Written by: Bao Yilong

Following a record-breaking IPO, SpaceX's massive $25 billion bond issue encountered heavy selling in the secondary market. The aggressive financing pace of this long-unprofitable rocket and artificial intelligence company quickly backfired on investor confidence, causing its bond spreads to widen sharply, directly approaching speculative-grade (i.e., "junk") levels.

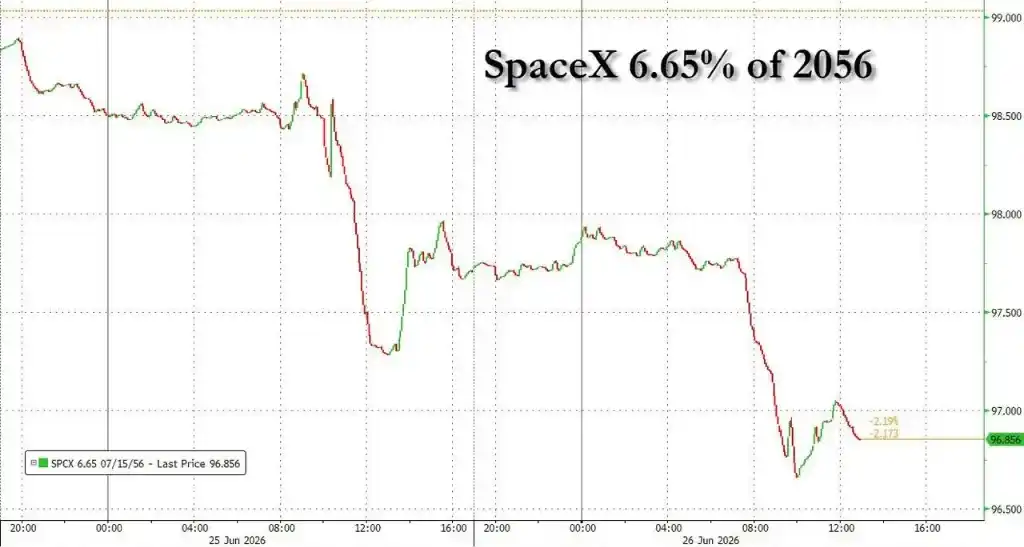

By Friday, SpaceX corporate bonds had turned from "hot demand" on the book to a full-blown sell-off within just 48 hours of pricing.

Selling pressure across SpaceX's various maturities led to cumulative book losses of approximately $400 million compared to U.S. Treasuries, completely erasing the spread tightening achieved by underwriters during the book-building stage with the declines in the long-end bonds.

According to MarketAxess data, SpaceX's 10-year bond yield rose to nearly 6%, with the spread over U.S. Treasuries widening to more than 1.6 percentage points. The spreads on its long-end bonds maturing in 2046 and 2056 surged to 1.93 and 2.01 percentage points, respectively.

According to Ice Data Services, the current market's average spread pricing for BB-rated "junk bonds" is 1.67 percentage points, meaning that with its Baa1/BBB investment-grade rating, SpaceX's actual trading price is significantly worse than that of some junk-grade issuers.

The magnitude and speed of the plunge shocked fixed-income market traders. Market participants noted that among recent mega bond issues, it's almost impossible to find a precedent where spreads widened so rapidly to such an extent.

"Perfect Storm" Hits Secondary Market

The initial book data for SpaceX's bond issue once masked the underlying risks.

According to Bloomberg, the deal initially garnered nearly $90 billion in subscription orders, nearly 4 times oversubscribed, and the issuance size was subsequently increased from $20 billion to $25 billion.

However, traders revealed that this frenzy was mainly driven by fast money seeking short-term arbitrage, not traditional buy-and-hold investors. When these funds tried to take quick profits in the secondary market, selling pressure surged.

Tony Trzcinka, portfolio manager at Impax Asset Management, said the market had anticipated a widening of SpaceX's spreads, but the current magnitude constitutes a "perfect storm."

He pointed out that this stems from the company's significant market cap decline since the IPO, the technical selling pressure brought by the increased issuance size, and investors still grappling with how to price its unique risk profile.

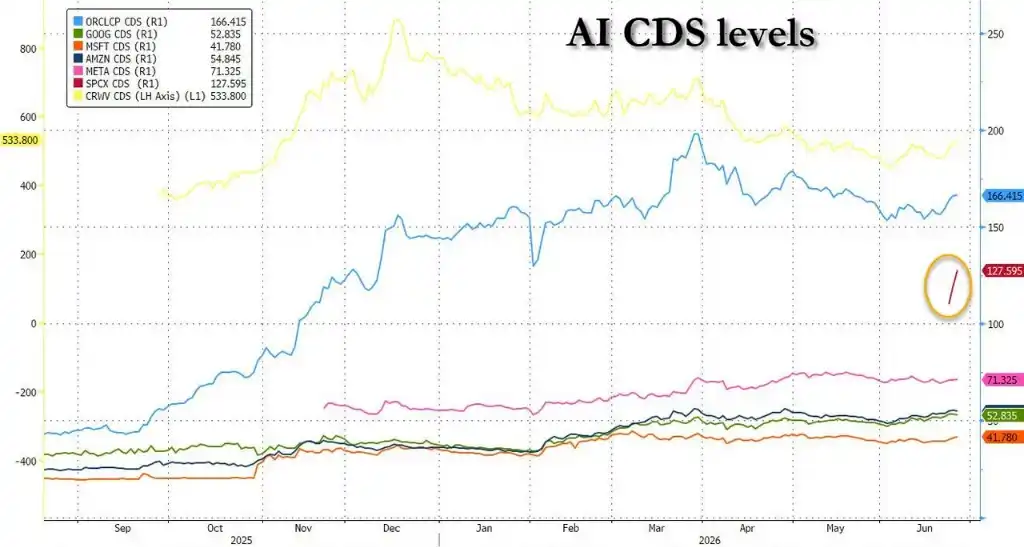

In contrast, Nvidia, which recently completed a $25 billion bond issue, saw its long-end bond spreads widen by only 11 to 12 basis points, while Alphabet's long-end spreads even narrowed.

Additionally, SpaceX's credit default swaps (CDS) widened significantly after trading began, further confirming the market's defensive stance towards its credit.

Cash Flow and Governance Risks Spark Direct Concerns

Stock and bond investors have fundamentally different logics for evaluating SpaceX.

The company raised $86 billion through its IPO earlier this month, with its valuation once reaching nearly $3 trillion before falling back to $2 trillion. This valuation is largely built on expectations that its AI revenue will surge in the future.

However, for creditors, the core fact is that while SpaceX achieved $18.7 billion in revenue in 2025, it recorded a net loss of $4.9 billion. PGIM portfolio manager Michael Campion stated:

In the investment-grade bond market, we focus on whether a company can repay its debt. We are accustomed to lending based on actual cash flows, not expectations.

Allianz Chief Investment Officer Ludovic Subran also remarked bluntly:

Bond investors are different from equity investors. Equity investors might go to Mars with you, but bond investors will just ask, 'Where's my coupon?'

Furthermore, the extreme reliance on Musk's personal leadership has become a core concern for rating agencies and investors. Fitch Ratings sees this as a "key rating constraint."

Professor James Dow of the London Business School pointed out that SpaceX is currently highly reliant on Musk, lacks a succession plan, and has exceptionally weak corporate governance, which significantly reduces the appeal of its long-term debt.

Tech Giant Bond-Issuance Wave Nears "Bubble" Territory

The cold reception faced by SpaceX is not an isolated incident but exposes systemic vulnerabilities in the current tech giant debt expansion.

As tech companies race to raise huge sums to fund AI projects, investors are facing a massive supply shock of bonds.

According to Morgan Stanley data, AI-related debt issuance this year has reached $236 billion, a 357% year-over-year increase, and is projected to double to $570 billion by year-end.

The borrowing frenzy is rapidly pushing up industry leverage ratios. Data shows that the total leverage ratio of mega-tech companies has doubled in just over two quarters, skyrocketing from 0.9x to 1.8x, already exceeding the total leverage ratio of the entire energy sector.

This massive supply is overwhelming the market structure. Bloomberg calculations show that as of Wednesday, U.S. investment-grade bond supply for June has reached $180 billion, a record high.

The supply glut has begun to weigh on broader credit spreads. Morgan Stanley notes that spreads for mega-size issuers are widening overall, a trend confirmed by the performance of bonds from Oracle and Meta.

In a report, Mark Dowding, Chief Investment Officer of Fixed Income at RBC BlueBay Asset Management, wrote, bondholders have clearly concluded that future debt issuance could be significant as this unprofitable company finances its path to future profitability.

Analysis suggests that if this pace of debt expansion continues, credit spreads could ultimately break out further, thereby imposing material constraints on tech companies' capital expenditure cycles.