Популярный в сообществе тезис о кризисе ликвидности первой криптовалюты не соответствует реальности, заявил глава отдела исследований биткоина CoinShares Кристофер Бендиксен.

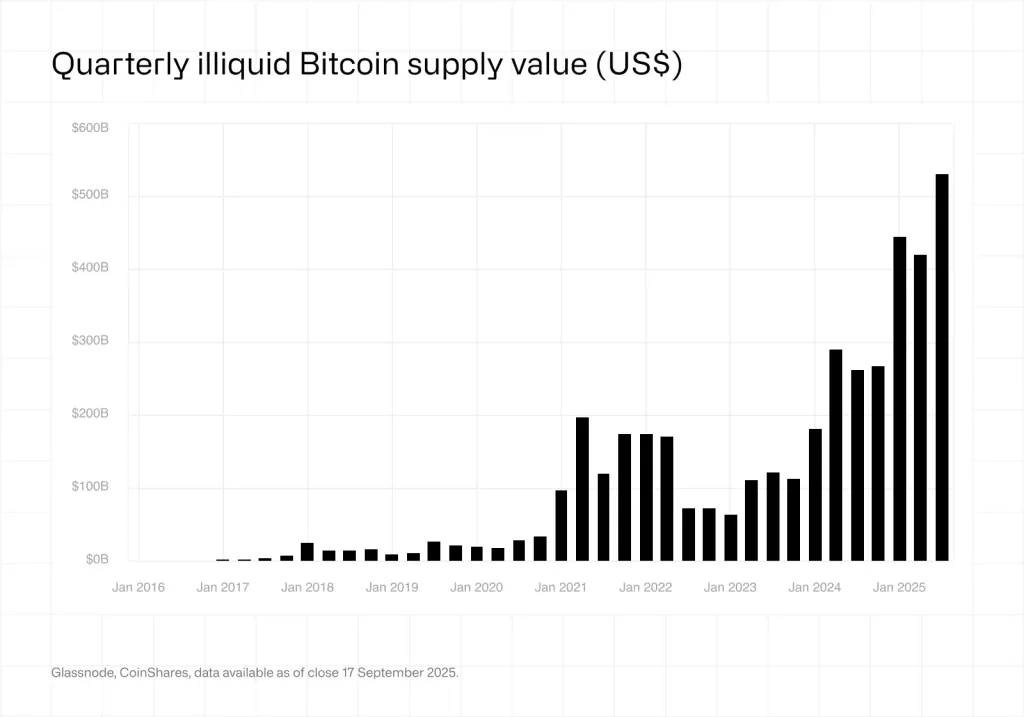

Эксперт разобрал два ключевых аргумента: сокращение остатков цифрового золота на биржах и увеличение монет в неликвидных UTXO. Он указал на ошибку в интерпретации — при оценке ликвидности важно учитывать не количество монет, а их стоимость в долларах.

«Даже при сокращении числа ликвидных биткоинов в штучном выражении их совокупная стоимость продолжает расти. […] Как видно [на графике выше], она увеличивается практически в той же прогрессии, что и неликвидное предложение, поскольку определяющим фактором здесь выступает цена», — пояснил Бендиксен.

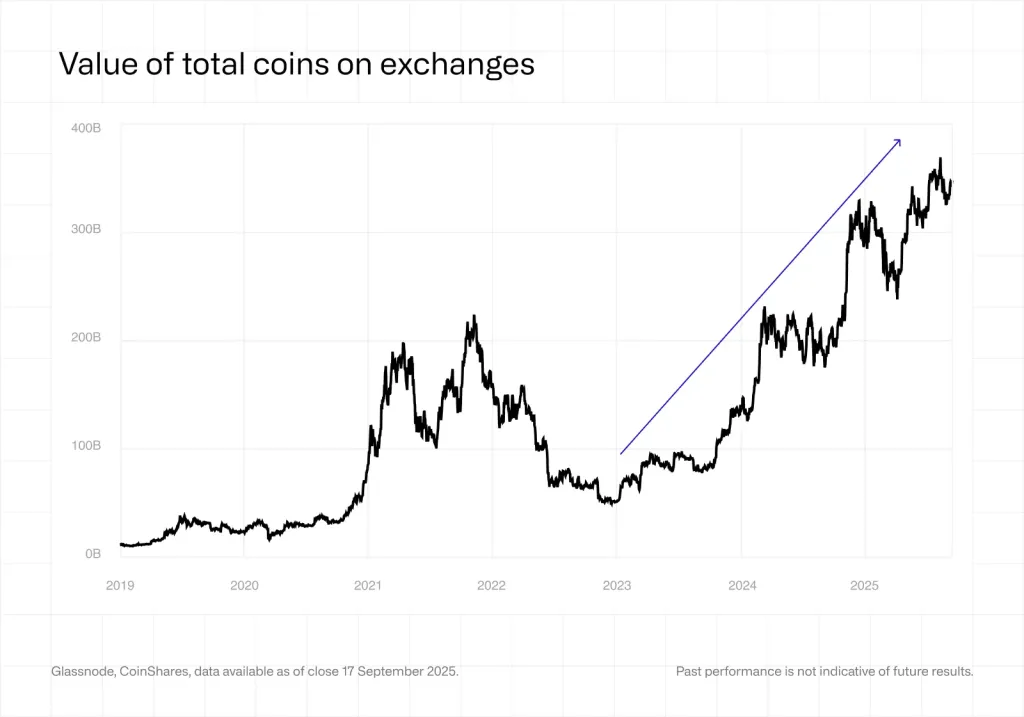

Эксперт также сделал график общей стоимости монет на биржах, который свидетельствует о том, что проблемы с ликвидностью нет:

«Объем доступной ликвидности почти вдвое превышает показатели пика последнего бычьего цикла, и к этому добавился новый крупный источник — биткоин-ETF, торгуемые на Nasdaq», — отметил он.

По его расчетам, для резкого ралли котировок необходимо, чтобы инвесторы скупали более миллиона монет каждый год по текущим ценам. Только такой масштаб спроса может создать дефицит и спровоцировать ажиотажный рост.

ETF стали ключевым источником ликвидности для биткоина

«Монет всегда будет достаточно»

Бендиксен считает, что «любого количества первой криптовалюты будет достаточно для удовлетворения любого долларового спроса». Он сослался на возможность цифрового золота бесконечно делиться (например, на сатоши).

По его мнению, представления о сокращении ликвидности до описываемых некоторыми экспертами уровней «выглядят оторванными от реальности». Единственный сценарий «свечи Бога» — коллапс спроса на доллар США как базовую валюту. Хотя в исторической перспективе такой исход возможен, в обозримом будущем он маловероятен, подчеркнул аналитик.

«Тем временем при устойчивом росте цены биткоина и медленной продаже давними держателями в ответ на новый спрос во время каждого ценового ралли, похоже, что монет достаточно для всех по любому преобладающему курсу», — подытожил он.

Напомним, трейдер под псевдонимом CrypNuevo допустил формирование цифровым золотом дна на уровне $101 000.