撰文:Luke Leasure & Carlos

编译:AididiaoJP,Foresight News

本周 Meteora 即将发行其代币 MET:其公平价值可能在哪里?

指数

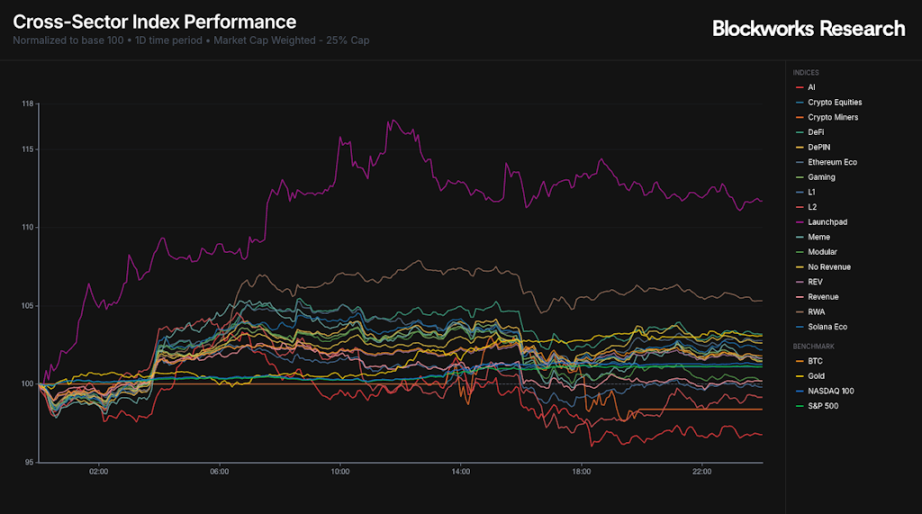

本周开局强劲,BTC 从上周五低点上涨了 7%。在周一的交易时段中,Launchpad 是表现最好的板块,而 AI 板块跌幅最大,扭转了各自在过去一周所展现的相对强弱态势。

从周线图来看,近期 Launchpad 的强势使该板块成为相对赢家,仅被黄金超越,后者在周一收盘时再次接近历史高点。总体上,在历史性的清算事件之后,大多数指数在周线上仍为负值。在 Launchpad 指数中,基于 BSC 的 Launchpad 项目 AUCTION 是周线上唯一显示正收益的标的,上涨了 46%。

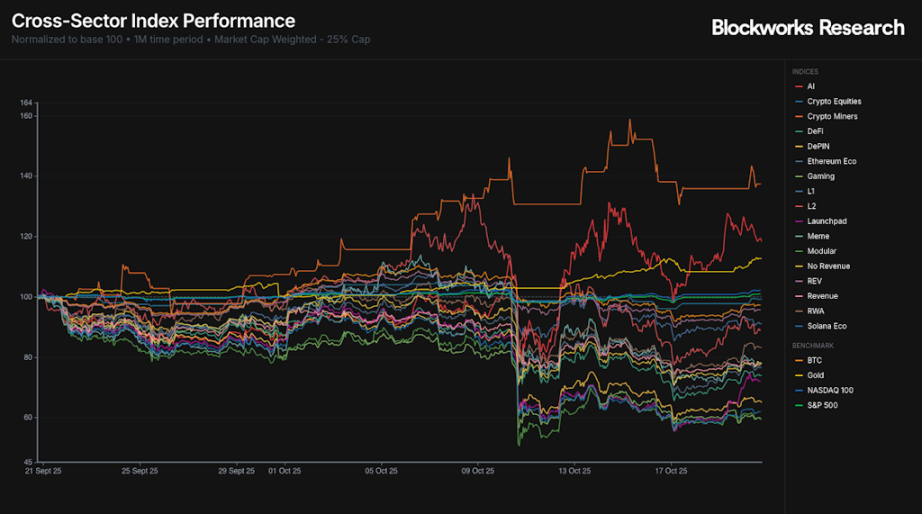

虽然短期显示一些上涨,但月线图显示几乎所有的加密货币指数在过去 30 天内都在下跌。10 月 10 日的清算事件导致了普遍的疲软,只有黄金、加密货币矿工、AI 和股票指数是表现强劲的领域。

VIX 指数已显著回落,在周五早上飙升至 29 后,现已降至 18。标普 500 指数和纳斯达克指数在周一的交易时段中均走高,收盘价距离历史新高仅一步之遥。

市场更新

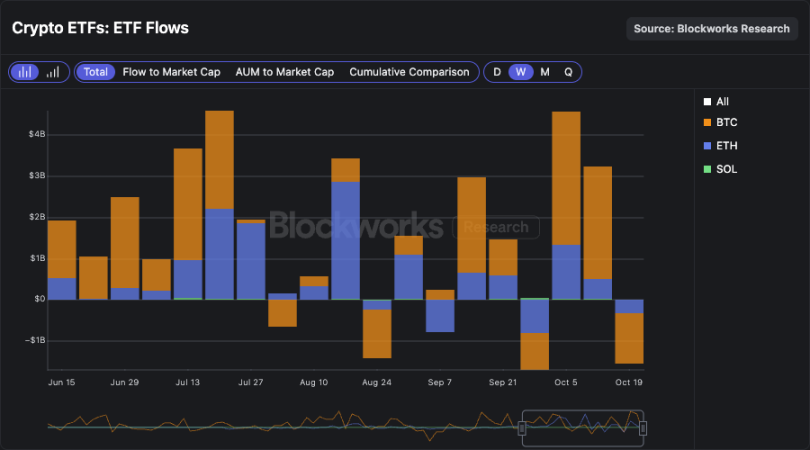

ETF 资金流仍然平淡且为负值。周一数据显示,BTC ETF 流出 4000 万美元,ETH ETF 流出 1.45 亿美元,而 SOL ETF 则流入 2700 万美元。从周线看,上周 ETF 净流出总额达 15 亿美元,逆转了 10 月份开局非常强劲时积累的部分资金。SOL ETF 是唯一显示净流入的产品,增加了 1400 万美元。

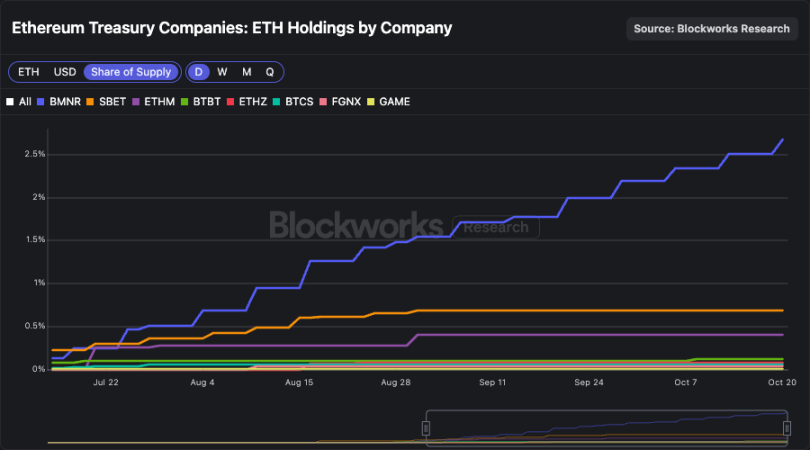

在 DATCOs 中,BMNR 遥遥领先。该实体目前持有 3,236,014 枚 ETH,超过了所有其他 ETH DATCOs 持有的总和,占 ETH 总供应量的 2.67%。值得注意的是自 8 月底以来,BMNR 持续增持了近 70% 的 ETH,而大多数其他 ETH DATCOs 的持有量则持平。在此过程中,BMNR 在 DATCOs 持有的 ETH 中所占的市场份额从 50% 增长到现在的接近 65%。

这种情况也反映在 ETH DATCOs 的交易量上。BMNR 占据了 ETH DATCOs 交易量的 60-85%,使其股票成为流动性最强的。这种流动性特征使得该实体获得了较大配置者的偏好,也减少了 ATM 增发对价格的边际影响。BMNR 似乎是 ETH 国库公司领域的明显赢家。

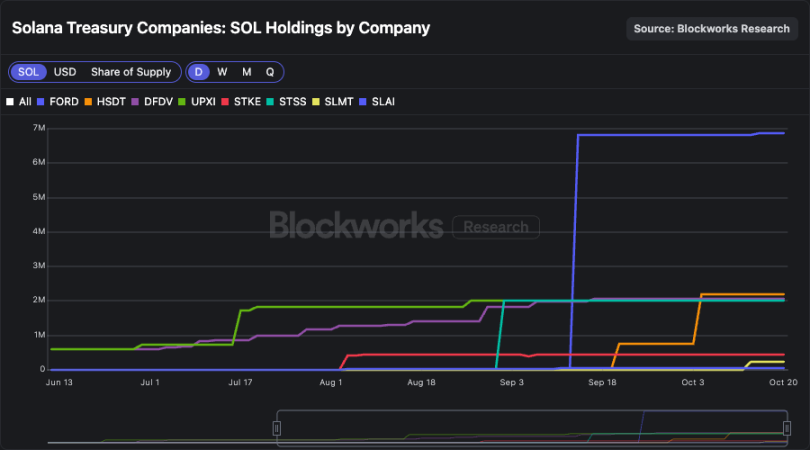

在 SOL DATCOs 中,情况则不那么清晰。FORD 仍然是持有量最大的实体,其几乎全部规模都是通过 PIPE 发行的收益获得的。尽管已授权一项 40 亿美元的 ATM 增发计划,该实体尚未通过 ATM 增发显著增加其持有量。

持有量的增长仍然疲软,HSDT 最近升至第二位。

SOL DATCOs 的交易量也讲述了类似的故事。虽然 DFDV 曾一度占据该领域交易量的大部分,但现在情况已转向顶级名称之间更均匀的分配。虽然 FORD 占据了 DATCOs 持有的 SOL 的约 43%,但它仅占该领域交易量的约 10%,表明其股票的换手率相对较低。这些数据可能很好地解释了为何通过 FORD 的 ATM 增发积累的 SOL 非常少。

虽然 BMNR 正成为 ETH 领域的明显赢家,但 SOL 领域的领导者可能仍悬而未决。在未来一个月,预计交易量将日益集中在头部公司。

Meteora 的 TGE:MET 的公平价值是多少?

备受期待的 Meteora TGE 将于 10 月 23 日星期四进行。与近期项目进行 ICO 趋势不同,Meteora 在 TGE 之前不进行融资。相反它将向符合条件的接收者进行空投,包括 Mercurial 利益相关者、Meteora 流动性提供者、JUP 质押者和 Launchpad 合作伙伴。空投接收者默认将收到未锁定的 MET,或者可以选择在启动时提供流动性以赚取交易费用。

Meteora 由 Solana 最大的 DEX 聚合器和永续合约交易平台 Jupiter 团队于 2023 年 2 月推出。当 Meteora 推出时,协议的前一个迭代版本 Mercurial Finance 被终止。关闭 Mercurial 及其治理代币的原因是有大量 MER 涉及 FTX/Alameda,因此团队决定最佳行动方案是使用新代币重建平台。

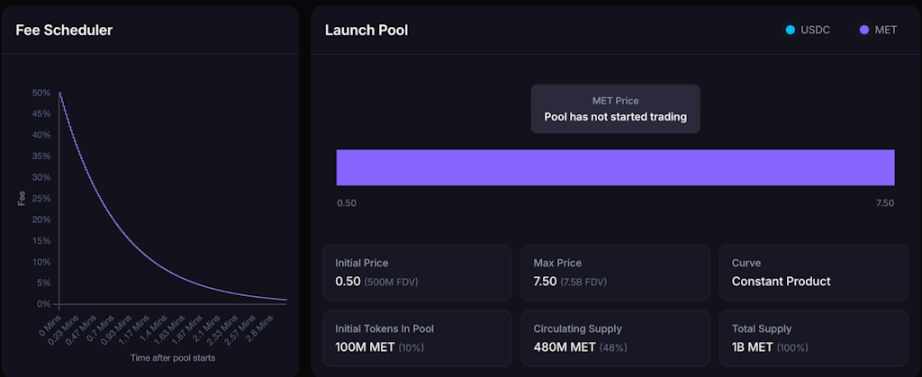

早在 2023 年,团队就宣布 20% 的 MET 代币将在 TGE 时分发给 Mercurial 利益相关者。如下所示,团队信守了最初的承诺,其中 15% 分配给 Mercurial 利益相关者,5% 分配给 Mercurial 储备。此外该 DEX 自 2024 年 1 月 31 日起一直在运行一个积分计划,总共将分配 15% 的 MET 给该计划。在启动时,MET 供应量的 48% 将处于流通状态,与 Solana 生态系统中其他著名代币发行相比,这是一个高流通比例。

来源: https://met.meteora.ag/

如前所述,总供应量的 10% 将用于通过动态 AMM 池引导初始流动性,起始价格为 0.5 美元,流动性分布范围直至 75 亿美元估值。早期流动性池是单边的,早期买家将用他们的 USDC 兑换 MET。请注意,池费用开始时很高,并通过费用调度程序随时间急剧下降。

来源: https://met.meteora.ag/

估值计算

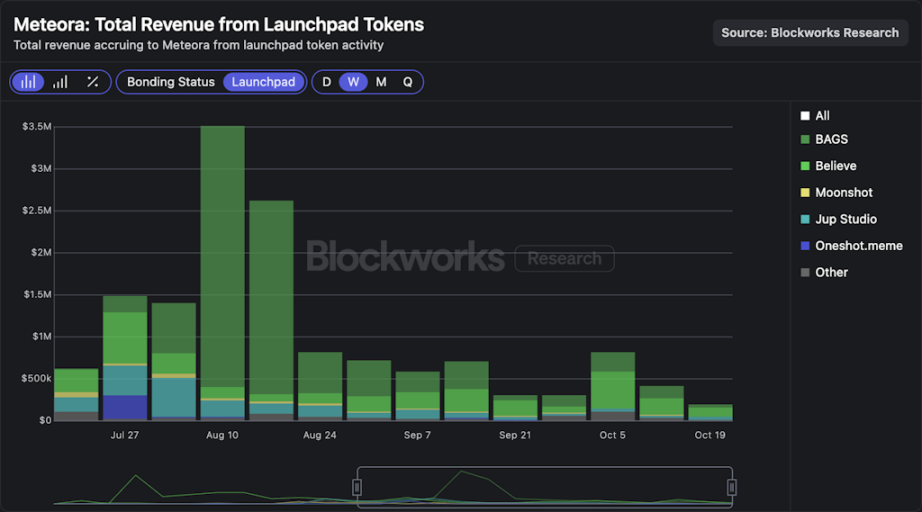

DEX,尤其是在 Solana 上,缺乏显著的护城河,因为它们没有前端。这种动态的最佳例子是 Raydium 在 Pump 决定将毕业代币引导至其自己的 AMM PumpSwap 后,损失了数百万美元的交易量和收入。Meteora 试图通过垂直整合来缓解这个问题,通过 Jupiter 和选定的 Launchpad 合作伙伴扩展其分发能力。

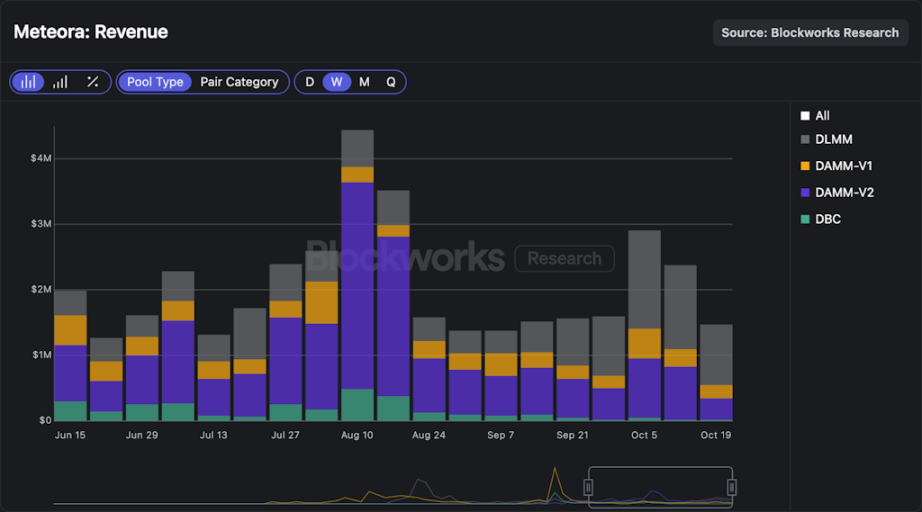

如前所述,该 DEX 与 Jupiter 团队紧密合作,Jupiter 已成为零售用户进行链上交易的常用门户。此外 Meteora 于 2024 年 8 月与 Moonshot 合作推出了一个 Launchpad,并随着时间的推移引入了新的合作伙伴,包括 Believe、BAGS 和 Jup Studio。下图显示,最近几周 Launchpad 活动为 Meteora 贡献了每周 20 万至 80 万美元的收入,其中大部分流量来自 Believe 和 BAGS。

从整体财务数据来看,Meteora 在过去 30 天内从其所有资金池中产生了 880 万美元的收入,即使在链上活动相对较低的时期,每周收入也持续接近 150 万美元。值得注意的是,Meteora 超过 90% 的收入来自 Memecoin 资金池,这些池通常比 SOL- 稳定币、项目代币、LST 和稳定币 - 稳定币池具有更高的费用等级。

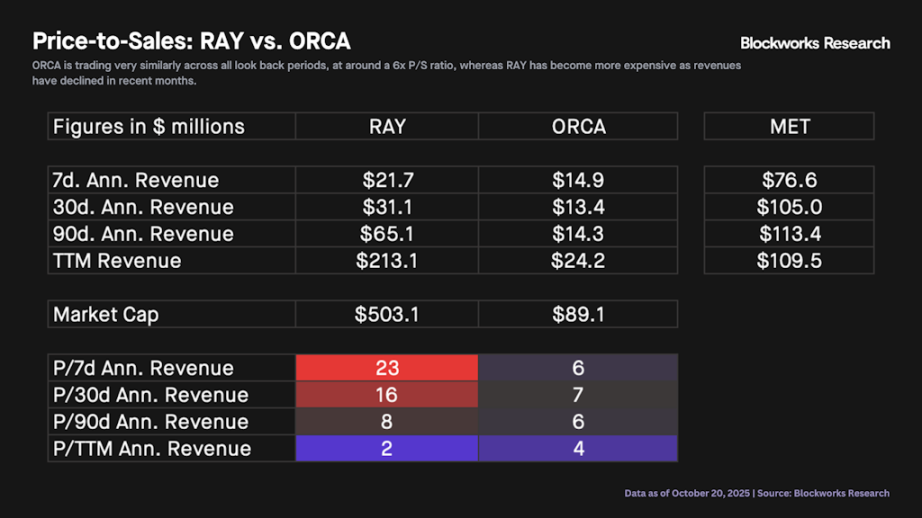

关于估值,我们可以将 Raydium 和 Orca 作为可比公司。下图显示了 RAY 和 ORCA 今年至今基于 30 日年化数据的市销率。我们观察到,直到 9 月份之前,这两种资产的定价比率相对相似,之后 RAY 开始以溢价交易。从更广的视角看,这两种资产在 2025 年的市销率中位数为 9 倍。

下表比较了 RAY 和 ORCA 在不同回顾期内的市销率。我们观察到 ORCA 在所有年化时间框架内的交易情况非常相似,市销率约为 6 倍。相比之下,随着收入下降,RAY 在最近几个月变得更为昂贵。就 Meteora 而言,我们看到其年化收入在约 7500 万至约 1.15 亿美元之间,具体取决于回顾期。

最后,下图展示了 MET 在不同收入和市销率范围内的潜在估值。基于 RAY 和 ORCA 的历史定价方式,市销率在 6 倍到 10 倍之间是最有可能的。因此可以合理地预期 MET 在启动后的交易估值在 4.5 亿到 11 亿美元之间。请注意基于以下数字,估值超过 10 亿美元相对于可比公司开始显得有点昂贵,而超过 20 亿美元则 MET 几乎肯定被高估,除非它能提高其收入运行率。