Крупнейшая международная платежная компания Western Union подала заявку на регистрацию торговой марки, охватывающей широкий спектр криптовалютных услуг, всего через день после анонса собственной стейблкоин-системы на блокчейне Solana (SOL).

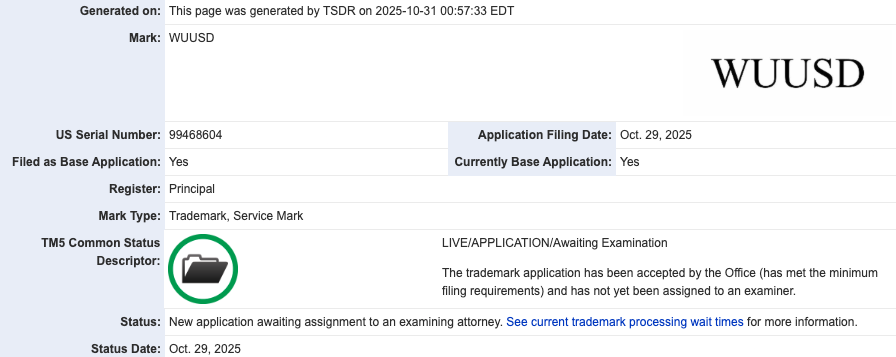

Согласно данным Ведомства по патентам и товарным знакам США (USPTO), Western Union Holdings, Inc. подала заявку на регистрацию марки WUUSD в 29 октября. Документ охватывает криптосервисы, связанные со стейблкоинами.

Заявка уже принята ведомством, но пока не передана на рассмотрение эксперту.

В описании указано, что торговая марка WUUSD может использоваться для криптокошельков, торговли цифровыми активами и обработки платежей в стейблкоинах, а также для других связанных продуктов.

23 октября компания объявила о планах по запуску собственного стейблкоина под названием US Dollar Payment Token (USDPT). Запуск актива намечен на первую половину 2026 года на блокчейне Solana.

Western Union также сообщила о создании Digital Asset Network совместно с банком Anchorage Digital Bank. Эта сеть должна стать инфраструктурой для вывода фиатных средств и поддержки операций со стейблкоинами компании.

По теме: Western Union протестирует переводы средств с помощью стейблкоинов

Пока неясно, чем будет отличаться WUUSD от USDPT. В заявке только указано, что WUUSD может использоваться для обмена и торговли стейблкоинами, а также для их обработки в платежных системах.

Документ раскрывает возможность более широкого спектра криптосервисов — от программного обеспечения для управления и проверки транзакций до инструментов, позволяющих тратить и торговать цифровыми активами.

Среди описанных направлений также криптобиржевые услуги, обработка платежей и брокерское обслуживание, связанное с торговлей криптовалютами.

Особое внимание вызывает пункт о криптокредитовании и операциях с ценными бумагами и деривативами, что может стать серьезным расширением традиционной бизнес-модели Western Union, основанной на денежных переводах.

Многие платежные компании и финтех-провайдеры проявляют интерес к стейблкоинам после принятия в США GENIUS Act в июле 2025 года, который внес больше определенности в регулирование стейблкоинов, привязанных к доллару.

По теме: закон уже позволяет выпускать стейблкоины — глава ЦБ РФ