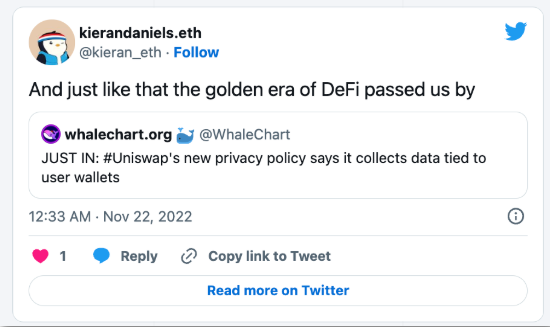

随着MetaMask和Uniswap披露了他们追踪用户的程度,Discord中的许多人对此表示反对。

""

你怎么看你的个人数据的披露程度?

""

至少据我了解,有很多DeFi用户们现在对流行的Uniswap追踪公共用户数据的披露大为不满。

""

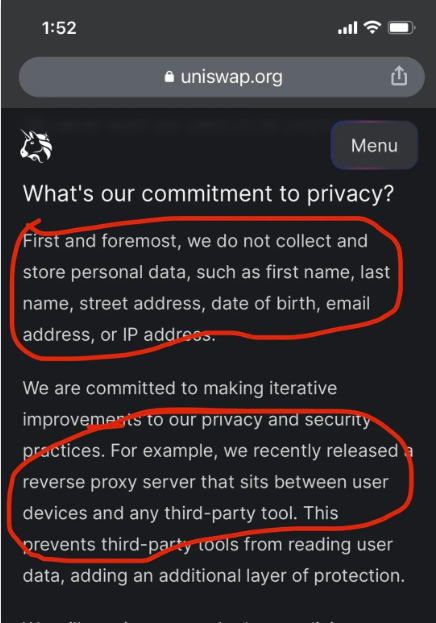

诚然,该交易所没有跟踪个人姓名或IP地址这类私人数据,但根据新上传的条款和条件文件,几乎所有可在网上公开查看的东西都被汇总和收集了。

""

无独有偶的是,本周早些时候,流行的以太坊钱包Metamask承认了跟踪用户的IP地址。

""

这难道是他们考虑到什么政策不得不做出的妥协吗?

Uniswap在追踪什么?数据给了谁?

""

根据其隐私政策,Uniswap收集的许多乱七八糟的信息活中包括公共区块链数据、用户偏好、移动和浏览器元数据、客户调查中包含的生物数据(其中包括姓名)和客户服务通信数据,以及第三方服务供应商提供的有关“非法或其他欺诈活动”的信息。

""

人家Uniswap自己非常“有理有据”,宣称收集这些用户数据是为了“改善DEX的用户体验”。

""

那么它向谁提供这些数据呢?

""

只有服务提供商、执法部门、法院(在遵守搜查令的情况下)、经纪公司和并购律师,仅举几个实体。基本上,任何可能以任何方式与Uniswap Labs(交易所背后的法律实体)有关联的人和所有人。

""

但最重要的是,它这么做不是刚刚开始跟用户打声招呼,而是已经这么做了很多年,只是现在才告诉用户。

""

“去中心化是一个神话吗?“一位DeFi Degen在Crypto Twitter上控诉。

此刻,在推特上搜索中输入“Uniswap用户数据特务(TREASON)”,就可以看到很多人的吐槽和质疑。

""

在某种程度上,这种疑虑并不是完全没有道理的。一位名叫Yoda Research的DeFi分析师认为,这反映了“加密货币的持续集中化趋势”。Yoda指出,隐私政策不是由Uniswap DAO决定的,而是由大概是其核心团队的开发人员单方面管理的。

""

对DeFi的许多人来说,Uniswap的T&Cs是一个不受欢迎的数据采集、Web2感觉的引入DeFi。

""

正如激进的去中心化爱好者Chris Blec所指出的,Uniswap团队曾经是一个由强硬的、反体制的编码员组成的中立队伍,但现在已经被旧世界的守旧派所占领。

有关的用户数据是通过Uniswap网站追踪的,该网站的后端不对公众开放,由一小群为Uniswap Labs工作的开发者管理,该公司开发了交易所,即存在于区块链上的底层协议。

""

这个小组获得了Uniswap最初代币铸币收益的40%,在四年的归属期后,将对交易所的管理机制有更大的影响力。

""

交给这几个人掌控,这不又是背离了去中心化的精神本质吗。

在这个队伍中,有来自纽约证券交易所、贝莱德和数据跟踪公司Chainalysis的高管,以及前奥巴马发言人和美联储经济学家。

""

这个团队班子一看就是不是很符合我们心中那些加密行业交易中心的人,这帮人就不是加密行业的坚定信仰者,或许可以说,这就是为什么这些平台从未真正起飞的原因。

""

我想起了以前的一条有趣的推特。它具有讽刺意味,但还是抓住了当时的主流精神。

""

“没有人'经营'加密货币公司......我们只是普通人的代理人,通过他们的小作品,分解账本货币的梦想在这个最不值得的主物质平面上体现出来。”

""

也许,做出这样的数据追踪是平台有一些法律上难言之隐类的合理考虑。总归说起来,加密行业仍就属于尚未被主流采用,渴望被认可的漫长努力阶段,相关法律法规定性分析未明确之前,加密货币开发者很容易被扣上个帽子拘留,就像发生在荷兰的隐私平台Tornado Cash的开发者身上一样。就在本周,荷兰当局裁定,在审判开始之前,有关开发人员应在监狱中再呆三个月,并给他贴上逃跑风险的标签。

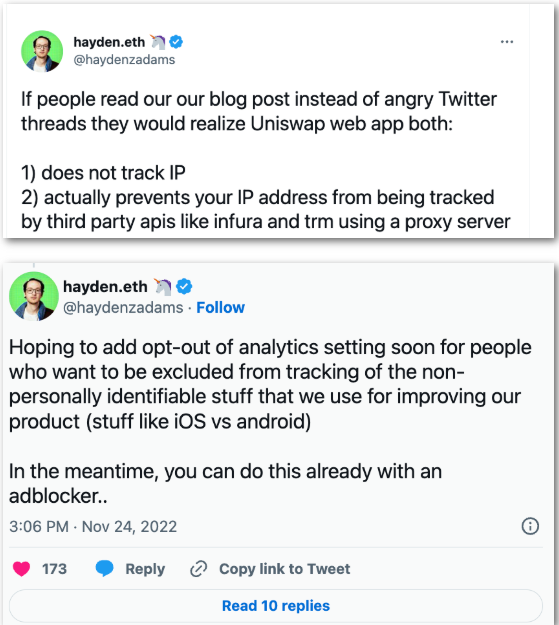

Uniswap实验室没有确认或否认最近在Defi世界的逮捕是否刺激了其公开数据政策的决定。然而,拥有类似数据政策的Metamask公司的开发人员Dan Finlay对外表示,这是由欧盟的一般数据保护条例和雇用新的数据保护官员所推动的,但这个决定“不是由任何数据分析的增加所驱动的”。

""

他承认,该政策暴露了现代以太坊规范的缺陷,但他说,对于大型的、广泛使用的以太坊产品来说,这是一个必要的,即使是不太理想的义务。

""

看来,这个冬天对于Defi用户们来说还很漫长,谨慎的从业者们不应该错过行业里风吹操作的任何消息。