Author: Xiao Ba Jiu Ling, Wu Xiaobo Channel

"A plane carrying 'the Jerusalem of the stock market' is flying towards us."

On the evening of May 13, the U.S. presidential delegation formally landed at Beijing Capital International Airport.

In the eyes of stock market investors, what landed was the currently most fervent AI bull market.

Accompanying Trump were the CEOs of 17 major American companies. The combined market capitalization of their companies exceeds $10 trillion, accounting for over one-fifth of the U.S. stock market—essentially half of America's corporate wealth.

Familiar faces like Jensen Huang and Elon Musk need no introduction. Also accompanying the delegation were representatives of the hottest AI hardware companies on Wall Street.

For example, Sanjay Mehrotra, CEO of Micron Technology, whose stock price has surged over 320% in the past year driven by AI storage demand; Another example is Jim Anderson, whose company, Coherent, Inc., is a representative 'optical communication concept stock' on the U.S. market, also seeing its stock price double this year.

Jensen Huang, Elon Musk Arrive in Beijing with Trump

In other words, standing in this delegation is not only Trump, the 'King of K-lines,' but also the 'staunch bulls' of the entire U.S. AI industry.

U.S. stocks also celebrated the visit. That night, the Nasdaq and S&P 500 indices hit record highs, with Tesla rising over 2%, and Nvidia and Apple gaining over 1%, the latter two giants even revisiting their previous market capitalization peaks.

In less than a day, another piece of good news emerged. Just after the A-share market closed, Reuters dropped a major positive report, stating that the U.S. had allowed ten Chinese companies, including Alibaba, ByteDance, Tencent, and JD.com, to purchase Nvidia's H200 chips. When the market opened that evening, Nvidia's stock price directly hit a new all-time high.

Such market movements seem to reinforce investors' current fascination with a particular market logic: "Cutting high for high, the portfolio keeps hitting new highs; cutting high for low, the skill level gets lower and lower."

Cutting High for High, Portfolio Hits New Highs

Generally, during relatively stable market conditions, funds rotate from one sector to another, flowing from overvalued high-flying stocks to undervalued low-flying stocks—this is 'cutting high for low.'

In the experience of investors, after a tech stock rally, profits are rotated into cyclical stocks; when cyclicals tire, dividend stocks take over, ending with pharmaceuticals and consumer staples.

However, over the past month in global markets, funds have not flowed from high-flying sectors to lower-priced assets but have continued chasing the stronger, hotter, more crowded AI direction. This is 'cutting high for high.'

The market is like a snake biting its own tail, single-mindedly rolling from AI-related stocks to more AI-related stocks, ultimately churning out one multibagger after another.

From early April to May 11, in the A-share market, funds flowed from upstream optical chips (represented by Yuanjie Technology, up over 60%) to midstream optical module 'three musketeers'—'Yi Zhong Tian': InnoLight (up over 70%), Zhongji Innolight (up over 55%), and Tianfu Communications (up over 45%).

Subsequently, they moved to PCB printed circuit boards (represented by Shennan Circuits, up over 70%), and finally to downstream AI computing power (represented by Cambricon, up over 90%). Almost the entire AI infrastructure chain saw gains.

U.S. stocks are also moving in this strange cycle: After Nvidia's rally (30%), it's the turn of memory stocks represented by Micron (181%) and SanDisk (100%).

Data from Soochow Securities indicates that as of April 24, the trading volume of the top 5% most-traded stocks accounted for 43.7% of the total A-share market, approaching the critical congestion level of 45%.

Amid the fierce, gap-up trend of 'cutting high for high,' an extreme sentiment has even emerged in the market: "Besides AI, I don't want to buy anything else."

And this is precisely the choice of mainstream capital.

Among the top 50 heavily-held stocks by A-share funds in Q1 this year, 18 belong to the information technology sector. For instance, Zhongji Innolight alone is heavily held by 1,163 funds, and InnoLight is backed by a similar thousand-fund level. Meanwhile, among global hedge funds, the net exposure to the semiconductor industry has jumped from 5.5% last year to the current 20%.

The biggest victims of 'cutting high for high' are naturally those holding other 'non-AI stocks.'

The new world is accelerating its arrival, but not everyone can get a seat on that rocket.

Data from CITIC Securities shows that among stock indices rising over 10% in April, the 'Information Technology + Communication Services' sectors contributed an average of 68.9% to the index gains. Even for weaker-performing indices, the tech sector's contribution to gains was as high as 54%.

In contrast, against the backdrop of the Shanghai Composite Index stabilizing above 4100 points and gaining 5.66% in April, the A-share Food & Beverage (-1.1%), Transportation (-0.7%), and Banking (-0.6%) sectors were among the worst performers, underperforming the broader market.

AI's Exclusive Prosperity

However, even as many indicators warn of the risks of single-sector crowding, no one dares to jump off lightly.

The reason is that people prefer 'cutting high for high' not entirely out of fear of missing out (FOMO) but also due to practical considerations.

Currently, AI is genuinely boosting the economy and corporate profits, becoming, somewhat exaggeratedly, 'the hope of the entire village.'

Taking the U.S. as an example, in Q1 this year, U.S. GDP grew by 2% (excluding inflation). According to *The Wall Street Journal* calculations, the AI economy grew by 31%, while the non-AI economy grew only 0.1%.

Among the components, personal consumption—the largest part of U.S. GDP—grew only modestly by 1.6%; investment in commercial buildings like housing, offices, factories, and transportation equipment like trucks and planes all declined. In contrast, technology equipment investment soared by 43%, software investment grew by 23%, and data center construction investment increased by 22%.

Data Centers Developed by Oracle and OpenAI

Similar patterns are faintly visible within China's economic structure.

In Q1 2026, the profits of high-tech manufacturing enterprises above a designated size, represented by computer communications and equipment manufacturing, increased by 47.4% year-on-year, contributing 7.9 percentage points to the profit growth of all industrial enterprises above the designated size.

In terms of investment, the gap between the growth rate of high-tech industry investment and the overall fixed asset investment growth rate widened from 4.8 percentage points in 2024 to 5.7.

The pull from the AI-related industrial chain is even more pronounced on the export front.

In Q1 this year, integrated circuit exports increased by 77.5% year-on-year, and exports of industrial robots with AI visual recognition and autonomous navigation capabilities grew by 42%, significantly higher than the overall export growth rate.

By April, China's export growth rate further rebounded to 14.1% year-on-year. Among them, integrated circuit exports grew by 99.6%, and automatic data processing equipment exports increased by 47.3%, becoming the core force driving exports.

The import side tells a similar story.

Driven by AI computing power demand, China's integrated circuit import value increased by 45% year-on-year in Q1, further rising to 54.7% in April.

Profit leaders in the capital market are also concentrated in 'AI.'

Estimates show that in Q1 this year, the information technology sector contributed 80% of the profit growth in U.S. stocks. For example, S&P 500 overall profits grew by 15.1% year-on-year, but the 'Magnificent Seven' grew by 61%, while the other 493 companies increased by only 16%.

The A-share market exhibits similar characteristics.

In Q1 this year, the trailing twelve months (TTM) net profit growth rate for AI-highly-related industries like Communications, Electronics, and Nonferrous Metals increased by 60.9% compared to the end of 2023; excluding these three industries, the TTM net profit of other non-financial sectors in A-shares fell by 23.5% over the same period.

AI's exclusive prosperity gives investors the courage to crowd into the trade.

New Story vs. Old Narrative

However, despite the powerful AI narrative, Trump's three-day, two-night visit to China has introduced new variables to the market.

On May 14, the Shanghai Composite Index, after hitting a new interim high of 4258 points during the day, turned downward, closing below 4200 points with a large -1.52% red candlestick amidst a sea of green; the Hong Kong Hang Seng Index also opened high and closed low.

This is a sign of diverging views.

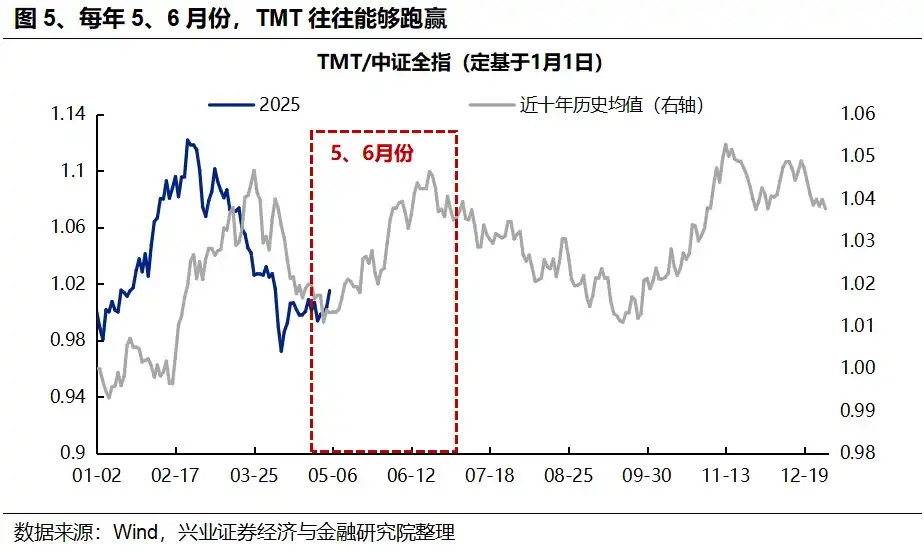

Historically, the period from May to June each year is typically when sector rotation speed converges, implying the market may be incubating a new round of structural themes.

Wall Street is also prepared for this, stating they do not expect a super grand reconciliation but hold high expectations for 'a thawing of relations.'

After all, stepping away from AI, the real world still has many problems to solve, and the keys to solving them lie in the hands of these two superpowers.

Summarizing media reports, potential issues in this U.S.-China dialogue may include the U.S.-Iran conflict, tariffs, critical minerals, U.S. investment, imported agricultural products, etc., each promising to become a new market bellwether.

But this doesn't mean the 'cutting high for high' cycle in AI will stop.

On one hand, according to the calendar effect, the technology sector often outperforms the market in May-June, as this period also sees a higher concentration of important industry conferences.

On the other hand, considering the presence of so many 'AI bulls,' future news flow will naturally favor the 'cutting high for high' proponents, with the Reuters report serving as significant evidence.

Judging from their responses, the future evolution of the market still depends on the correlation of related assets with AI and the degree of impact from geopolitical factors.

Ironically, some views are already contemplating a new logic: As AI becomes the only source of prosperity, more and more industries originally unrelated to AI are beginning to rely on the wealth effects created by the AI bull market.

In other words, consumption, the property market, risk assets, and even domestic demand recovery all need that rocket to keep going up.

Perhaps everything is just as former Citigroup CEO Chuck Prince once said:

As long as the music is playing, you've got to get up and dance.

The subtlety lies in the fact that this statement was made on the eve of the subprime mortgage crisis.

Results of the May Wealth Survey Announced

Finally, we invited 9 investors and financial experts to make predictions and judgments about the market over the next month.

The Monthly Wealth Growth Report is now in its third issue since March. Each month, we conduct a check-up based on the previous month's market trends and invite experts for forecasts.

The major asset classes participating in this month's voting are: CSI 300 Index (representing A-share large caps), Hang Seng Index (representing Hong Kong stocks), U.S. Stocks (AI bubble barometer), U.S. Dollar Index (inflation expectations), Gold Price (safe haven), First-Tier City Property Prices (confidence), Crude Oil Price (geopolitics), CSI Main Consumption Index (domestic demand expectations).

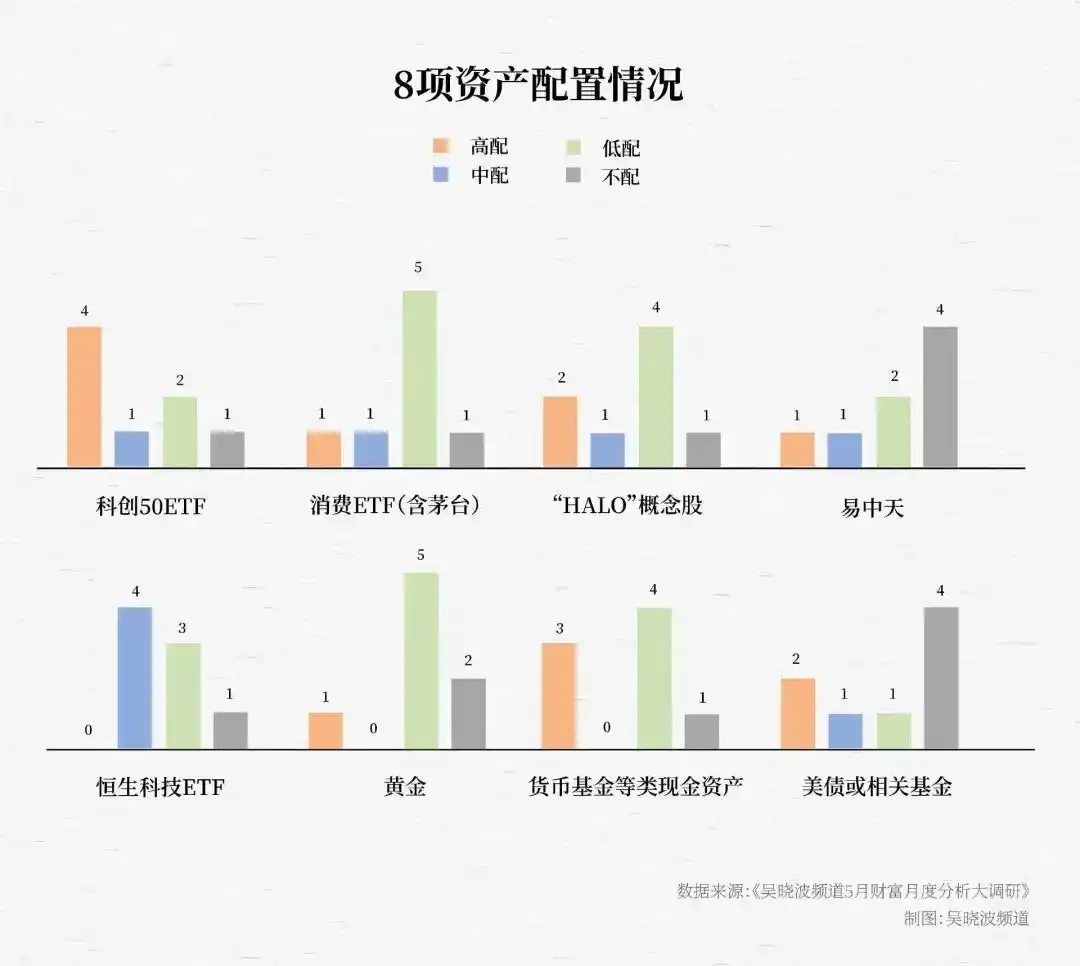

The survey results are as shown:

Furthermore, after the experts completed their assessments of asset upsides and downsides, the next step involves real-money asset allocation. Based on the above eight asset classes, we further selected eight corresponding investment targets and invited them to make allocation choices.

The results show that the most frequently selected assets in the priority ranking outline two clear themes: Technology Growth and 'HALO' Assets.

Specifically, they exhibit the following five distinct characteristics:

▶▷ First, the STAR 50 ETF has become the most favored asset for the third consecutive month.

Experts who are clearly optimistic and choose to overweight it give three reasons:

◎ First, the ChiNext/STAR Market has already demonstrated strong profitability momentum.

◎ Second, the essence of this bull market is a 'technology bull,' with the STAR Market being the main battlefield for new quality productive forces and a key area of support in the '15th Five-Year Plan.'

◎ Third, the STAR 50 Index offers high certainty, superior to specific individual stocks or sectors.

▶▷ Second, the allocation preference for 'HALO' assets has risen again.

Over the recent three months of surveys, expert optimism towards 'HALO' concept stocks has experienced noticeable changes:

In March, HALO concept stocks were favored 6 times. By April, this dropped to 3 times, primarily due to market concerns about overheated sentiment. The situation turned around in May. The enormous energy demands of AI infrastructure have given HALO assets—represented by nonferrous metals, electricity, and energy—a new narrative in the AI era. HALO concept stocks were favored 5 times, again ranking second.

▶▷ Third, most experts choose to avoid the hot assets represented by 'Yi Zhong Tian.'

The core reason is declining win rates. Over the past year, 'Yi Zhong Tian' have each risen 7-10 times, and the optical module sector they represent has reached its highest congestion level in nearly a decade.

▶▷ Fourth, while experts remain cautious about the momentum of consumption recovery, they generally recognize the value of Consumer ETFs for allocation.

Judging by allocation proportions, few experts opt for medium or high allocations to Consumer ETFs; over half choose low allocation, but only 2 chose not to allocate at all.

Experts generally believe the consumption sector has barely participated in the bull market rise and still has catch-up potential; with hot sectors already showing signs of crowding, its cost-effectiveness becomes prominent. Therefore, allocating at this stage is an option that 'loses time but not money.'

▶▷ Fifth, the allocation preference for defensive assets continues to decline.

Over the past three months, the favorability and overall allocation ratio for gold have continuously declined. Most experts are bearish on gold's short-term trend, holding it only as a portfolio allocation.

Views on money market funds and U.S. Treasury bonds have polarized into two camps: One camp generally overweights technology growth assets and underweights or avoids cash-like products. Their reasoning is that the slow, long-term bull market remains solid, and the market will continue its upward charge, thus favoring shifting funds to high-volatility targets.

The other camp overweights cash products and underweights or avoids tech products. Their reasoning is risk control: "Allocating at relatively high levels of prosperous assets makes it hard to find cost-effective directions; now is not the time to add positions."