Author: Eric, Foresight News

How long has it been since you last heard news about Metaplanet?

In the first quarter of 2026, this company, Japan's and even Asia's largest Bitcoin treasury firm, adjusted its capital strategy. It chose not to dilute equity when its mNAV was less than 1 (meaning the company's market cap to crypto holdings value ratio was below 1), shifting towards strategies including Bitcoin-collateralized financing and share buybacks to maintain its stock price to some extent.

Although the Q1 financial report showed Metaplanet still purchased 5,075 Bitcoins, since the beginning of the second quarter, aside from announcing the acquisition of the Japanese licensed securities firm Siiibo Securities about a week ago to promote Bitcoin-backed bond-like products and explore security tokenization, there has been little other news.

Even Strategy, which guaranteed countless times it would never sell Bitcoin, has experimented with the market impact of selling a small amount of Bitcoin to replenish cash. The once "never sell" vow has become "ensure total holdings increase." When the DAT companies holding the top two positions in Bitcoin reserves are stretched thin, it's not hard to imagine the predicament other companies are currently facing.

In fact, aside from a few companies like Strategy, Metaplanet, and BitMine who are still holding on, most former DAT companies have begun seeking other avenues.

Two Paths to Survival

In the face of an unexpected bear market, many DAT companies have directly chosen to "quit the game."

ETHZilla is a typical example. Backed by Peter Thiel, this company held over 90,000 ETH at its peak in 2025 but sold a total of $115 million worth of ETH twice by the end of that year to repay debt. This year, it has abandoned the DAT model altogether, pivoting to businesses like RWA tokenization.

Bitcoin DAT companies like Prenetics Global and Sequans Communications have also chosen to quit, returning to their core businesses. Many bandwagon altcoin DAT companies are in the same boat, with their stock prices nearing zero and the coins in their hands difficult to liquidate, so they simply give up. Data shows that in July 2025 alone, DAT companies bought approximately $20 billion worth of cryptocurrency, while the total purchase volume in Q1 this year was only about $3.7 billion.

Facing the stalling of their flywheel, aside from quitting or giving up, mid-tier treasury companies have begun a collective strategic pivot, which can roughly be summarized into three directions. They all point to one core proposition: DAT must evolve from a passive balance sheet manager to an active ecosystem participant to truly possess commercial value.

The first direction is repositioning themselves as institutional-grade crypto asset management platforms and yield funds. SharpLink Gaming is a representative of this path. From day one, this company has staked nearly 100% of its ETH holdings and allocated all staking rewards to shareholders without taking any fees. This stands in stark contrast to spot ETH ETFs, which, although granted staking permission by the SEC, can only stake about 50% of their holdings to meet daily liquidity requirements. Building on this, SharpLink partnered with the Wall Street veteran crypto investment bank Galaxy Digital in early 2026 to launch the $125 million "Galaxy Sharplink On-Chain Yield Fund," investing approximately $100 million worth of staked ETH into DeFi liquidity protocols seeking excess returns. This company is transforming from a simple cryptocurrency holding company into a management platform providing institutional clients with access to on-chain yield configurations.

The exploration by GameSquare, which holds about 15,000 ETH, is more radical. This listed company, which owns gaming assets like FaZe Clan, collaborated with crypto asset management firm Dialectic to integrate Dialectic's self-developed Medici platform. This platform uses machine learning models and automated algorithms to dynamically allocate funds across 72 to 250 different DeFi protocols, targeting annualized returns of 8% to 14%, far exceeding the 3% to 4% benchmark of standard Ethereum staking.

The second direction is transforming into blockchain infrastructure operators, which is particularly evident in the Solana ecosystem. DeFi Development is one that has gone the furthest. This company not only purchases large amounts of SOL but also acquired a validator company and launched its own liquid staking token, dfdvSOL. dfdvSOL has been integrated into multiple core Solana DeFi protocols like Kamino, Orca, Drift, and Jupiter Lend, used as lending collateral and liquidity pool assets. DeFi Development earns fee income from every staking operation and protocol integration, building a self-reinforcing network effect loop.

SOL Strategies acquired three validator companies, constructing a complete business line from digital asset holding to infrastructure operation. It manages over 3.4 million SOL in delegated staking, far exceeding its own treasury size, shifting from serving its own balance sheet to providing staking infrastructure for institutional clients across the entire ecosystem.

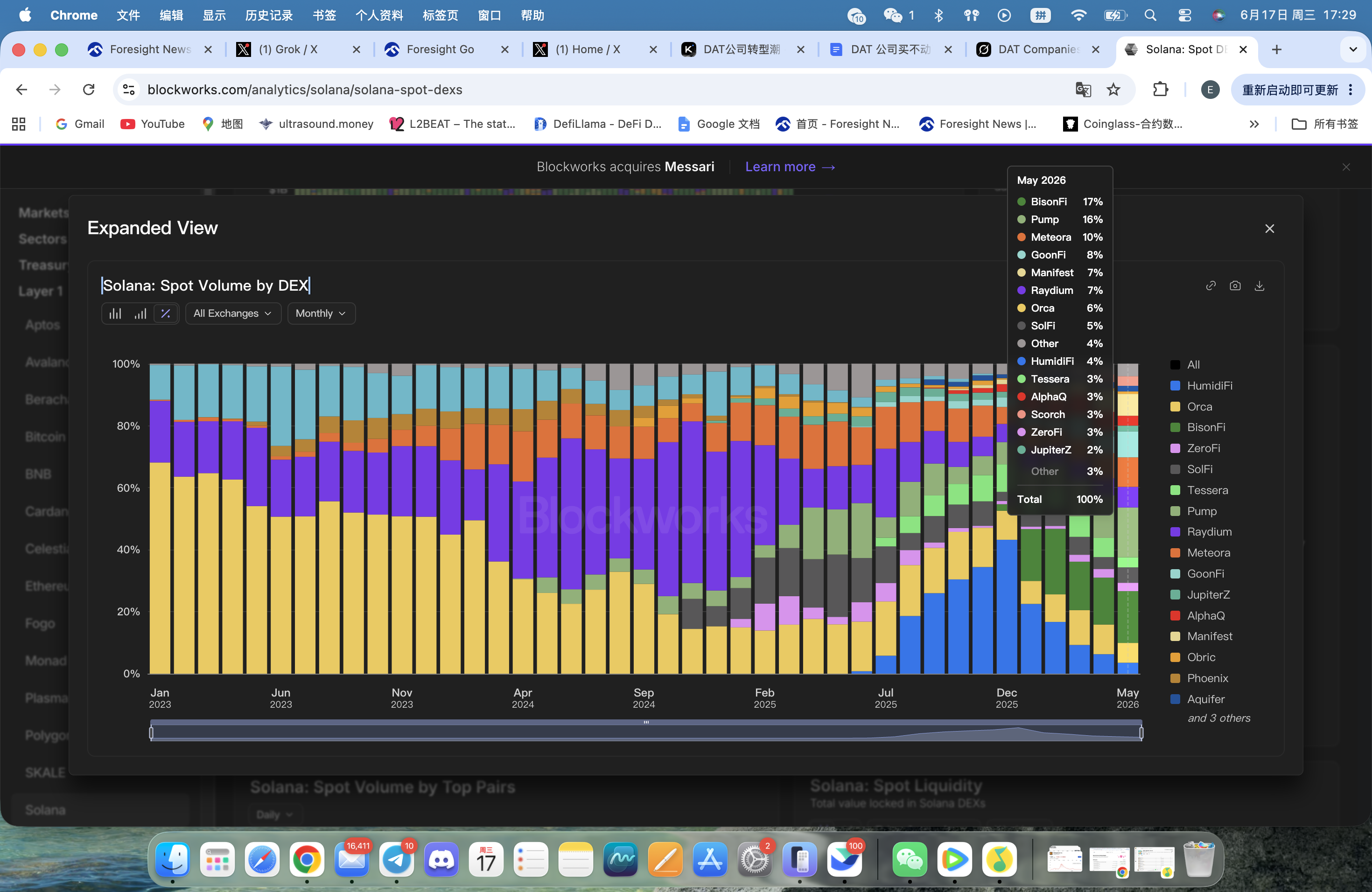

Forward Industries has followed a similar path. Besides launching its liquid staking token fwdSOL, Forward Industries also collaborated with Galaxy Digital and Jump Crypto to launch the propAMM project BisonFi. Since its launch, BisonFi has surged ahead to become the highest volume DEX on Solana, squeezing the once-dominant HumidiFi to less than a 4% market share.

These two routes essentially correspond to the capital market's different attitudes towards Ethereum and Solana. ETH's recognition as an "asset" itself is still higher than SOL's. ETH treasury companies can position themselves as "funds managing ETH," providing institutions with exposure to yield-generating assets. On the other side, Solana's crypto-native attributes are more pronounced. SOL treasury companies need to demonstrate their profitability within this ecosystem, showcasing their value in a logic closer to the "look at the financials" approach of regular listed companies.

Can the Transformation Succeed?

The collective transformation of DAT companies actually reflects a profound cognitive upgrade the entire crypto industry is undergoing. The treasury model initially pioneered by Strategy was essentially a form of financial engineering that leveraged the convenience of public market financing and investor sentiment for capital arbitrage. When participants expanded from a few early adopters to hundreds of companies, and from Bitcoin to various altcoins, scarcity was diluted, and premiums naturally evaporated. The launch of cryptocurrency ETFs further accelerated this process. When investors can purchase ETH ETFs with staking yields directly through traditional brokerage accounts at prices close to net asset value, the logic of holding DAT stocks at a premium is fundamentally shaken.

The answer given by successful transformation cases is operational capability. Whether it's SharpLink's 100% staking strategy and institutional-grade yield fund, DeFi Development's dfdvSOL ecosystem and validator network, or GameSquare's machine-learning-driven yield platform, they are all attempting to build difficult-to-replicate operational barriers around crypto assets. These barriers may stem from technological advantages, network effects, institutional partnerships, or deep participation in the on-chain financial ecosystem.

However, these transformations are not without risks. The 8% to 14% DeFi yield pursued by GameSquare is built on smart contract risks and protocol risks; any major DeFi protocol vulnerability or extreme market event could lead to significant losses. DeFi Development's business model is highly dependent on the healthy development of the Solana network; once the ecosystem cools, its entire business would be impacted.

For the Web3 market, the impact of this transformation is profound and complex. Those DAT companies that have successfully evolved into infrastructure operators and asset management platforms are building bridges between traditional finance and the blockchain ecosystem, promoting the maturation and standardization of institutional-grade services. But the process of the DAT model moving from frenzy to sobriety also sends an important signal to the market: in the crypto space, pure capital games are not for everyone. Entities that truly participate in network building, create actual cash flow, and provide user value possess greater anti-cyclical capabilities.

The DAT movement is entering a stage of sober restructuring from a capital carnival. This might not be bad news. An industry can only truly see who is swimming naked and who is building an ark after the泡沫 recedes. The collective pivot of treasury companies is both a passive response to survival pressure and the inevitable growing pains of a nascent industry maturing.