加密行业的清算日终于到来了。

在过去的五年里,代币享受了一种我愿意礼貌称之为「远超基本面的投机需求」的状态。不那么礼貌地说,它们一直被严重高估。

原因其实很简单:加密行业中具备良好基本面的流动资产并不多。因此,投资者只能通过他们能接触到的资产来获得敞口,这些资产通常是 比特币 或 山寨币。再加上那些听闻「比特币百万富翁」故事的散户投资者,他们希望通过投资更新、更小的代币来复制这种回报。

这导致了对山寨币的需求远远超过了那些真正有扎实基本面的山寨币供应量。

第一层效应

当市场情绪跌至低谷时,你可以随意买入任何资产,几年后就能获得惊人的回报。

第二层效应

大多数行业的商业模式(如果你能称之为商业模式的话),都围绕着出售自己的代币,而不是依赖于与其产品挂钩的实际收入来源。

过去两年里,山寨币市场经历了三件具有灾难性影响的事件:

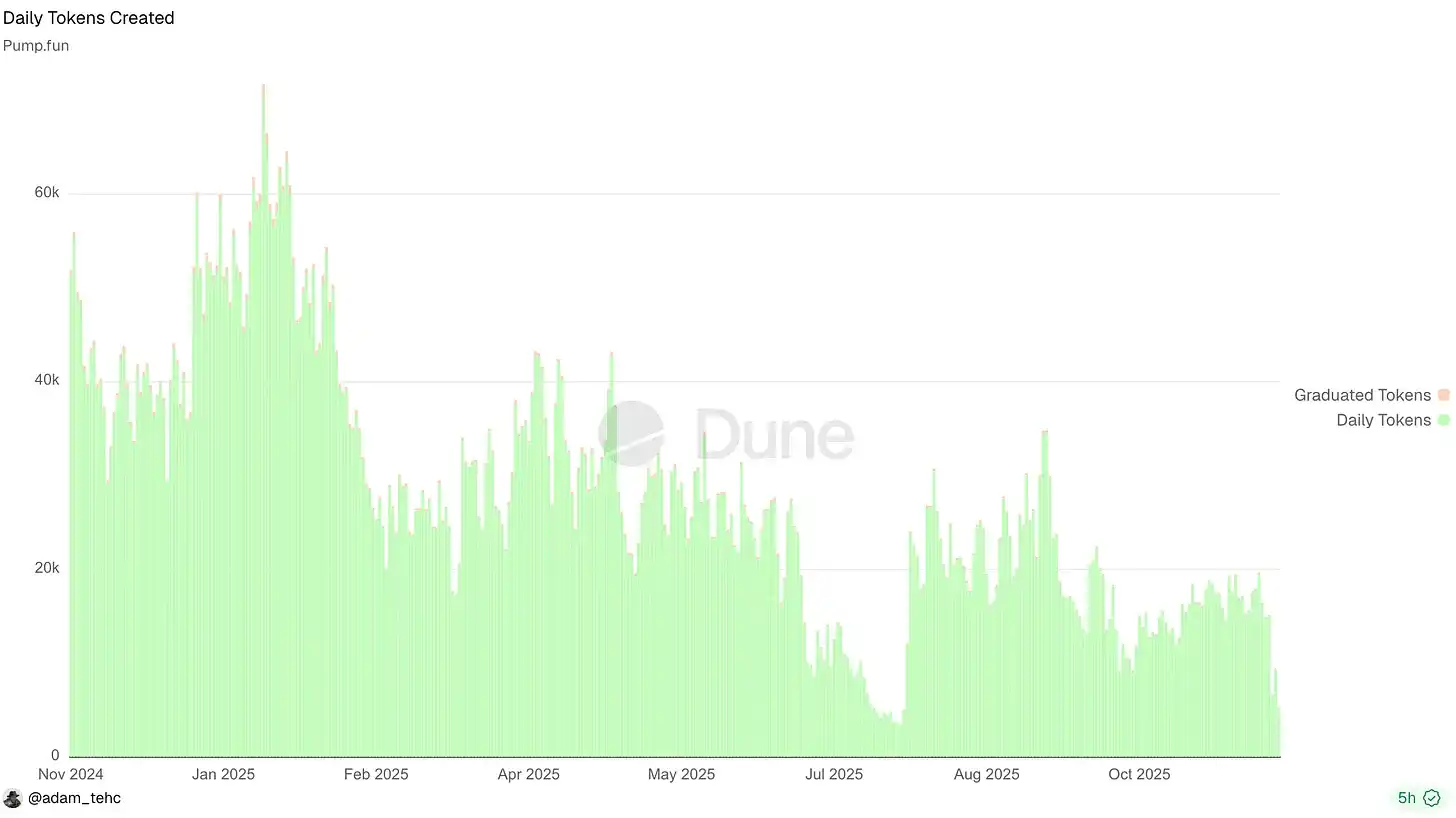

1.「Pump fun」和其他代币发行平台的兴起

这些平台将新代币的发行「商品化」(即变得过于普遍化),导致注意力被分散到数百万种资产上。这种分散效应阻止了前几千种顶级代币继续吸引集中资金流入,也扰乱了比特币减半通常会带来的财富效应。

2. 部分加密资产开始具备真实的基本面

一些代币(如 HYPE)和新的 IPO 项目(如 CRCL)开始展现出真正的基本面。当市场上出现了由基本面支撑的资产后,很难再去押注那些仅靠白皮书支撑的代币。

3. 与此同时,科技股表现优于加密市场。在许多情况下,与人工智能、机器人、生物技术和量子计算相关的股票收益超过了加密市场的表现。这让散户投资者不禁疑惑:为什么要冒险投资山寨币,而「真实」的公司却提供了更高的回报,且看似风险更低?甚至连 NASDAQ 今年以来的表现都超过了比特币和山寨币。

结果是什么?

· 表现不佳的山寨币成了一片「墓地」;

· 团队们在日益稀缺的资本池中激烈竞争;

· 经验丰富的加密投资者也变得无所适从,像无头苍蝇一样四处寻找投资方向。

归根结底,代币要么代表了一个业务的权益,要么就是毫无价值的。它们并不是一种神奇的新事物,仅靠存在就能获得价值。

如果你停止将代币视为难以理解的东西,而是将它们看作是代表企业未来现金流的资产,一切都会变得更加清晰。

但你可能会抗议说:「Dynamo,有些代币并不赋予未来现金流的权利!有些代币是功能性(Utility)代币!有些协议同时拥有代币和股权!」但你错了。这些代币仍然代表了未来的现金流;只不过,它们关联的现金流恰好是 0 美元。

最终,代币要么提供了业务中的权益,要么毫无价值。它们并不会因为「存在」或「社区」而自动获得价值(如许多人所认为的)。

需要注意的是,这一观点不适用于像比特币(BTC)这样的网络币种,因为它们更接近于商品的特性;这里讨论的是协议代币。

在不久的将来,唯一具有实际价值的 DeFi 代币将是那些作为伪股权存在的代币,并且满足以下两个条件:

1. 对协议收入的主张权;

2. 协议收入足以使其成为一个有吸引力的价值主张。

散户与加密市场「分手」

散户投资者暂时告别了加密市场。

一些头部 KOL 高喊「犯罪是合法的」,却对人们不愿成为「犯罪」受害者感到惊讶。

从目前来看,散户对绝大多数代币已经失去了兴趣。

除了之前提到的原因,还有一个重要因素是:人们对亏钱感到厌倦。

1. 过度膨胀的承诺:许多代币的价值建立在无法兑现的承诺之上。

2. 代币数量的泛滥:由于 memecoin 发行平台的兴起,市场上代币数量严重过剩。

3. 掠夺性代币经济学:行业对毫无价值的代币的容忍,导致散户正确地认为自己注定会「接盘」。

结果是什么?那些原本会购买加密资产的人,转而寻找其他满足「赌博欲望」的出口,比如:体育博彩、预测市场、股票期权。这些选择未必是明智的,但购买大多数山寨币也谈不上是好主意。

但是能责怪这些人吗?

一些 KOL 一边讨论「犯罪是合法的」,一边却对人们不愿成为受害者感到意外。

这种公众对加密市场的冷漠情绪,也反映在对行业的兴趣上。今年的热情远未达到 2021 年的高度,尽管当前的基本面比以往更好,监管风险也比以往更低。

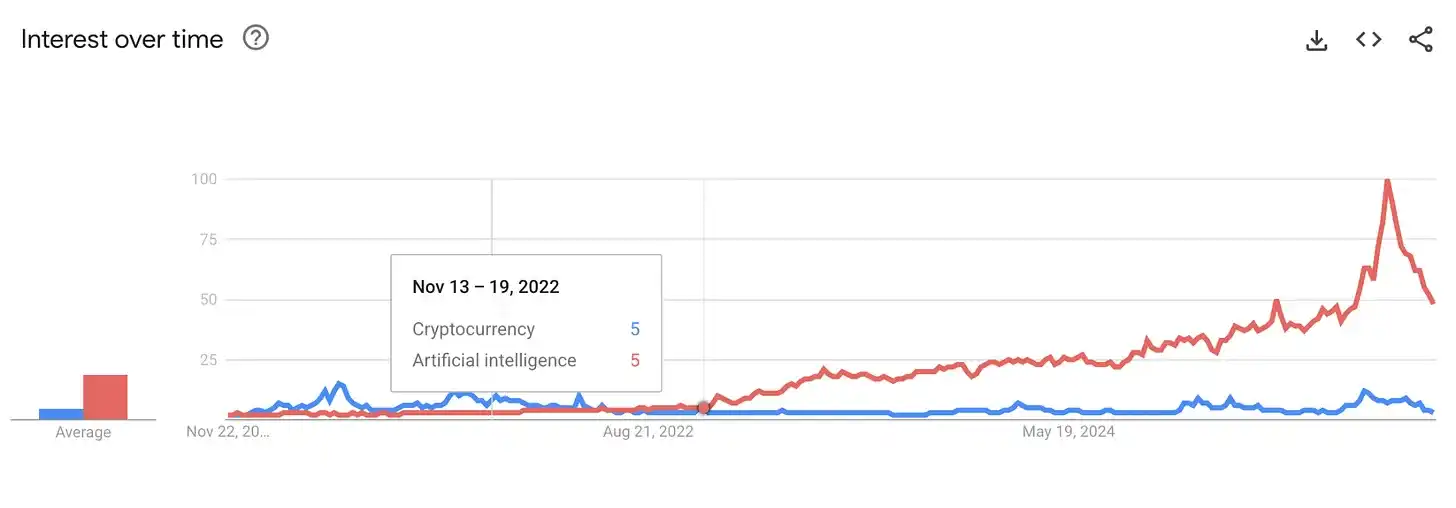

我还认为,ChatGPT 以及随之而来的人工智能热潮减弱了人们对加密货币的热情,因为它向新一代人展示了什么才是真正的「杀手级产品」。

过去十年里,加密爱好者们一直在谈论加密行业是一个新的「互联网泡沫时刻(Dot-Com Moment)」。然而,当人们每天都能看到人工智能以更加直观、明显的方式重塑他们的世界时,这种说法就变得更难令人信服了。

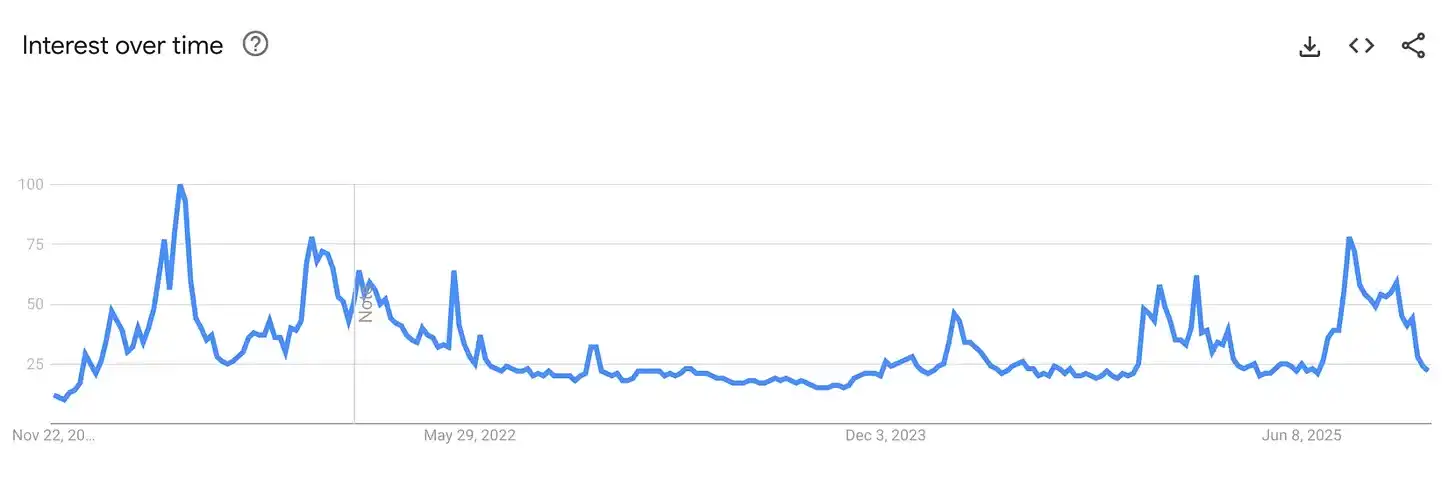

在搜索引擎上的关注度上,加密与 AI 的差距显而易见。上一次加密货币在 Google 上的搜索兴趣超过 AI,还是在 FTX 崩盘期间:

散户会回归加密市场吗?

答案是:会。

可以说,散户今天已经回归了某种形式的预测市场,但他们买的是关于「政府停摆何时结束」的二元期权,而不是山寨币。如果想让他们再次大规模购买山寨币,他们需要感受到自己有合理的机会获利。

代币价值的核心来源:协议收入

在一个代币无法依赖于投机驱动的源源不断买家的世界中,它们必须依靠自身的内在价值站稳脚跟。

经过五年的实验后,痛苦的事实已经显现:代币价值积累的唯一有意义形式是对协议收入的主张(无论是过去的、现在的,还是未来的)。

所有这些各种形式的真实价值积累,最终都归结为对协议收入或资产的主张:

· 分红(Dividends)

· 回购(Buybacks)

· 销毁费用(Fee Burns)

· 金库控制(Treasury Control)

这并不意味着一个协议要想有价值,今天就必须执行这些措施。在过去,我曾因为表示希望我看好的协议将收入再投资而不是用于回购而受到批评。但协议需要在未来具备启动这些价值积累机制的能力,理想情况下通过治理投票或满足明确标准来触发。模糊的承诺已经不再足够。

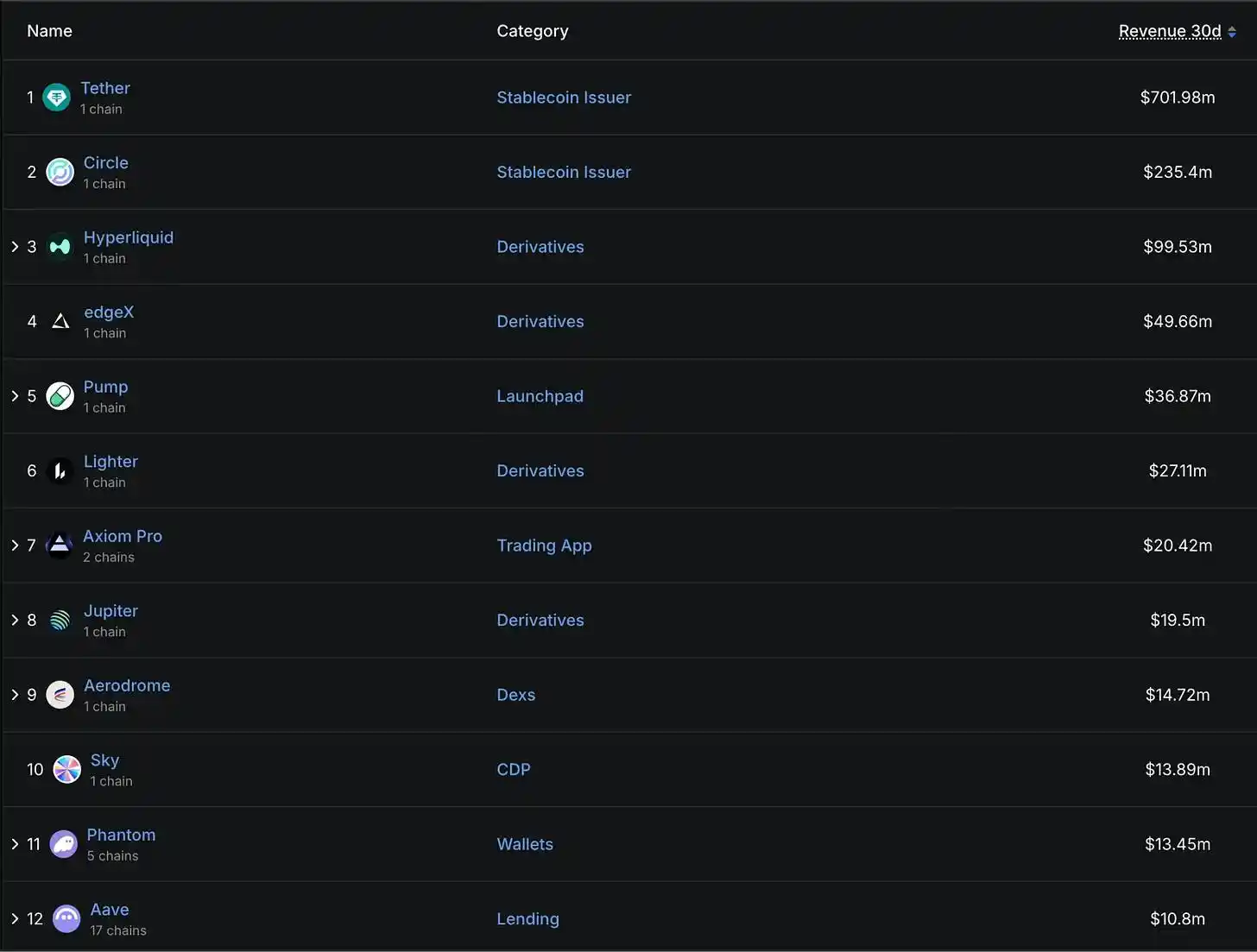

幸运的是,对于精明的投资者来说,这些基本面数据在像 DefiLlama 这样的平台上已经可以轻松获取,涵盖了数千个协议。

快速浏览过去 30 天内按收入排名的顶级协议,可以清晰看到一个模式:稳定币发行方和衍生品平台占据主导地位,同时 Launchpads(代币发行平台)、交易应用、CDPs(抵押债仓)、钱包、去中心化交易平台(DEXs)以及借贷协议也有所表现。

几点值得注意的结论:

1. 稳定币和永续合约是当前加密行业最赚钱的两大业务

2. 交易相关业务依然非常赚钱

总体来看,支持交易的业务利润丰厚。然而,如果市场进入长期熊市,交易相关活动的收入可能面临显著风险,除非协议能够转向交易现实世界资产(RWAs),正如 Hyperliquid 所尝试的那样。

3. 掌控分发渠道与构建底层协议同样重要

我猜测,可能有一部分硬核 DeFi 用户会强烈反对交易应用或钱包成为顶级收入来源,因为用户可以直接使用协议来节省成本。然而,在现实中,像 Axiom 和 Phantom 这样的应用却极为盈利。

一些加密应用每月能创造数千万美元的收入。如果你所关注的协议尚未达到这个水平,也没关系。作为负责 DefiLlama 收入的人,我深知开发一个市场愿意为之付费的产品需要时间。但关键在于,必须有一条通往盈利的路径。

玩乐的时代已经结束了。

面向价值导向的加密世界:投资框架解析

在未来几年寻找投资代币时,表现强劲的代币需满足以下标准:

1. 对协议收入的主张权或清晰透明的收入主张路径

2. 稳定且持续增长的收入和收益

3. 市值与过去收入相比处于合理倍数范围内

与其空谈理论,不如来看几个具体例子:

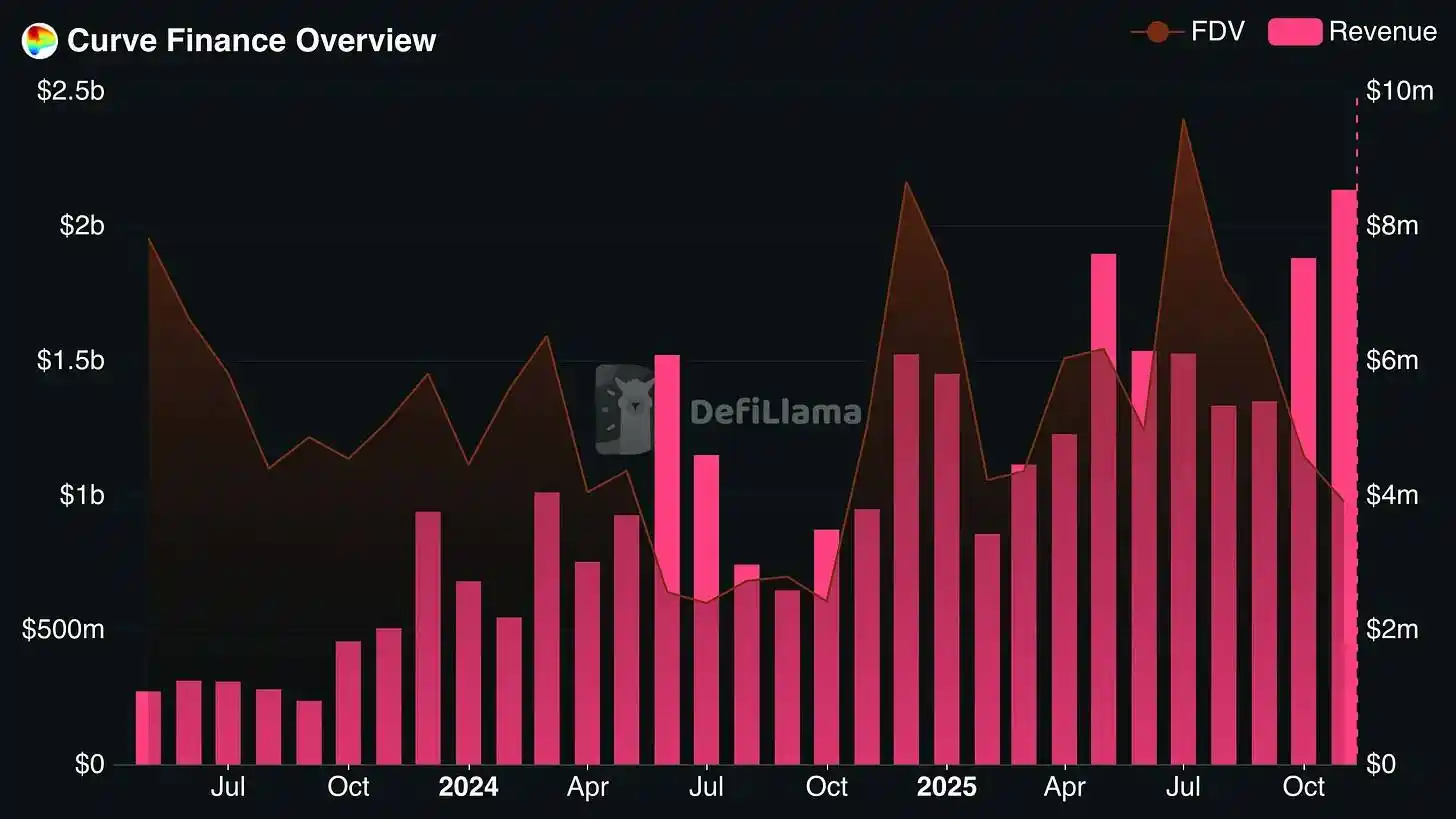

Curve Finance

Curve Finance 过去三年实现了稳定且持续的收入增长,即便完全稀释估值(FDV)有所下降。最终,其 FDV 已降至不足 Curve 过去一个月年化收入的 8 倍。

由于锁定 Curve 代币的持有者可以获得贿赂奖励(bribes),再加上代币释放周期较长,代币的实际收益率要高得多。接下来需要关注的是,Curve 是否能够在未来几个月中维持其收入水平。

Jupiter

Jupiter 已经稳固地成为 Solana 生态繁荣的主要受益者之一。它是 Solana 链上使用最广泛的 DEX 聚合器和永续合约去中心化交易平台(perp DEX)。

此外,Jupiter 还进行了多项战略性收购,这使其能够利用自身的分发渠道扩展至其他链上的市场。

值得注意的是,Jupiter 分配给代币持有者的年化收入相当可观,约占流通市值的 25%,并且超过了 FDV(完全稀释估值) 的 10%。

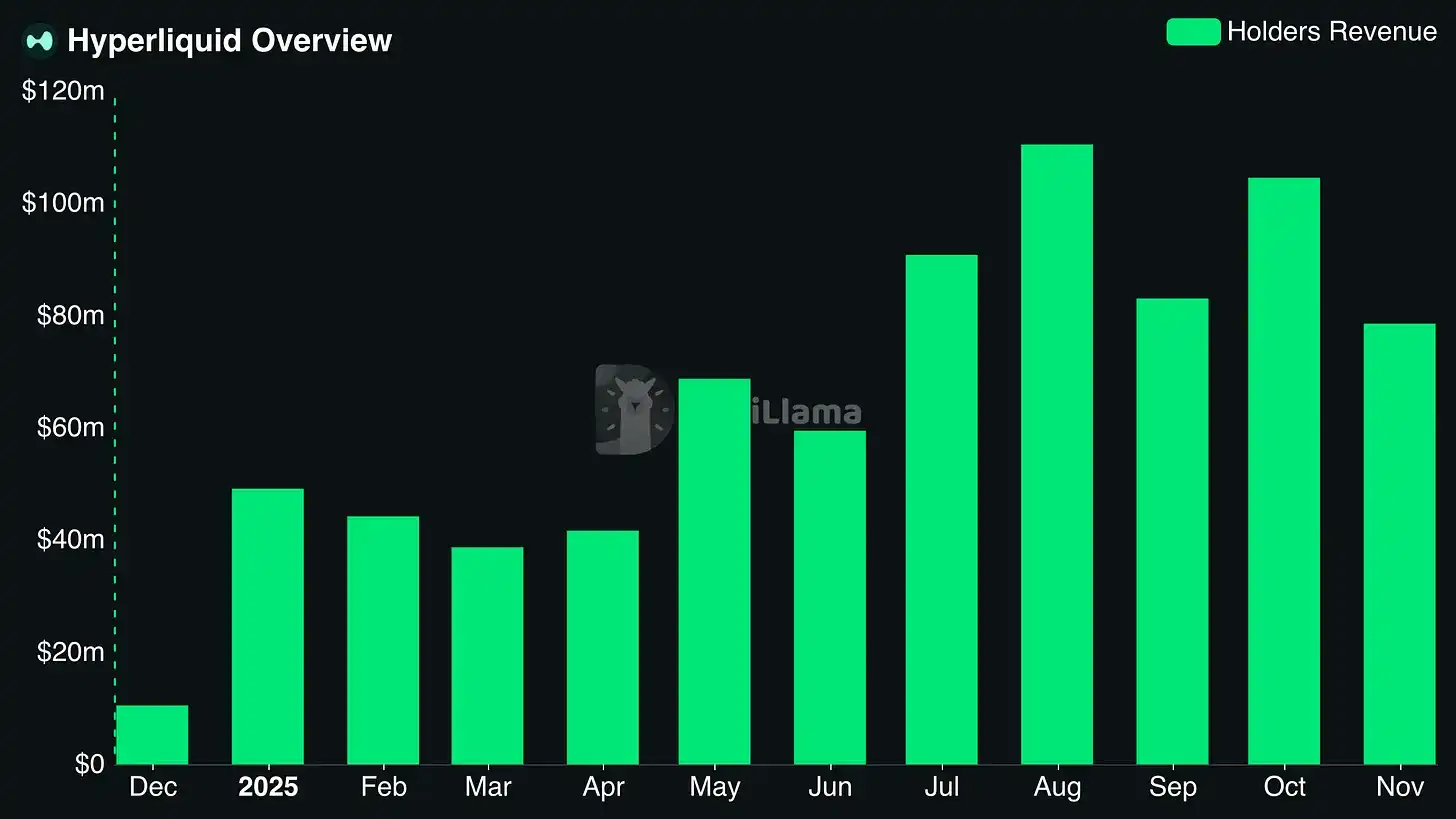

符合标准的其他协议:Hyperliquid、Sky、Aerodrome 和 Pendle

积极信号:希望之光

好消息是,那些真正关心自身生存的团队正在迅速意识到这一点。我预计,在未来几年内,由于无法无限制抛售代币的压力,将促使更多 DeFi 项目开发实际的收入来源,并将其代币与这些收入流挂钩。

如果你知道从哪里寻找,未来将充满希望。