Author: Kuli, Deep Chao TechFlow

My feeling about crypto this year is probably this: watching the U.S. stock market hitting new highs every day, then opening my own portfolio, staying silent for three seconds, and closing it.

BTC has fallen by nearly 20% year-to-date, ETH has performed even worse, and altcoins—let's not even mention them. In such a market, it wouldn't be news if any public chain's token dropped 90%. But even colder than the prices is the feeling of abandonment.

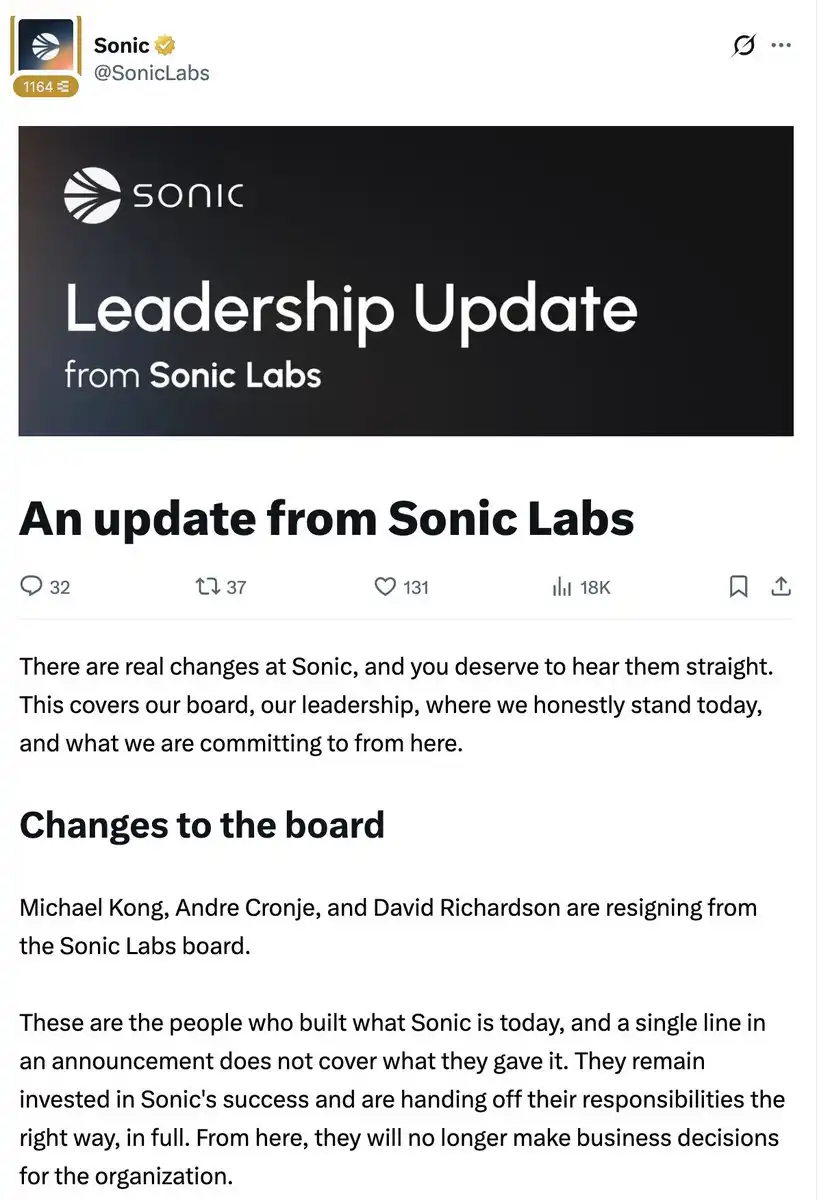

On June 19, DeFi Godfather AC, along with two other founding directors, exited the Sonic Labs board. The S token was trading at $0.028 at the time, just a fraction of its peak of $1.03 at the beginning of the year. On-chain TVL had plummeted from a high of $1.14 billion last May to $20 million. According to DefiLlama data, that's a 98% evaporation.

The industry's reaction to AC's departure was muted. After all, he quit the space once in 2022, only to return later. This exit statement was also standard, saying he "remains bullish on Sonic" but will no longer be involved in business decisions.

But the next part was the real sting.

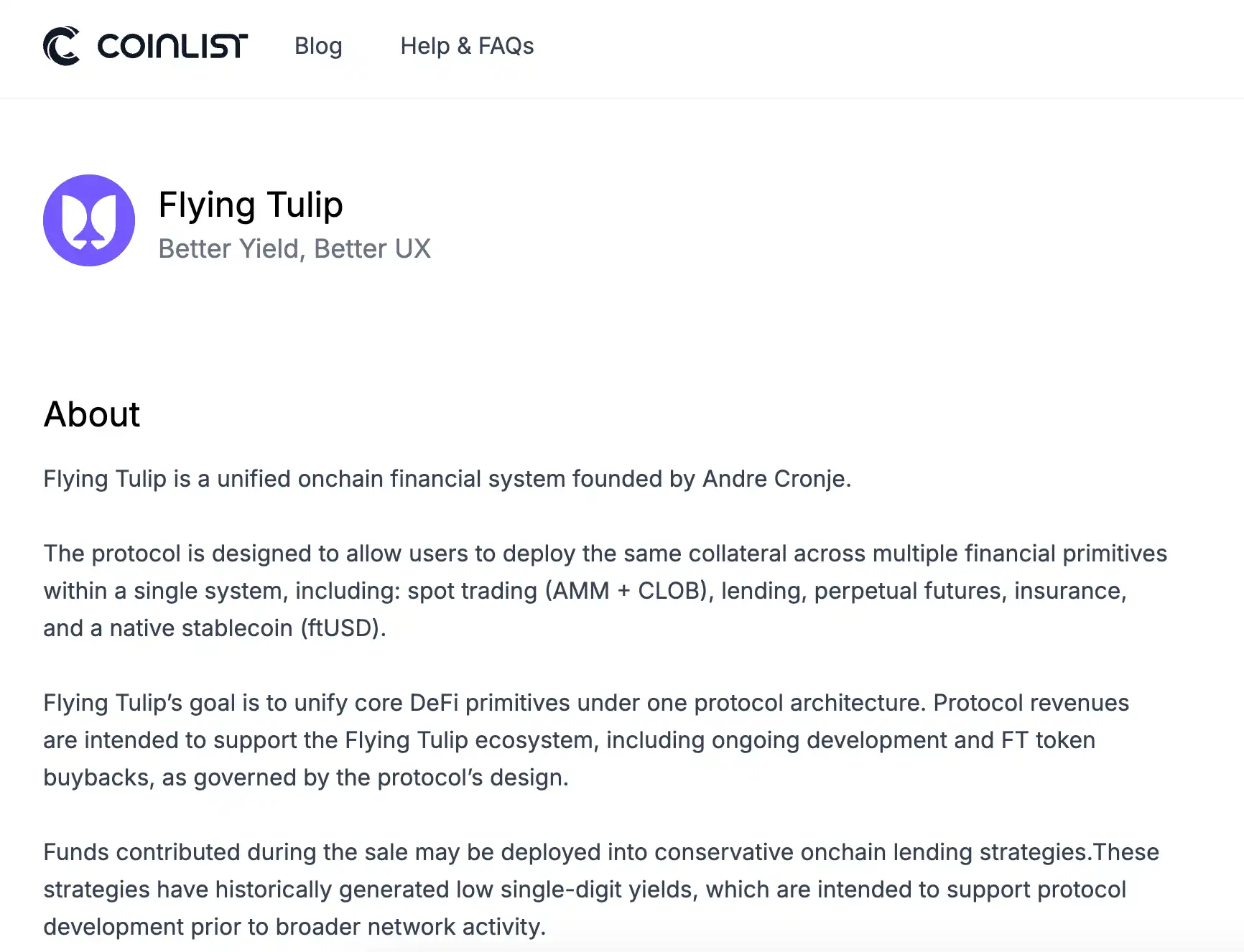

He said his primary focus for the past 18 months has been on Flying Tulip. This project raised a $200 million private placement last August at a $1 billion valuation, and opened a public sale on CoinList this February. The investors include names like Brevan Howard, DWF Labs, and Susquehanna.

In other words, during the exact period S was dropping from $1.03 to $0.028, AC was busy setting the stage for a brand-new billion-dollar project.

The real kicker is Flying Tulip's token design.

Primary subscription investors receive an NFT called ftPUT, which is essentially a perpetual put option. If they incur losses, they can burn the token at any time and redeem their principal at the original price. The CoinList public sale page clearly states, in bold, that the FT tokens (the tradable tokens, i.e., the normal coins) bought on the open market do not carry this right—only primary participants have it.

In contrast, S holders who bought on the secondary market are stuck with $0.028 being $0.028. No floor, no redemption, no safety net written by anyone...

Not My Fault

AC posted his exit statement on X. It was short, but every sentence seemed carefully measured.

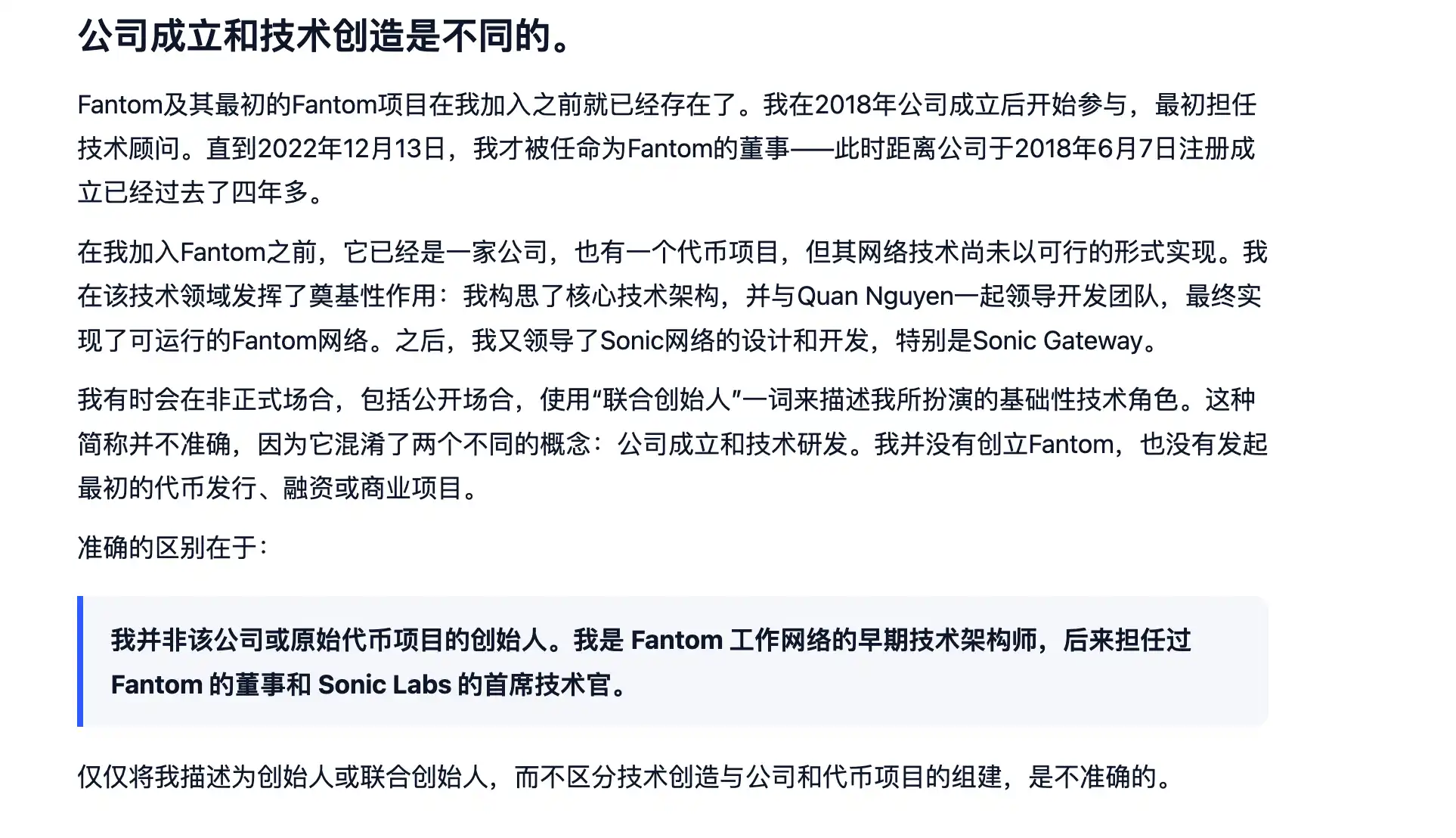

He said he joined Fantom as a technical advisor in 2018 and only formally became a director in December 2022. He was not Fantom's founder, never was, just the earliest technical architect. He was responsible for the underlying technology, including Sonic's core system and cross-chain gateway.

Then came the key paragraph, which roughly translates to:

"I am responsible for the technical decisions I led, but decisions regarding the migration, airdrop, tokenomics, and disposition of the old network—I was not the initiator, nor the final decision-maker."

With one sentence, he absolved himself from the S token's 97% drop. I built the tech, the tech is fine. As for why the coin you bought fell from a dollar to three cents, those were someone else's decisions.

The author won't comment on whether this claim holds water, but one must admit this separation is impressively clean.

When most project founders abandon ship, they either go silent or issue vague statements full of "we" and "the team," diluting responsibility into a murky soup. AC is different. He draws his responsibility boundaries with extreme precision, so precise it's hard to argue, because he indeed didn't manage tokenomics.

And this wasn't a spur-of-the-moment idea.

In March 2022, AC announced his exit from the crypto industry, citing regulatory pressure and burnout. At the time, Fantom's TVL evaporated nearly a third within a week, drawing a torrent of community criticism. He quietly returned a few months later, returning to work on Sonic's technical overhaul.

He left saying he was tired, returned without fanfare, and now leaves again saying, "I've actually been busy with other things for the past 18 months."

As for Sonic? In the half-year before his departure, its executive team was completely overhauled. CEO Mitchell Demeter, hired just last September, resigned in February, along with the head of business. After the CEO left, the board stepped in to manage for a few months. Now the board has also stepped down, replaced by a new CEO, Matt Visser, who has never managed a public chain operation at the front lines.

In five months, the entire management team from top to bottom has been replaced. Sonic's official statement didn't sugarcoat it either, directly stating, "The token price dropped, community sentiment dropped, we're not going to pretend it didn't happen."

This kind of "hands-up honesty" is rare in the crypto industry. But the problem is, the ones telling the truth are the new team, while the one leaving is the one whose name carries value.

The Script for a Strategic Retreat

Looking back at AC's trajectory over the past few years reveals a pattern.

2020: Wrote Yearn Finance, the iconic product of DeFi Summer, with TVL once soaring to tens of billions of dollars. He essentially let it go not long after, and Yearn ran on its own. It ran okay, but it had little to do with him anymore.

Next, he worked on Fantom's technical architecture. Fantom rallied for a while. In March 2022, he announced his exit. Fantom subsequently entered a long, slow decline, later rebranding as Sonic and relaunching. He returned with a CTO title. Sonic's TVL initially broke through a billion but then collapsed all the way down to its current state.

Every time, he disengaged at the peak of hype or just as it started cooling, moving on to the next thing. Every time, holders of the old project bore most of the decline after his departure.

Flying Tulip is his fourth project to date. The author thinks this time, he might have truly absorbed the lessons from previous experiences and baked them into the token design.

When you participate in Flying Tulip's public sale on CoinList, spending $0.10 to buy an FT, you don't receive the token directly. Instead, you get an NFT called ftPUT, with the token locked inside. This NFT is that perpetual put option. You have three choices.

First, do nothing. The token remains in the NFT, non-tradable, but the redemption right persists. Whenever you want to leave, burn the token and get your USDC or ETH back at the original price. Regardless of how low the FT price falls on the secondary market, your principal has a floor.

Second, extract the tokens from the NFT to trade freely. But the moment you extract them, the redemption right is permanently forfeited. The principal corresponding to the extracted tokens is released to the protocol for buyback and burn.

Third, extract some, keep some. The portion kept in the NFT continues to have protection; the extracted portion goes naked.

AC himself said something very interesting in an interview with The Block, the gist being that because of the perpetual PUT's existence, the funds raised essentially cannot be spent at all.

The net funds raised are zero. So where does operating capital come from?

All raised capital is placed into lending protocols like Aave and Ethena for conservative strategies, targeting around 4% annual yield. Based on a full raise of $1 billion, this would generate approximately $40 million in interest annually. This money funds the team, development, and buybacks. The team has no initial token allocation; all FT tokens must be bought back by the protocol from the open market using protocol revenue.

The author must admit, this design is quite ingenious within DeFi. It addresses the foulest problem in the crypto industry in recent years: project founders taking the money and running, or spending it recklessly, leaving investors with nothing. AC's solution essentially ties his own hands: the money can't be touched, the team gets no pre-allocated tokens, and investors can exit at any time.

But ingenious as it is, this protection exists only in the primary market. Once FT is listed on exchanges, tokens bought on the secondary market do not come with ftPUT. This sentence is written in bold on CoinList's page.

Buyers on the open market see the same token but receive completely different treatment.

A Microcosm of the Industry

Money is flowing out of the crypto market this year—that's no secret.

BTC has fallen nearly 20% year-to-date, and the median drop for altcoins far exceeds that. People in the circle look at the Nasdaq hitting new highs, then switch back to their own holdings—the feeling needs no description.

Many people's real strategy this year has been slowly shifting their positions into U.S. stocks and stablecoin yield products. On-chain activity is visibly shrinking.

In this environment, AC's exit from Sonic is just the tip of the iceberg. The entire L1 sector is experiencing the same story: TVL contraction, user attrition, founding team changes, or direct disappearances. Sonic just gets highlighted as a case study because of its fame and extreme decline.

But AC's case has a layer other projects lack.

Flying Tulip's current valuation is about $1 billion. Sonic's current market cap is about $100 million. The same person, the same period, one at $1 billion, the other at $100 million—a tenfold difference. What's the distinction? The distinction lies in which project AC's name is attached to.

This is a fact few in the DeFi industry are willing to voice openly.

The valuation of many projects isn't built on revenue, users, or technological moats—it's built on a person's name. The name stays, the money stays. The name leaves, the money follows.

The bear market ripped off this fig leaf. In a bull market, all L1s rise, making it hard to distinguish whether fundamentals or a name is propping it up. When the tide recedes, what remains becomes clear.

There's one more detail the author finds most interesting.

Flying Tulip's primary deployment chain is Sonic. AC exited Sonic's board, no longer involved in any business decisions, but his new project's first stop is on Sonic. He's gone, but his business remains.

The captain has disembarked, but opened a new shop on the dock, selling things more expensive than what was on the ship.