1. BTC second horizontal adjustment

BTC's sideways adjustment shows that the early warning of decline has not been lifted and BTC is still looking for a downward breakthrough trend after the price has accelerated to fall. At present, BTC is in the second stage of horizontal operation. Before that, the price showed an accelerated retreat trend on August 19 and August 26. At present, the trading enthusiasm of investors has increased slightly, and there are signs of continuous and frequent pulse amplification in trading volume. Once the price platform of US $20000 falls, it may be difficult to predict the low point.

2. Profit clearing of long-term investors

From the trading profit performance of long-term investors, SOPR index reached the recent high of 1.532 and 1.395 on August 28 and August 29, respectively, indicating that there is a large trading profit space for long-term investors. In other words, the market is in a stage of long-term investors' profit flight, which makes the BTC price which has been in a falling state shaky. From the perspective of the trading profit space of long-term investors, the average profit after two consecutive trading days of profitable trading is close to 50%.

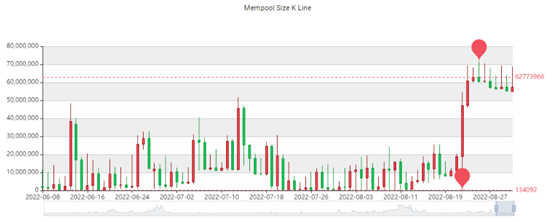

3. Increase in unconfirmed transactions

Since August 23, the unconfirmed transactions of BTC have reached a peak level, which is the highest value in nearly three months. With the further closing price drop of BTC on August 26, the number of unconfirmed transactions did not decrease significantly. From the perspective of transaction fees, most of the transaction costs are very low, which means that the transaction volume of small and medium-sized investors is large and contributes the largest number of unconfirmed transactions. In the process of reduction of unconfirmed transactions, it is expected that the BTC price may still easily fall below the current price platform, and the adjustment expectation is still at a high level.

4. Eth rebound space is limited

During the contraction of eth trading volume, there is not much room for the price to rebound in the falling stage, and it is still operating under the middle rail of the brin line. Therefore, it is expected that there is still an opportunity for the ETH price to fall further. At present, ETH has further confirmed the reversal trend of the head and shoulder top, and the neck line of this form is around us $1500. It is expected that after further falling below US $1500, the pace of decline will probably accelerate.

5. Eth financing interest rate rebounded

The financing interest rate of eth has remained above 0 for a long time, reaching 0.012 to 0.024 in the last four months. Starting from August 22, the financing interest rate began to decline significantly, reaching a minimum of 0.026.

With the increase of the purchase scale of eth, the financing interest rate continued to rise. At present, the financing interest rate is close to 0, so it is judged that eth may have ended its adjustment performance.

Next, the possibility of eth further falling is increased. The financing interest rate rebounded to around 0, which means that the selling pressure may form again. The financing interest rate rebounded in the price horizontal operation stage, which means that it is more difficult for the ETH price to rebound after the cost of long buying increases. In terms of short-term support, we can pay attention to the USD 1347 corresponding to the decline of eth's brin line.