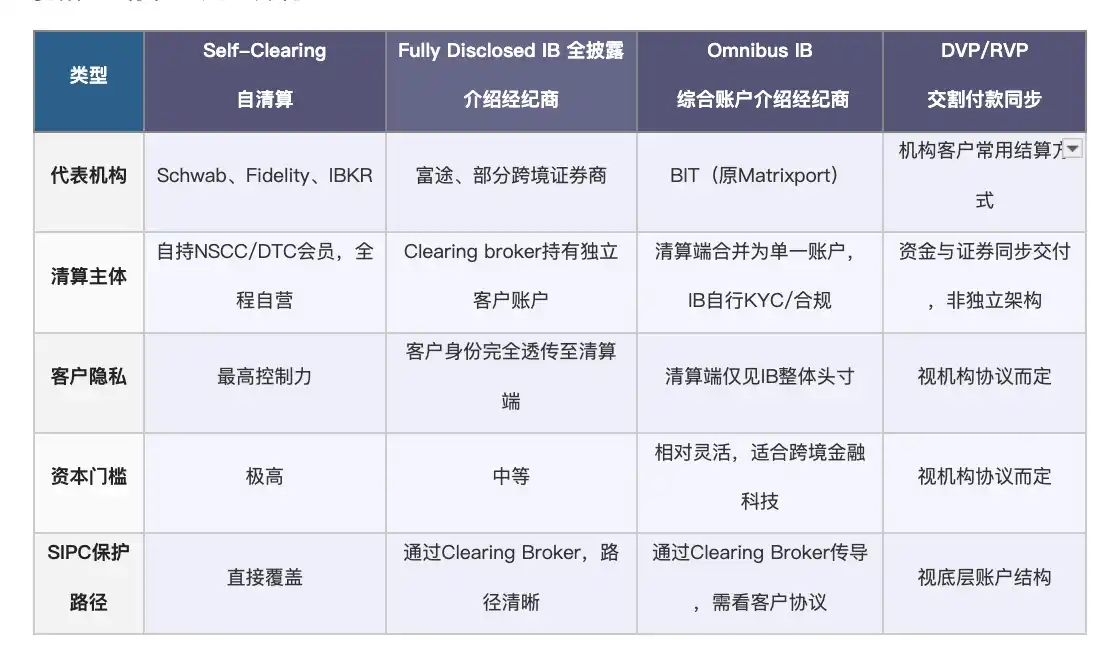

However, the "Brokerage Model" is not monolithic. Platforms claiming to offer "real U.S. stocks" may have vastly different underlying broker architectures—this directly determines where user assets are held, how SIPC protection is transmitted, and whether users can effectively assert their rights if platform issues arise.

U.S. stock trading may appear to be completed on the NYSE or NASDAQ, but what truly determines the change in fund and securities ownership is the SEC-regulated clearing and settlement system. This system centers around the DTCC: the DTC (Depository Trust Company, custodizing assets exceeding $100 trillion) is responsible for the final settlement of nearly all U.S. stock trades.

The system's core mechanism is CCP novation (Central Counterparty Contract Substitution)—after any trade is executed, the NSCC immediately becomes the central counterparty for all trades. The central counterparty mechanism reduces direct counterparty risk arising from broker bankruptcy. The key is that user assets entering this clearing system share the same underlying infrastructure as clients of large, established brokers—not on any public blockchain, not in custom platform accounts, and not reliant on the platform's own balance sheet.

Currently, there are four mainstream architectures in the industry for accessing the clearing system, with differentiation in capital requirements, customer identity disclosure, and SIPC transmission paths:

Source: Compiled from public information, note: DVP/RVP are settlement methods commonly used by institutional clients and are not directly comparable with retail brokerage architectures.

For users:

- Fully Disclosed IB: Customer identity is fully transmitted to the Clearing Broker; the SIPC protection path is clearest; suitable for users valuing legal certainty.

- Omnibus IB: Only the IB's aggregate position is visible at the clearing level; SIPC protection is transmitted through the Clearing Broker, with the specific path depending on client agreements—this is a common access model in international cross-border securities services.

- Self-Clearing: Directly holds NSCC/DTC membership; protection is most direct, but capital requirements are extremely high, typically only met by large, established brokers like Schwab, Fidelity, or IBKR.

Therefore, when a platform claims to offer "real U.S. stocks," the question worth asking is: Through which architecture does it access the U.S. clearing system? At which layer are user assets protected?

Taking BIT (formerly Matrixport) as an example, its compliance architecture consists of three layers:

- First Layer, GMC License: addresses the question "Are user assets segregated?" The Bhutan GMC license imposes strong core requirements regarding the segregation of client funds from proprietary funds. User funds are custodied by independent institutions and subject to audit. This means BIT cannot use user stocks for the platform's own financing or positions—this is the first institutional safeguard distinguishing it from opaque platforms and a prerequisite for "real ownership."

- Second Layer, Omnibus IB Architecture: addresses the core question "Where exactly are user assets?" BIT accesses NSCC clearing and DTC depository custody through two U.S.-licensed Clearing Brokers, both verifiable independently via FINRA BrokerCheck: U.S. stocks purchased by users through BIT are ultimately custodied at these two institutions, not held in BIT's own account or the platform's internal ledger. Assets share the same U.S. securities clearing and custody infrastructure as clients of Schwab and Fidelity.

- Third Layer, SIPC Protection: addresses the question "What is the safety net in the worst-case scenario?" Since BIT's clearing institutions are SIPC members, this layer of protection can be transmitted to end-users through account structures and client agreements by the Clearing Brokers, providing statutory baseline protection (specific transmission paths are subject to client agreements).

Source: Compiled from public information

IV. Conclusion

Buying U.S. stocks with USDT—three paths represent three entirely different assets. Tokenized Stocks hold an on-chain economic representation, with shareholder status residing with the issuer; Stock Futures track prices, unrelated to stock ownership; the Brokerage Model is the path to truly buying the stock itself—rights are most complete, long-term holding costs are cleanest. Even within the Brokerage Model, architectural differences determine the actual protection level of assets—whether the underlying clearing institutions and compliance architecture are publicly verifiable is worth careful verification before choosing a platform.

This article is for educational and informational purposes only and does not constitute investment advice. It should not be construed as a recommendation to buy, sell, or hold any security or financial instrument. All investments involve risks. Readers should conduct their own thorough research and consult a licensed financial advisor before making any investment decisions.