Ripple’s former CTO David Schwartz pushed back against the idea that he is a committed long-term XRP holder, saying in a series of X posts that Ripple stock, not XRP, now represents his main exposure to the crypto sector.

The comments matter because Schwartz remains one of the most closely watched figures in the XRP community. His remarks cut directly into a recurring tension around Ripple, XRP and the difference between exposure to the company’s business and exposure to the asset associated with the XRP Ledger.

The exchange began after users revisited Schwartz’s past decision to sell ETH at $1.05. Responding to a post that framed the sale as a missed opportunity, Schwartz said he did not view the upside probability as obvious at the time.

“If I had thought there was a 1% chance of it hitting $2,368, I would not have sold it for $1.05,” he wrote. “I’m still not sure the odds of that happening really were more than 1% at the time.”

That admission set off a broader discussion about Schwartz’s current XRP exposure. When asked whether he was still holding XRP, he replied that he no longer had “that much left anymore” and had tried to move most of his assets away from crypto risk, with one major exception: Ripple stock.

“I fully recognize that crypto may be a once-in-a-generation chance to get rich that we have not missed yet and that may mean that I miss a lot of it,” Schwartz wrote. “I’m okay with that and hope my Ripple stock gives me enough exposure. I sleep better at night that way.”

Ripple Stock As The Core Exposure

Schwartz framed the decision as a question of risk tolerance rather than a direct call on XRP’s future price. He said he does “not really like risk,” even though many of the risks he has taken have worked out well for him. In another post, he made the point more bluntly.

“I’m not the diamond hands guy. That’s not me. I’m the smart, sensible investment guy who might miss the big opportunities. And I’m okay with that.”

For XRP holders, the more consequential part of the exchange was not simply that Schwartz said he holds less XRP. It was his explanation that Ripple stock already gives him enough exposure to the same broad ecosystem. When asked whether he would view XRP differently if he had less stock, Schwartz said he probably would.

“Yeah. I think I would hold more XRP (and probably more of other cryptos as well) if I had less exposure to the crypto space through my Ripple stock. I kind of feel like that’s enough risk just there and almost everything else should be fairly conservative.”

That distinction is important. Schwartz did not say XRP and Ripple stock are the same trade. In fact, he argued the opposite when asked about whether Ripple could ever create an “XRP for equity” scheme that would give long-term XRP holders priority access to shares if Ripple were to go public.

He said information he has on secondary-market trading of Ripple shares is covered by non-disclosure agreements, though he pointed users toward platforms such as Notice.co and Hiive for public-facing data. But he was skeptical of tying XRP holders more directly to Ripple’s equity story.

“I’m personally not a fan of Ripple trying to do something like that,” Schwartz wrote. “If people want exposure to Ripple’s gains and losses, they should buy Ripple stock on the secondary market. I don’t think it’s good for XRP for its value to become more entangled with Ripple’s success or failure than it absolutely needs to be.”

The Legal Line Between XRP And Equity

Schwartz also rejected the idea that the firm could simply open stock access to XRP holders. When one user argued that the company should let the community buy Ripple stock directly, he said there was “no practical way” to do that under current law.

“Ripple stock is, without doubt, a security,” he wrote. “If you want direct exposure to Ripple’s success or failure, you can buy Ripple stock on the secondary market if you qualify under US law. But you probably shouldn’t.”

He also described any future Ripple public listing as speculative, citing uncertainty around the regulatory environment. A less favorable SEC in the future, he argued, could become a major issue if Ripple were to go public in the United States.

The discussion later turned to Schwartz’s own XRP allocation. Asked why he had only 26 million XRP while other early Ripple-linked figures received far larger amounts, he declined to revisit the full history but said he ended up with “quite a bit of Ripple stock.” In another reply, he clarified that the 26 million XRP was not a gift, saying it was XRP he had traded bitcoin for.

“Once XRP hit 10 cents, I had millions of dollars at risk,” he wrote. “I very much did not like that at the time.”

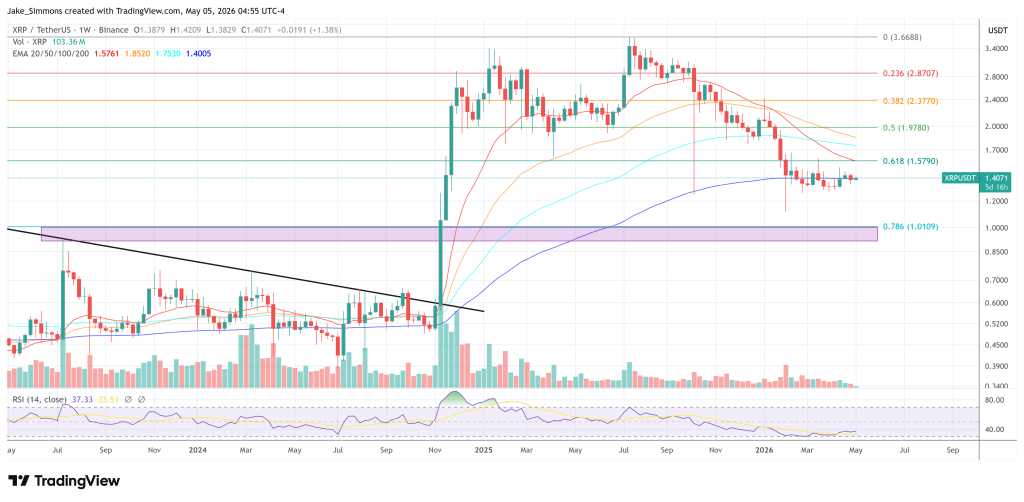

At press time, XRP traded at $1.4071.