Original Author:Four Pillars(@FourPillarsFP)

Original Compilation:AididiaoJP,Foresight News

Key Points

- Collector Crypt (CC) has generated a cumulative total revenue of $635 million, with 90.6% returned to users via instant card buybacks, resulting in a net revenue of only $43 million, a retention rate of 6.7%.

- Total secondary trading volume across all channels is less than $5 million. The share of eBay transactions has dropped from 1.23% to 0.10% (declining for six consecutive quarters).

- Token value capture (burn + buyback) totals only $1.4 million, accounting for 3.4% of net revenue, while operational wallets have off-ramped $45.7 million USDC.

- As volume tripled and shifted towards higher-tier card packs, the net margin was halved from 11.2% to 5.8%. With each step up in denomination, the blended profit margin is further depressed.

- The current ~$535 million FDV corresponds to 7.3x net revenue for a "casino" with a continuously compressing profit margin, only ~420 daily active players, a float ratio of 20.5%, and 72% of insider supply locked until November 2027.

Introduction

You deposit $1,000 into Collector Crypt, open a Grail card pack, and receive a tokenized Pokemon card valued at $1,015 by the platform. It seems you made a profit. Turbo mode automatically activates, selling the card back to the protocol at a 93% buyback rate, and $944 lands in your account instantly. The entire cycle takes just seconds.

This cycle is rapidly repeated by hundreds of wallets, generating $635 million in transaction volume and creating a ~$535 million FDV for the CARDS token. This article will dissect the composition of this volume, whether the collector economy priced into the token is materializing, and how much share of the revenue the token actually captures.

Note: Collector Crypt (abbreviated CC) is an on-chain gacha (loot box/blind box) platform that combines physical collectible cards (primarily graded Pokemon, sports cards, etc.) with NFTs. Users deposit USDC to purchase random card packs at different price tiers ($25 ~ $2500+), open them to receive an NFT card backed by a physical card, and the platform offers an 85%~93% instant buyback (Turbo mode is enabled by default). Users can sell the card back to the platform within seconds to recover USDC, forming a fast loop.

What is this $635 Million Really?

90.6% of the cumulative volume is returned to users seconds later

CC's core product is a gacha machine. Users deposit USDC, purchase random card packs ($25 to $2500, with a $5000 tier in the API not yet public), and receive a card NFT backed by a physical graded card. Each card has an "insured value," and the platform offers 85%–93% instant buyback.

Buyback is the default behavior, not the exception. All 33 machine configurations in CC's API have turboMode: true enabled. Cards are automatically sold back to the protocol, and users receive USDC minus the spread within seconds.

According to Blockworks daily data up to June 13, cumulative revenue is $635 million, of which $576 million was returned to users as card buybacks, leaving net revenue of $43 million, a 6.7% retention rate. Here, "buyback" refers not to token buybacks, but to the platform repurchasing the cards just sold, recycling the same deposit for the next draw.

On the ATH day, June 11, the machine processed $10.6 million in volume, retained $881k, a retention rate of 8.3%.

The DeFiLlama adapter source code confirms this breakdown: dailyFees = pack_purchases + royalties - buybacks. That is, the ~$52 million annualized fees on the dashboard are already net of buybacks. dailyVolume = pack_purchases, representing gross expenditure before the loop, which is the number displayed on protocol volume leaderboards.

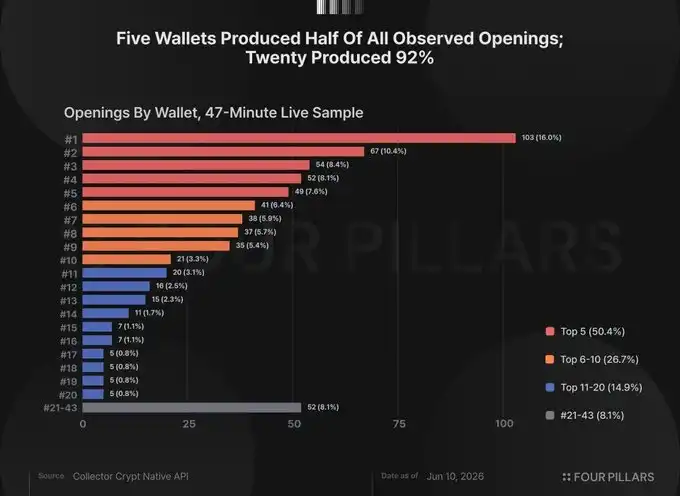

Transaction volume is highly concentrated among dozens of wallets

Blockworks statistics show 23,333 cumulative users. In May 2026, the platform had ~420 daily active users, with a daily average volume of $3.3 million, translating to ~$7,800 per user daily. Even if 400 of the 420 users spent $1,000 each per day, the remaining 20 wallets would still contribute $2.9 million, accounting for 87% of the total volume. Extreme concentration is a mathematical necessity given the averages.

Actual activity corroborates this. We polled CC's public win feed 20 times over a 47-minute window on June 10, deduplicating by NFT address. The sample contained 645 pack openings from 43 wallets. The top 5 wallets contributed 50.4% of openings, the top 10 contributed 77.1%, and the top 20 contributed 91.9%. The single most active wallet contributed 103 openings, 16% of the total.

This is just a 47-minute snapshot, not the full distribution. But both averages and the sample point in the same direction: this $635 million is a casino with a 6.7% retention rate, fed by dozens of high-frequency players at industrial speeds.

The Collector Market Has Not Arrived

The Bull Case

The strongest bull case is worth stating: The buyback loop is the product itself. The draw is the entertainment. An 85%–93% return rate means users lose slowly, and the instant liquidity for vaulted physical cards is a product innovation. As consumer design, it is defensible.

But the machine configuration reveals the direction of design optimization. CC independently controls two variables: the insured value allocated to cards and the buyback rate for automatic resale in turbo mode. Tier ranges and vault inventory are configured so the probability-weighted expected card value is higher than the pack price. The buyback rate then discounts this value below the price.

For example, a $1000 Grail pack shows an expected card value of $1015. The user sees a +1.5% proposition. Turbo mode activates at a 93% buyback rate, returning $944 cash. The card EV is higher than the pack price, which is higher than the cash return. The user sees the former comparison, while the platform profits from the latter. All tiers follow the same structure, achieving edges ranging from 3.2% to 11.2%.

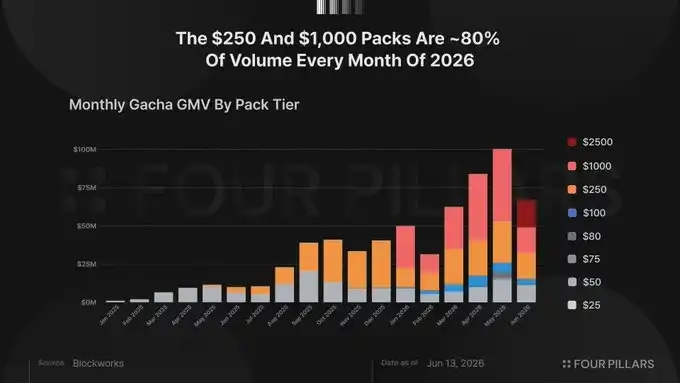

Spending distribution confirms user types. Monthly in 2026, the $250 and $1000 tiers accounted for ~80% of volume (79.4% in Jan, 80.6% in Mar, 79.4% in Apr). Collectors would buy specific cards at specific prices to complete specific sets. The dominance of $1000 random packs is a high-roller distribution.

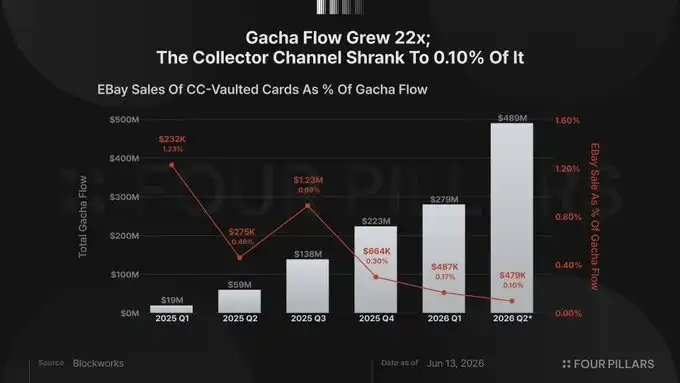

Secondary trading below 1%, eBay share down 12x

If collectors used this platform, they would trade with each other, and cards would flow into the broader market. CC data tracks both, and both are near zero.

On-platform, cumulative marketplace royalties total $133k. Of the $6.9 million lifetime marketplace volume, only $823k is genuine peer-to-peer trading; the rest is buyback flow and V1 legacy volume.

Off-platform, Blockworks tracks eBay sales of CC vault cards. The cumulative total is $3.4 million, but the trend is the key finding. As a share of gacha flow, eBay was 1.23% in Q1 2025, 0.46% in Q2, 0.89% in Q3, 0.30% in Q4, 0.17% in Q1 2026, and 0.10% in Q2 2026. Over the same period, gacha volume grew ~25x. The absolute collector channel has barely moved, while its share has plummeted 12x.

Of the $635 million in card value generated by the platform, only $18.5 million has been redeemed for physical cards, accounting for 2.9%. The remaining 97% was sold back to the protocol via automatic buyback, mostly within seconds.

Combining all channels (eBay + peer-to-peer marketplace trades), total real secondary activity is less than $5 million against $635 million in gacha throughput. The standard bull rebuttal is "it's early," but the quarterly eBay series answers that. The platform is not on an early path towards collector behavior; it has been moving distinctly away from it for six quarters.

Turbo mode eliminates the dwell time — browsing, comparing, collecting — upon which collector platforms monetize and build secondary markets. The design optimizes for loop speed, not discovery. These are two different products.

Token Utility

CC's revenue flows through three layers. Users deposit USDC to buy gacha packs, receive random card NFTs, and in almost all cases, automatically sell them back at an 85%–93% buyback rate. The platform retains the 7%–15% spread as net revenue. Secondary revenue lines include a 2% royalty on marketplace trades and a 2% fee when users redeem NFTs for physical cards. All net revenue flows into the operational treasury, used for card inventory purchases, USDC off-ramping, and a small token buyback program starting in June 2026.

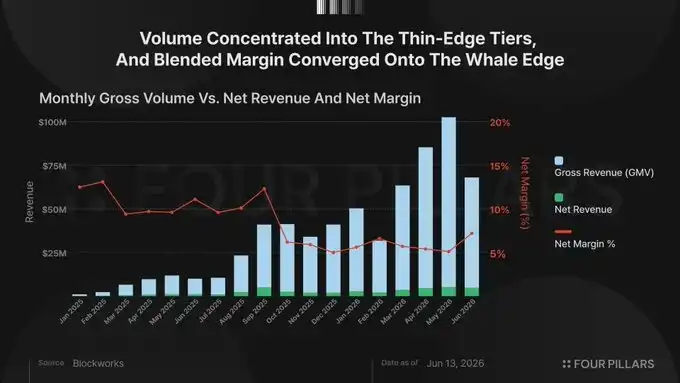

Volume triples, profit margin halves

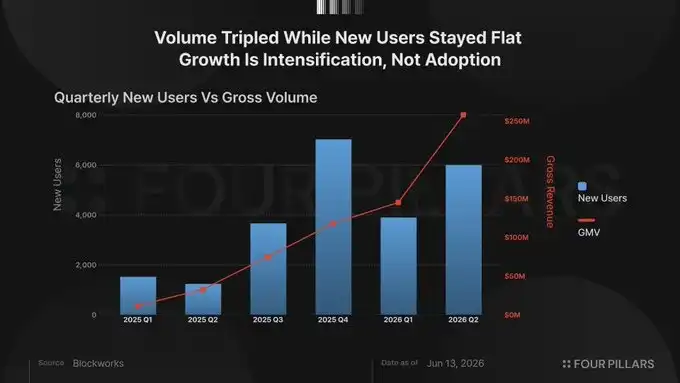

According to Blockworks daily data, in Q3 2025 gross volume was $75 million with a net margin of 11.2%; Q4 gross volume was $116.3 million with a net margin of 5.7%; Q1 2026 gross volume was $145.9 million with a net margin of 5.9%; Q2 up to June 13 gross volume was $256 million with a net margin of 5.8%.

The compression is structural. The thinnest margins are where volume is highest — ~5% for the $250 and $1000 packs versus 9%–11% for the $25 and $50 tiers, because high-volume players won't cycle six-figure sums at an 11% spread. As volume concentrates at higher tiers, the blended margin converges to the high-tier edge. The marginal dollars of growth come from the players from whom the platform retains the least.

The $2500 Mythic pack launched on June 10 has a 6.4% margin. A $5000 Celestial pack already exists in the API (inventory zero). Each step up in denomination continues to grow gross volume while pulling the blended margin toward the lower bound of higher tiers.

User data confirms growth is intensification, not expansion of adoption. New users over the past four quarters were 3,668, 7,013, 3,886, and 5,982 (Q2 up to June 13), roughly flat, while volume more than tripled. May 2026 added 2,593 new users, but daily active users rose from ~280 in April to 420 in May. Most new users churn within days.

Token Value Capture: $55.9k Burned + $887k Buyback

Since launch, 294,203 CARDS tokens have been burned, 0.015% of the supply, worth ~$55.9k over 9.5 months. CC documentation does not specify the mechanism triggering burns, and the downward trend coincides with a market activity crash. In May 2026, 372 tokens were burned; in June, 21 tokens worth $4 were burned.

On June 13, Lukas Ruppert from Maelstrom posted on-chain evidence linking token purchases to wallets associated with CC's operational infrastructure. Ruppert traced from a known CC operational hub (DFEst) through Kraken to DCA bots and identified associated wallets with pack-opening history. He did not fully confirm team control but wrote, "If these wallets are indeed controlled by the team, the significance goes far beyond the purchase itself." The circumstantial evidence is strong.

On-chain traces show two events. On May 12, the CARDS Aggregator wallet paid $500k via Fireblocks custody to pre-seed investor GSR, receiving 4,045,013 CARDS at ~$0.124 each. Then, on June 10 and 11, a newly created wallet funded via Kraken began market-buying CARDS via a DCA bot, two parallel streams of ~$625 and ~$587 every 2–6 minutes. By June 12, the bot had deployed $159k, accumulating 599,104 CARDS, with a remaining budget of $728k.

Calculating all forms of token value capture: Burns ($55.9k), GSR settlement ($500k), full DCA budget including undeployed funds ($887k) totals $1.4 million, 3.4% of the platform's cumulative $43 million net revenue. At the current Q2 annualized rate of ~$73 million, the entire DCA budget equals 1.2% of one year's net revenue.

Wallets identified by Ruppert as CC operational hubs have off-ramped $45.7 million USDC, $8.5 million since May 2026. Regardless of who controls these wallets, the disproportion is noteworthy: $1.4 million flows toward the token, $45.7 million flows away from it. The buyback could be the start of sustained value capture, but simultaneously, the program has nothing on-chain, automated, or committed about it; it could stop tomorrow.

At a 5.8% net margin, massively increasing token buybacks is a zero-sum game with operational wallet income. The buyback rate (85%–93%) determines player cost per spin; lowering it would bleed volume, so the total margin pool is defined by player tolerance. Within this margin, token buybacks and operational off-ramps compete for the same funds.

Even taking things at face value, annualized at the Q2 rate of ~$73 million, the ~$535 million FDV corresponds to 7.3x net revenue for a casino with a continuously compressing profit margin, ~420 daily players, and a revenue base so concentrated that a single wallet exiting could move daily volume by double-digit percentages.

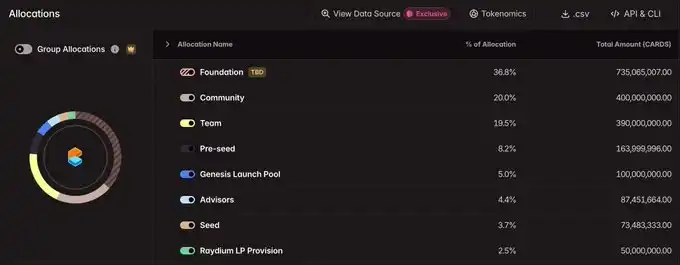

The ~$110 million circulating market cap reflects a 20.5% float ratio, with 410 million of the 2 billion total supply circulating. The remaining 79.5% is locked according to a public schedule until November 2027, with the next unlock on June 29 releasing 28.84 million tokens across four allocations. Insider allocations constitute 72% of supply (Foundation 36.75%, Team 19.5%, Pre-Seed 8.2%, Advisors 4.37%, Seed 3.67%), Community 20%, Genesis Launch Pool 5%, Raydium LP 2.5%.

Conclusion

CC has built a product that puts physical cards into a vault and found product-market fit with a small number of high-speed gamblers. Our view would change if marketplace royalties shifted to genuine peer-to-peer trades, if the eBay share reversed its six-quarter decline, or if the buyback program's scale exceeded 3.4% of net revenue. None of this is currently visible.

What is currently visible: Total token value capture of $1.4 million, 3.4% of cumulative net revenue, against a $110 million market cap ($535 million FDV); $45.7 million off-ramped from operational wallets within the same infrastructure alongside an $887k buyback; the collector channel has shrunk every quarter since launch; and on top of a 20.5% float ratio, insider allocations constitute 72% of supply, locked until November 2027.