The crypto market in December is as cold as the weather.

On-chain transactions have been dormant for a long time, and new narratives are hard to come by. Just look at the drama and gossip in the Chinese CT (Crypto Twitter) space these past few days, and you'll know hardly anyone is playing in this market anymore.

But the English-speaking community has been discussing something new.

A meme coin called Snowball launched on pump.fun on December 18th. In four days, its market cap surged to $10 million and is still hitting new highs; yet it's barely mentioned in Chinese circles.

In the current environment, devoid of new narratives and where even memes are considered unplayable, this is one of the few things that catches the eye and shows some localized wealth effect.

And the name Snowball itself tells the story it wants to convey:

A mechanism that allows the token to "roll and grow larger by itself."

Turning Transaction Fees into Buy Pressure, Rolling the Snowball for Market Making

To understand what Snowball is doing, you first need to know how tokens on pump.fun typically make money.

On pump.fun, anyone can create a token in minutes. The token creator can set a "creator fee," essentially taking a cut of every transaction into their own wallet, usually between 0.5% and 1%.

This money could theoretically be used for community building or marketing, but in practice, most Devs choose to: accumulate enough and then run.

This is part of the typical life cycle of a shitcoin. Launch, pump, harvest fees, rug. Investors aren't betting on the token itself, but on the developer's conscience.

Snowball's approach is to not take this creator fee money.

To be precise, 100% of the creator fees do not go into anyone's wallet but are automatically transferred to an on-chain market-making bot.

This bot performs three actions at regular intervals:

First, it uses the accumulated funds to buy tokens on the market, creating buy-side support;

Second, it adds the bought tokens and the corresponding SOL to the liquidity pool, improving trading depth;

Third, it burns 0.1% of the tokens with each operation, creating deflation.

Additionally, the percentage taken as the creator fee is not fixed; it fluctuates between 0.05% and 0.95% based on market cap.

It takes a higher percentage when the market cap is low, allowing the bot to accumulate ammunition faster; it reduces the fee when the market cap is high, decreasing transaction friction.

In one sentence, the logic of this mechanism is: every time you trade, a portion of the money automatically becomes buy pressure and liquidity, instead of going into the developer's pocket.

Therefore, it's easy to understand this snowball effect:

Transactions generate fees → Fees become buy pressure → Buy pressure pushes the price up → Higher price attracts more transactions → More fees... theoretically, it can roll on its own.

On-Chain Data Situation

Now that we've covered the mechanism, let's look at the on-chain data.

Snowball launched on December 18th, so it's been four days now. Its market cap grew from zero to $10 million, with a 24-hour trading volume exceeding $11 million.

For a shitcoin on pump.fun, these results mean it's already one of the longer-lasting ones in the current environment.

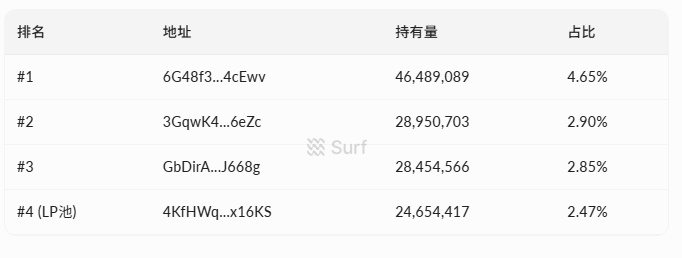

In terms of token distribution, there are currently 7,270 holder addresses. The top ten holders combined hold about 20% of the total supply, with the largest single holder holding 4.65%.

(Data source: surf.ai)

There's no address holding 20-30% of the supply; the distribution is relatively decentralized.

Regarding trading data, there have been over 58,000 cumulative transactions since launch, with 33,000 buys and 24,000 sells. The total buy volume is $4.4 million, and sell volume is $4.3 million, resulting in a net inflow of about $100,000. Buying and selling are basically balanced, with no one-sided selling pressure.

The liquidity pool holds about $380,000, half in tokens and half in SOL. For a market cap of this size, the depth isn't very thick, and large orders would still experience significant slippage.

Another notable point is that Bybit Alpha announced listing the token less than 96 hours after launch, which to some extent confirms the short-term hype.

Perpetual Motion Meets a Cold Market

Looking around, you can see the English community's discussion about Snowball mainly focuses on the mechanism itself. Supporters' logic is straightforward:

This is the first meme coin that locks 100% of the creator fees into the protocol; developers can't take the money and run, making it structurally safer than other shitcoins, at least.

The Dev is also playing into this narrative. The developer wallet, market-making bot wallet, and transaction logs are all public, emphasizing "verifiable on-chain."

@bschizojew labels himself as "on-chain schizophrenia, 4chan special forces, first-generation meme coin veteran," radiating a self-deprecating degen vibe that really appeals to the crypto-native community.

But a safe mechanism and making money are two different things.

The snowball effect relies on the premise that there is sufficient trading volume to continuously generate fees to feed the bot for buybacks. More trades mean more ammunition for the bot, stronger buy pressure, higher prices, attracting more people to trade...

This is the ideal state for any meme coin's so-called buyback flywheel to spin up in a bull market.

The problem is, the flywheel needs external momentum to start.

What is the current crypto market environment? On-chain activity is sluggish, overall meme coin hype is down, and there's simply less capital willing to chase shitcoins. In this context, if new buy pressure doesn't keep up and trading volume shrinks, the fees the bot receives will become less and less, buyback strength weakens, price support falters, and trading willingness declines further.

The flywheel can spin forward, but it can also spin in reverse.

A more realistic problem is that the mechanism solves only one risk point—"developers taking money and running"—but meme coins face far more risks than that.

Whales dumping, insufficient liquidity, narratives going out of style—if any of these happen, 100% fee buybacks can only do so much.

Everyone is tired of being rugged. As one Chinese crypto brother aptly summarized:

Play if you want, but don't get in over your head.

More Than One Snowball Rolling

Snowball isn't the only project telling this automated market-making story.

Within the pump.fun ecosystem, a token called FIREBALL is doing something similar: automatic buybacks and burns, packaged as a protocol other tokens can plug into. But its market cap is much smaller than Snowball's.

This shows the market is currently responsive to the direction of "mechanism-based meme coins."

The traditional玩法 (playbook) of shilling, pumping, and community hype is finding it harder to attract capital. Using mechanism design to tell a "structurally safe" story might be one of meme coins' latest tricks.

That said, artificially creating a specific mechanism isn't a new玩法 (play) either.

OlympusDAO's (3,3) in 2021 was the most classic case, packaging a staking mechanism with game theory, telling the story "if everyone holds, we all profit together." It reached a peak market cap of several billion dollars. The ending, as everyone knows, was a death spiral, dropping over 90%.

Even earlier, there was Safemoon's玩法 of "taxing every transaction and distributing it to holders," also a narrative of mechanism innovation, which ended with the SEC suing and the founders charged with fraud.

A mechanism can be a great narrative hook, capable of gathering capital and attention in the short term, but the mechanism itself does not create value.

When external capital stops flowing in, even the most精巧 (ingenious) flywheel will stop.

Finally, let's recap what this little gem is actually doing:

Turning the meme coin's creator fees into an "automated market-making bot." The mechanism itself isn't complicated, and the problem it solves is very clear: preventing developers from directly taking the money and running.

Developers not being able to rug doesn't mean you'll make money.

If after reading this you find the mechanism interesting and want to participate, remember one thing: it is first and foremost a meme coin, and only secondly an experiment with a new mechanism.