Original Text by Li Hailun, Tencent Technology

Oracle delivered a record-breaking financial report. However, behind the data growth, AI cloud orders are driving up the company's data center investments and capital expenditures, turning its annual free cash flow negative.

On June 10th, U.S. time, Oracle released its financial report for the fourth quarter of fiscal year 2026 (corresponding to February 2025 to May 2026) and the full fiscal year ended May 31, 2026.

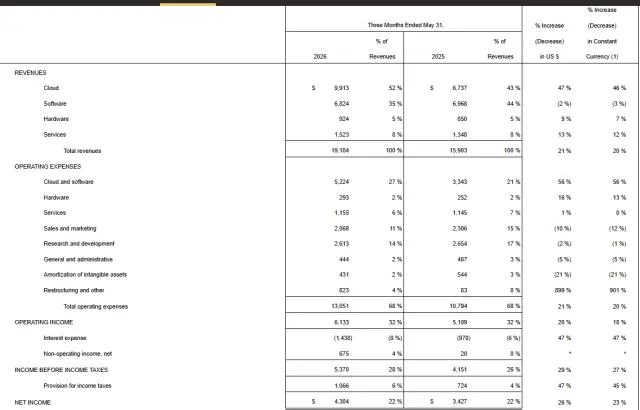

The report shows that Oracle's total revenue for Q4 was $19.2 billion, a year-on-year increase of 21%. Excluding the impact of exchange rate changes, the growth was 20%, exceeding market expectations. According to data from LSEG, analysts had on average expected Oracle's Q4 revenue to be $19.1 billion.

Oracle Q4 Financial Data

Operating profit was $6.1 billion, a 20% increase compared to $5.1 billion in the same period last year; on a non-GAAP basis, adjusted operating profit for Q4 was $8.6 billion, compared to $7.0 billion in the same period last year.

Operating margin was 32%, compared to 33% in the same period last year. On a non-GAAP basis, Oracle's Q4 operating margin was 45%, compared to 44% last year.

Net profit was $4.22 billion, a 23% increase compared to $3.43 billion last year. On a non-GAAP basis, net profit for Q4 was $6.2 billion, a 26% increase compared to $4.9 billion last year.

Diluted earnings per share were $1.45, a 21% increase compared to $1.19 per diluted share last year. On a non-GAAP basis, diluted earnings per share were $2.11, a 24% increase compared to $1.70 last year.

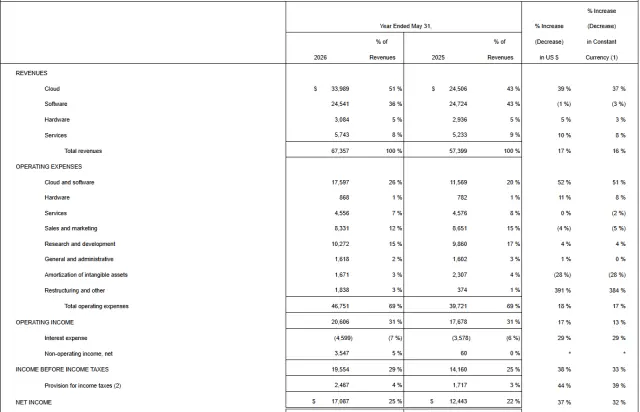

For the full year, Oracle's total revenue reached $67.4 billion, a 17% year-on-year increase, hitting a new historical high. Cloud business revenue for the full year was $34.0 billion, up 39%, while software revenue was $24.5 billion, down 1% year-on-year.

Oracle Full Year FY2026 Financial Data

Net profit for the year was $17.0 billion, a 36% increase. On a non-GAAP basis, net profit was $22.2 billion, up 29%. Earnings per share were $5.83, a 34% increase. On a non-GAAP basis, earnings per share were $7.63, a 27% increase.

Behind the record revenue, AI is pushing up Oracle's revenue ceiling, while also increasing its capital expenditure pressure.

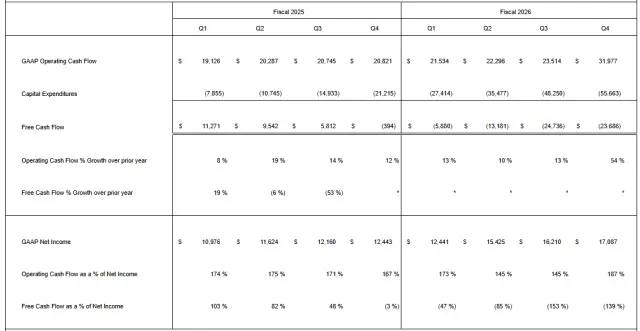

Oracle's full-year operating cash flow for FY2026 was $32.0 billion, a year-on-year increase of 54%. Free cash flow was negative $23.7 billion, with capital expenditures of $55.7 billion.

Oracle also announced a quarterly dividend of $0.50 per share, payable on July 24, 2026, to shareholders of record at the close of business on July 10, 2026.

Following the earnings release, Oracle's stock fell by up to 5% in after-hours trading. Previously, Oracle's stock had risen by 3% year-to-date, underperforming the S&P 500 index, which gained 6% over the same period.

01 Cloud Business Now Constitutes Half of Oracle

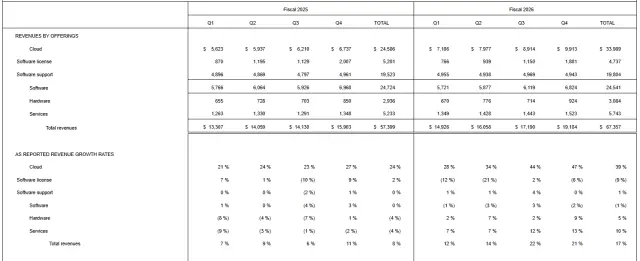

Oracle's cloud business (IaaS plus SaaS) contributed $9.9 billion in revenue in the fourth quarter, a year-on-year increase of 47%, now accounting for half of the company's total revenue.

The true growth driver was the cloud infrastructure business (IaaS), with quarterly revenue of $5.8 billion, a year-on-year increase of 93%. This pace slightly exceeded market expectations of 91% and is considered top-tier within the entire cloud computing industry. The company's annual IaaS revenue reached $18.1 billion, growing by 77%.

Financial Data for Oracle's Business Segments

In comparison, cloud application business (SaaS) revenue in Q4 was $4.1 billion, with a growth rate of 10%, steady but not spectacular.

Meanwhile, the traditional software licensing and support business continued to shrink, with quarterly revenue of $6.8 billion, a 2% year-on-year decline, indicating that the trend of customer migration to the cloud has not stopped. Service and hardware businesses grew by 13% and 9% respectively, but their smaller scale limits their impact on the company's overall trajectory.

Both database and application businesses benefited from Oracle's early adoption of AI. Oracle's multi-cloud AI database revenue grew 404% in Q4, with order volume up 325% year-on-year, becoming the company's fastest-growing business ever. This growth rate, from a product perspective, confirms that AI-related demand is not limited to the infrastructure layer but is also penetrating upstream data management layers.

In the earnings report, Oracle attributed the growth to broad market demand for its cloud technology and application suite. Judging from the changes in revenue structure, Oracle has largely completed its transformation from a database software company to a cloud infrastructure provider, with the computing demand driven by AI being the biggest force behind this shift.

02 The AI Bet Behind the $638 Billion Order Backlog

The most striking number in the report is the Remaining Performance Obligation (RPO), which is the total value of signed contracts not yet recognized as revenue.

As of the end of Q4, this number reached $638 billion, compared to $553 billion a quarter ago, meaning a net increase of $85 billion in three months, with a year-on-year increase of 363%. Wall Street analysts had previously forecasted this number to be around $590-$600 billion, with the actual data far exceeding expectations.

Analysts at Bank of America pointed out a key detail: over half of this $638 billion comes from OpenAI. This means Oracle's largest customer currently is an AI startup that itself is still burning significant cash.

Oracle explained the composition of these orders in its statement. Most of the new RPO comes from large-scale AI contracts, where either the customer prepays for GPU procurement, or the customer purchases GPUs themselves and hands them over to Oracle for deployment. The cumulative value of such contracts where customers bear the hardware cost currently stands at $75 billion. Oracle explained that this arrangement significantly reduces the funding pressure the company would face to build AI data centers itself.

This structure mitigates some of Oracle's financial risks. However, the issue is that if the largest customer itself faces funding pressure, or if overall AI industry demand fluctuates, the highly concentrated order structure itself becomes a risk point.

Reuters analysis suggests that the software industry is facing investor concerns that AI tools might replace traditional software products, which could potentially lure enterprise customers away from traditional software, posing an additional challenge for Oracle.

03 Behind the Massive Orders Lie Heavier Capital Expenditures

Supporting Oracle's $638 billion order backlog is a massive capital investment. Capital expenditures in Q4 were $15.9 billion, totaling $55.7 billion for the full year, significantly higher than Oracle's previous guidance of $50 billion.

Oracle's Free Cash Flow Turned Negative $23.7 Billion

This directly led to a deterioration in free cash flow. Although full-year operating cash flow of $32.0 billion set a new record, after deducting capital expenditures, free cash flow turned negative $23.7 billion.

To fill the funding gap, Oracle raised $43.0 billion through debt financing and $5.0 billion through equity financing in FY2026.

The company also announced plans to raise another $40 billion in FY2027, including the previously disclosed $20 billion in equity financing. Oracle stated that it will not issue new debt in the second half of 2026, but this news did not stabilize market sentiment.

CNBC believes that previous financing moves have already raised investor concerns because of uncertainty about whether market demand for AI can absorb such massive new capital. When the company announced an increased fundraising plan again, these concerns intensified.

Reuters further analyzed that Oracle's performance may intensify investor concerns on two fronts: first, the potential for AI-driven disruption of traditional software demand, which could pull enterprise customers away from the traditional software space; second, the financial risk posed by the high level of debt on Oracle's balance sheet itself.

TD Cowen analyst Derrick Wood pointed out that Oracle's stock price rise prior to the earnings release might be due to investors being more optimistic about the prospects of computing service providers and OpenAI, Oracle's most important customer.

In other words, the market had already accumulated certain gains and optimistic expectations before the earnings release. When the new financing plans and higher-than-expected capital expenditures were made public, some investors chose to reassess risks or take profits, which amplified the stock price correction.

04 FY2027 Revenue Target: $90 Billion

Oracle provided clear expectations for the next phase of growth.

For the first quarter of FY2027, total revenue growth is expected to be between 27% and 29%, with adjusted earnings per share between $1.72 and $1.76. The midpoints of both these guidance figures are above analyst expectations. Additionally, cloud business revenue growth guidance is 57% to 63%, maintaining a high-growth trajectory.

For the entire FY2027, Oracle reiterated its $90 billion revenue target and raised its adjusted earnings per share guidance to $8.05.

The company clarified in its statement that this growth rate is calculated after excluding one-time items from FY2026, such as the sale of the Ampere chip business and Bloom Energy warrant. The actual year-on-year growth rate is about 18%. Analysts had previously expected earnings per share of $8.01 and revenue of $88.9 billion.

05 Focusing on AI Healthcare

Beyond cloud infrastructure and AI computing power orders, Oracle is attempting to extend its AI capabilities into more specific industry applications, with healthcare being one of its emphasized directions.

The Oracle Health application suite will launch an AI-based Cerner hospital and clinic patient care management system, and it is expected that this product will drive the overall growth rate of the health business to double digits in FY2027. Oracle emphasized in its statement that this is just the beginning of the health business expansion.

In its longer-term technological outlook, Oracle believes AI is about to revolutionize healthcare. The company outlined three specific directions: the Oracle Health AI system will reduce doctors' time facing computers, allowing more time for patients; AI molecular design models are expected to enable researchers to accelerate the development of life-saving drugs; a new AI clinical trial system aims to enable regulatory agencies to quickly review and approve clinical trial results, thereby allowing patients to access new drugs faster.

Oracle does not want to be just an AI computing power supplier; it also hopes to embed AI capabilities into specific processes such as medical software, drug R&D, and clinical trials. However, compared to cloud infrastructure orders, this part of the business is still in a much earlier stage, and whether it can truly translate into scaled revenue still requires time for validation.