Written by: Prathik Desai

Compiled by: Block unicorn

In March of this year, OpenAI shut down a feature that allowed AI agents to shop on behalf of users. Since its launch, in just five months, fewer than 30 Shopify merchants had used this feature. The payment infrastructure itself was not the problem; the issue lay in the lack of rules to ensure a smooth shopping experience. Which products could agents purchase? Who was responsible for collecting sales tax? How to identify fraudulent behavior? Who would handle returns—all these questions were not properly addressed.

Providing wallets for agents or building payment infrastructure is relatively easy. However, enabling individuals or businesses to use agents for consumption in a trustworthy and regulated manner is not. Only programmability and rules can ensure a trusted environment. This governance-level gap presents an opportunity for the agent economy.

Last year, AI agents processed 176 million transactions, totaling $73 million. While this number might seem insignificant now, McKinsey predicts that by 2030, AI agents will facilitate $3 trillion to $5 trillion in global consumer commercial transactions.

Companies building this economic system are racing to control the governance layer, which includes spending controls, identity verification, and policy enforcement—these determine which agents have the authority to manage budgets.

Today, we will analyze who is building the banking layer for robots and what benefits those who dominate this layer can gain.

Why Own a Multi-Layered Architecture?

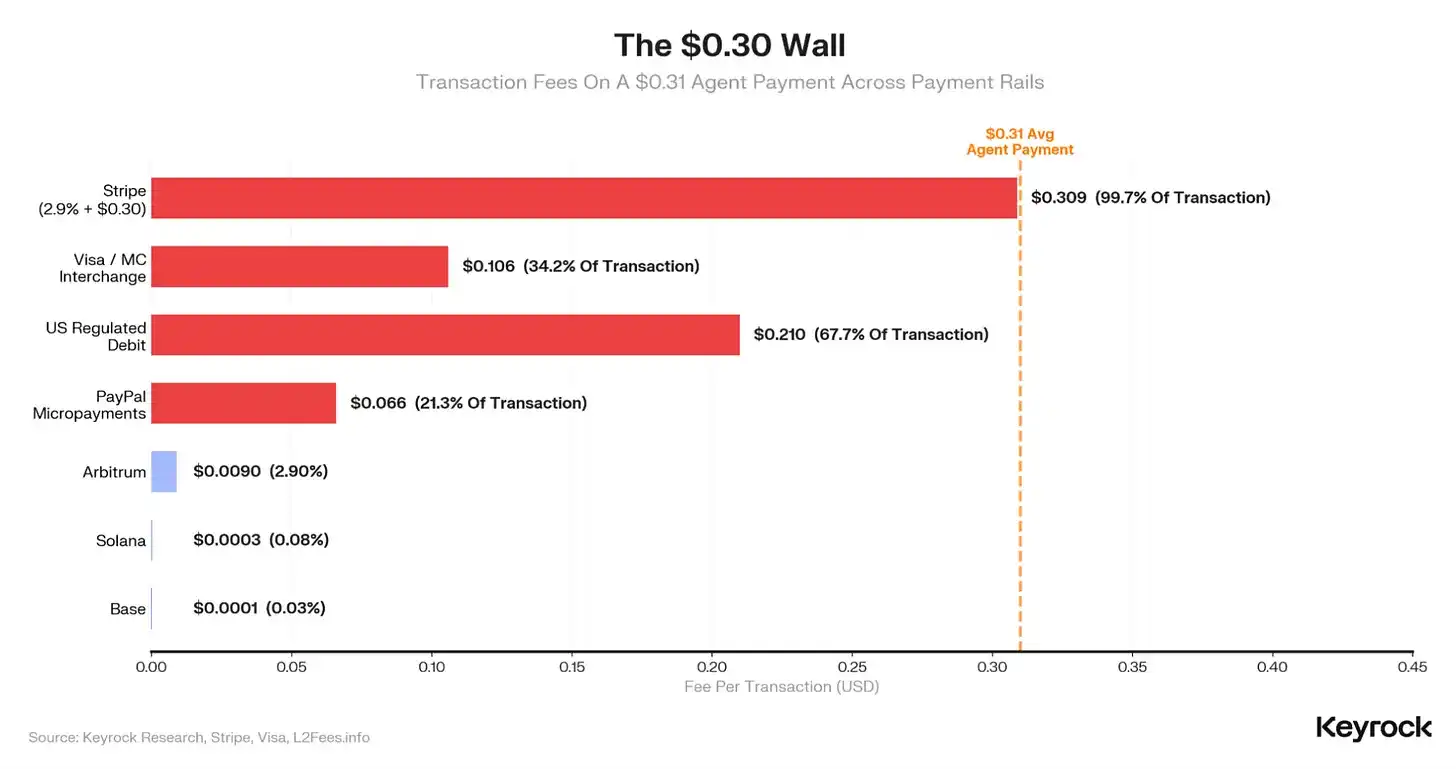

The economics of handling agent payments are very low. Over the past 12 months, the average AI agent payment was just 31 cents.

Consider how much profit is left for those processing transactions through multiple backend layers for a 31-cent payment. Stripe's standard pricing is 2.9% plus a 30-cent fixed fee, leaving the merchant with less than one-tenth of a cent. Visa's interchange fees would eat away another third. In contrast, a Layer-2 stablecoin payment system processing the same transaction charges only 0.0001 USD.

These economic factors provide a rationale for the use of cryptocurrency at the settlement layer.

The payment infrastructure at the settlement layer is largely in place. Coinbase's x402 protocol handled the vast majority of last year's 176 million transactions, and currently, about 3,900 merchants accept agent payments. Stripe and Tempo jointly developed a competing protocol—the Machine Pay Protocol (MPP), launched in March, which integrates over 100 services. Google, Visa, and Mastercard also launched agent payment products around the same time. This means five competing payment architectures emerged within just 12 months.

But the problem with agent payments is that no one gets rich processing 31-cent payments. Therefore, value concentrates in the funds in circulation and the enforcement of rules governing how agents make payments.

Last week, we explained how companies capture value by owning the wallet layer that holds AI agents' stablecoin balances. But floating balances are just one of many valuable layers worth capturing. Another value layer is the rules governing how these floating balances are used.

These rules include spending controls, agent identification, policy enforcement, audit trails, and allocating liability for failed transactions. This layer is wide open.

In April this year, American Express launched the "Agent Purchase Protection" plan, an insurance product designed to cover losses from erroneous purchases made by AI agents. This effectively acknowledges the current state of the AI agent governance layer. Solving the missing governance issue holds immense value in an industry projected to reach $3-5 trillion within five years.

This is why incumbent players are now racing to seize control of the governance layer.

But at which level should this layer be built? It could be a bank, a developer API, or even a wallet.

Wallet as the Governance Layer

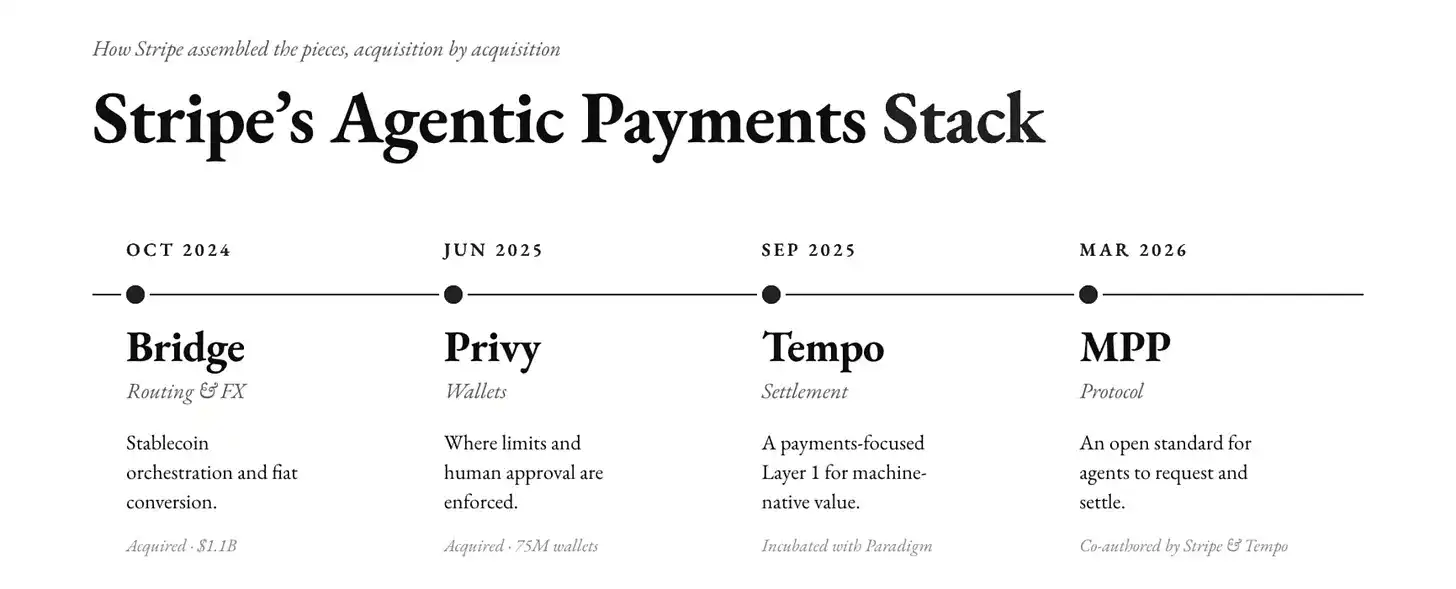

Every purchase an agent makes must go through a wallet. Therefore, the wallet is the optimal point to implement spending limits, identity verification, and human approval. Control the wallet, and you control the governance. Payment infrastructure company Stripe realized this early on.

In June 2025, Stripe acquired Privy, a company building embedded wallets for consumer crypto applications. Through this acquisition, Stripe gained 75 million wallets distributed across over 1,000 development teams. These wallets now sit at a critical choke point for fund flow, where all policies, spending limits, and human approvals must be executed before funds move.

Stripe has also built an entire agent payment technology stack. It acquired Bridge to handle stablecoin coordination and fiat conversion. Furthermore, it co-incubated Tempo with Paradigm, a Layer-1 blockchain focused on payments. Stripe and Tempo jointly authored the Machine Pay Protocol (MPP), an open standard for how agents request, authorize, and settle payments.

Stripe's Agent-Ready Financial Solutions now allow software to check balances, pay bills, store funds, create virtual cards, and transfer money. Agents can handle routine payments themselves, but any action outside their policy triggers a human review. Fund balances are powered by non-custodial Privy wallets available in over 150 markets.

Even Amazon, when forced to allow its developers to give AI agents spending power, chose two wallet companies—Privy and Coinbase. Not an experienced financial institution like a bank or card network, but a five-year-old wallet provider.

This is because wallets act as the ideal checkpoint, allowing an appropriate level of human intervention to ensure necessary checks and balances.

Keyrock, in its report "Who Pays for the Agent," states that the agent commerce market will "settle on an equilibrium where agents have considerable autonomy but operate within boundaries enforced by cryptography that humans can audit and revoke."

This is the position Privy holds within Stripe's stack. The wallet is responsible for setting the boundaries within which agents must operate.

Here's how governance policies work on this stack.

Privy offers two smart wallet models. In the first, the agent has full control of the wallet and executes transactions within policy constraints without human approval—ideal for fully autonomous agents like trading bots and portfolio managers. In the second, the user retains wallet ownership but grants the agent limited permissions to operate as a signer. The user can revoke access at any time.

Stripe's MPP follows similar governance logic.

The MPP introduces a feature called "Sessions" for high-frequency agent tasks. In Session mode, the agent pre-authorizes a spending budget and then makes continuous payments within that limit without needing a separate request for each on-chain transaction. The MPP has implemented sub-cent billing for LLM inference and per-query billing for data APIs.

This is a level of governance granularity that card networks cannot support.

Vertical Stack Expansion

Although Coinbase's x402 currently leads in AI agent payments, Privy's advantage is less about cryptocurrency itself and more about its distribution moat built through Stripe.

Coinbase has 3,900 merchants accepting agent payments. For every merchant accepting agent payments via Coinbase, Stripe has roughly 1,000. In February this year, Privy stated that if all Stripe merchants opted to accept machine payments, agent commerce could scale today via Privy wallets. Stripe merchants do not need to build custom crypto infrastructure.

Competition between Stripe and Coinbase is intensifying, and other traditional giants have joined the race for vertical expansion, aiming to grow across the entire technology stack.

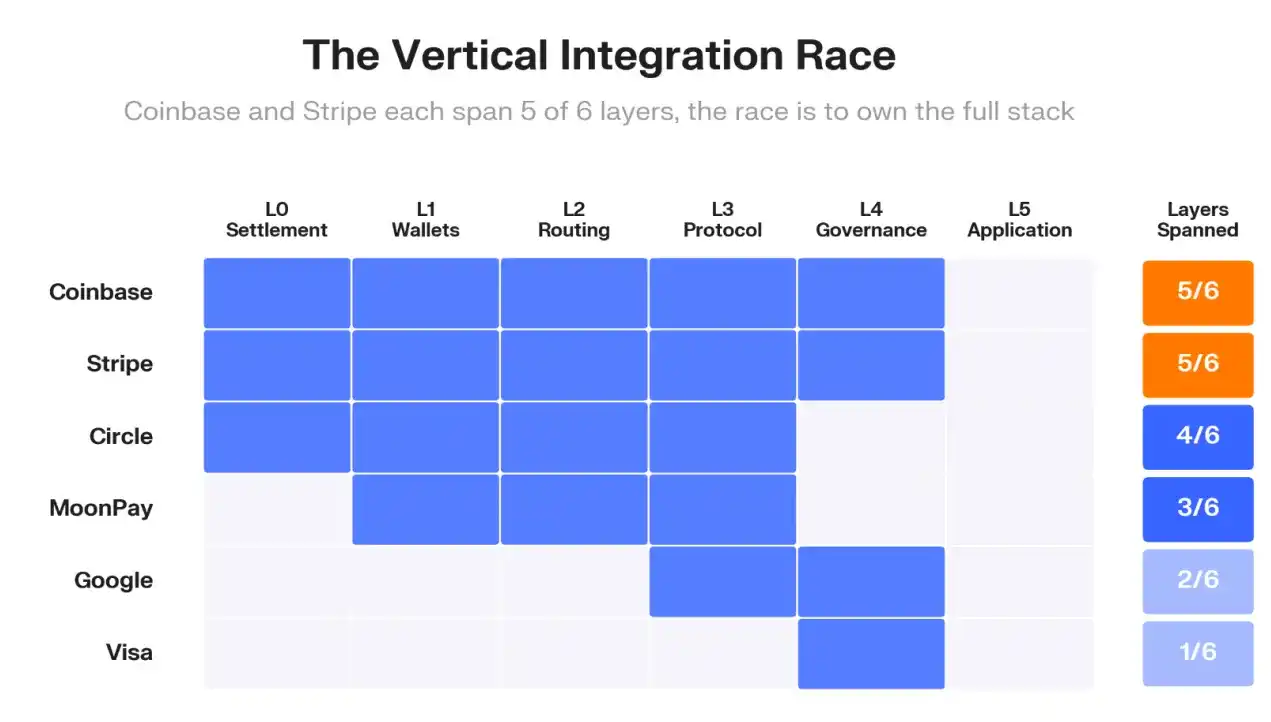

Keyrock mapped 179 projects across the six layers of the agent payment stack (Settlement, Wallet, Routing, Protocol, Governance, and Application).

Coinbase and Stripe each cover five of these six layers. Circle covers four. Despite their size, Google covers only two layers, and Visa just one.

Over the past twelve months, incumbent payment giants spent over $80 billion filling gaps in their own stacks. Capital One acquired AI-native software platform Brex for $5.15 billion. Mastercard acquired BVNK for $1.8 billion. Among these, the wallet layer and the AI software layer saw the most active M&A activity. Stripe acquired Privy, Fireblocks acquired Dynamic, Arbitrum acquired ZeroDev. In each case, a payment infrastructure provider acquired an independent wallet provider.

Collectively, these deals indicate the market has identified a scarce resource layer. Settlement fees become cheap and interchangeable, but programming permissions, budgets, and liability are where the value lies.

Vertical integration across multiple layers also has compounding effects.

Whoever owns this checkpoint sets the spending rules, intercepts funds before they move, decides which merchants, agents, and apps get trusted access, and charges fees to do all this. We see this in the Privy-Stripe distribution moat.

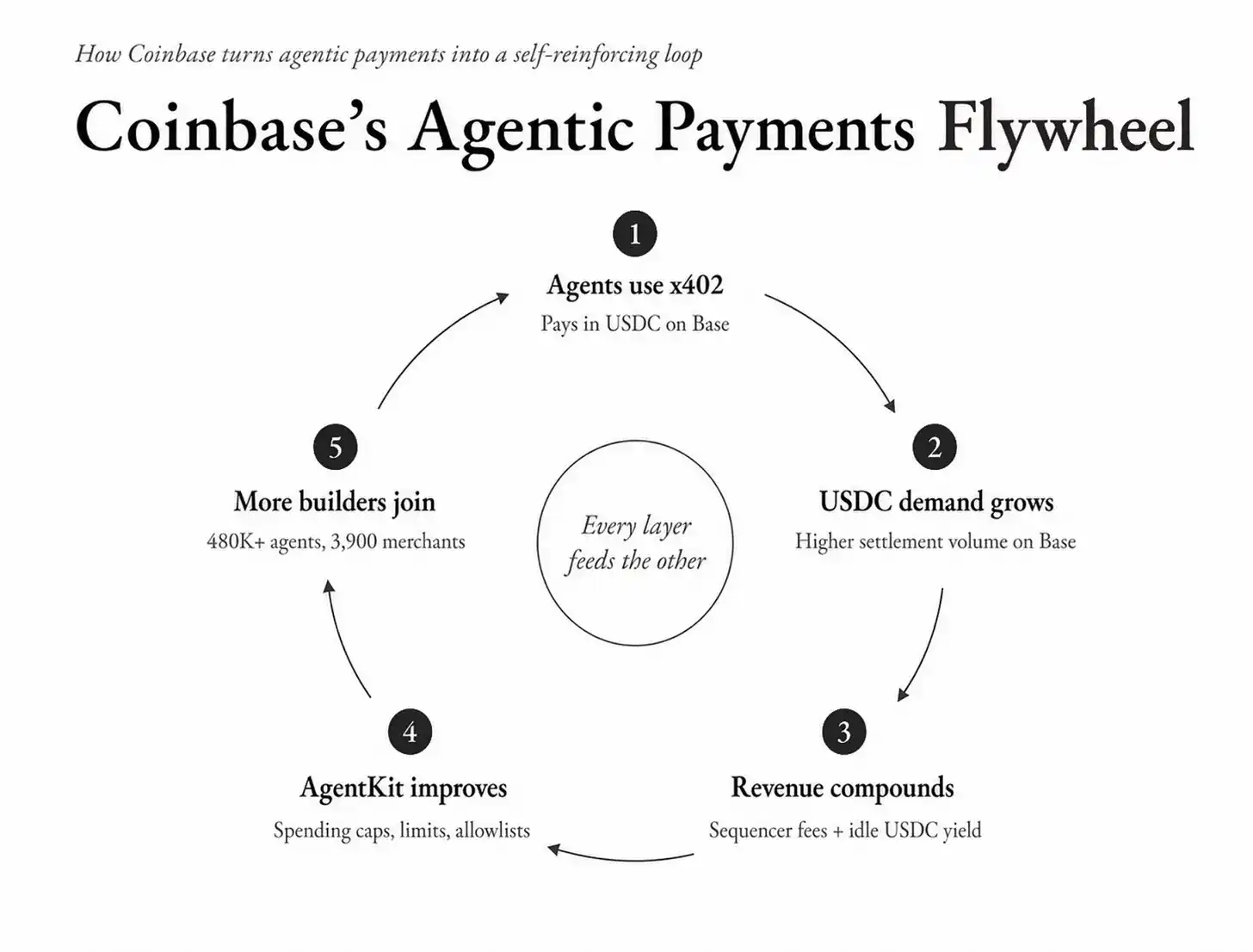

Even Coinbase's stance reflects this dynamic. Every x402 payment generates USDC demand on its Layer-2, Base, producing float yield. This yield funds more agent tools via AgentKit, which features built-in session caps, single-transaction limits, and allowlists restricting transfers to audited contracts. More agents on AgentKit mean more x402 payments. Each layer influences the others.

Incumbent investment activity is significantly more active.

Coinbase Ventures also invested in Catena Labs, Skyfire, and Payman, three of the most prominent independent governance startups currently. Circle's co-founder Sean Neville founded Catena, and Circle invested in Skyfire. a16z led funding rounds for both. Visa backed Payman and partnered with Skyfire.

The same players building payment settlement infrastructure are funding the governance layer. The idea is that incumbents maximize their returns if governance functions remain part of the existing infrastructure, as Privy built in its two models. If governance becomes a separate layer, they profit via their portfolio.

What Does Controlling the Governance Layer Mean?

Payment processing was never the most valuable position because financial systems eventually commoditize. Once that happens, profit margins shift to where the decision is made about whether a transaction is allowed and under what conditions.

Historically, many industries have undergone the same commodification process.

Consider what happened after the internet commodified cable TV. All Internet Service Providers (ISPs) became nearly identical, almost interchangeable. Therefore, telecom companies had to expand vertically to stay competitive.

India's two largest telecom operators, Jio and Airtel, began bundling hundreds of TV channels, six OTT platform subscriptions, unlimited voice calls, set-top boxes, and free routers into a single broadband package. Similarly, AT&T spent $85 billion to acquire Time Warner, becoming a media-telecom giant. The aim was to combine Time Warner's premium content—like HBO, Warner Bros., and CNN—with AT&T's vast distribution network to compete with streaming platforms like Netflix and Amazon.

When broadband connectivity (the underlying infrastructure) became the cheapest part of the package, value shifted to the combination of content, relationships, and offers that best attracted customers.

We see this happening in crypto as well.

Settlement was supposed to happen at the protocol layer. Think of Ethereum as a shared ledger where everyone settles. After Coinbase launched Base as a faster, less congested Layer-2 chain, it began collecting gas fees from every transaction settled on its own chain. Today, Coinbase earns approximately $60 million annually in sequencer revenue by processing transactions on Base.

Players building agent payment systems have learned this lesson.

In "Active Buoyancy," we explained how an economy can be built by controlling the stablecoin balances agents hold between transactions. This allows companies that control the wallet layer of the stack to add a revenue stream.

The governance layer adds another revenue stream, and potentially a much larger one.

Visa processes $14.2 trillion in payment volume annually, earning a roughly 0.28% take rate. This rate includes not just fees but also the implicit management fee Visa earns for the trust built by preventing fraud, resolving disputes, and enforcing network rules.

Applying even a fraction of this rate to agent transactions gives us an idea of the immense value it brings to companies built on the governance layer. McKinsey's $3 trillion projection for agent transactions by 2030 means that even a governance fee of just 0.1% (about 35% of Visa's take) could generate $3 billion in annual revenue. For reference, Coinbase's total subscription and services revenue in 2025 was approximately $2.8 billion. Revenue from just the agent transaction governance layer alone could match what Coinbase currently earns from staking, custody, and Coinbase One combined.

Companies with a presence in the wallet, settlement, and governance layers of the agent finance stack can profit from idle agent balances (float revenue), settlement fees (sequencer revenue per transaction), and compliance fees (enforcing governance).

This is why vertical integration across the entire technology stack will be the only business model that allows companies to remain competitive in the agent era.