撰文:深潮 TechFlow

两个月前,Pudgy Penguins 的小企鹅刚在纳斯达克敲了钟。各大圈内外机构,如 Coinbase 和 VanEck 等, 还为它集体换过头像。

似乎对小企鹅来说,将自己的IP传播更广,成为了这个圈内为数不多幸存的 NFT 项目的发展主线。

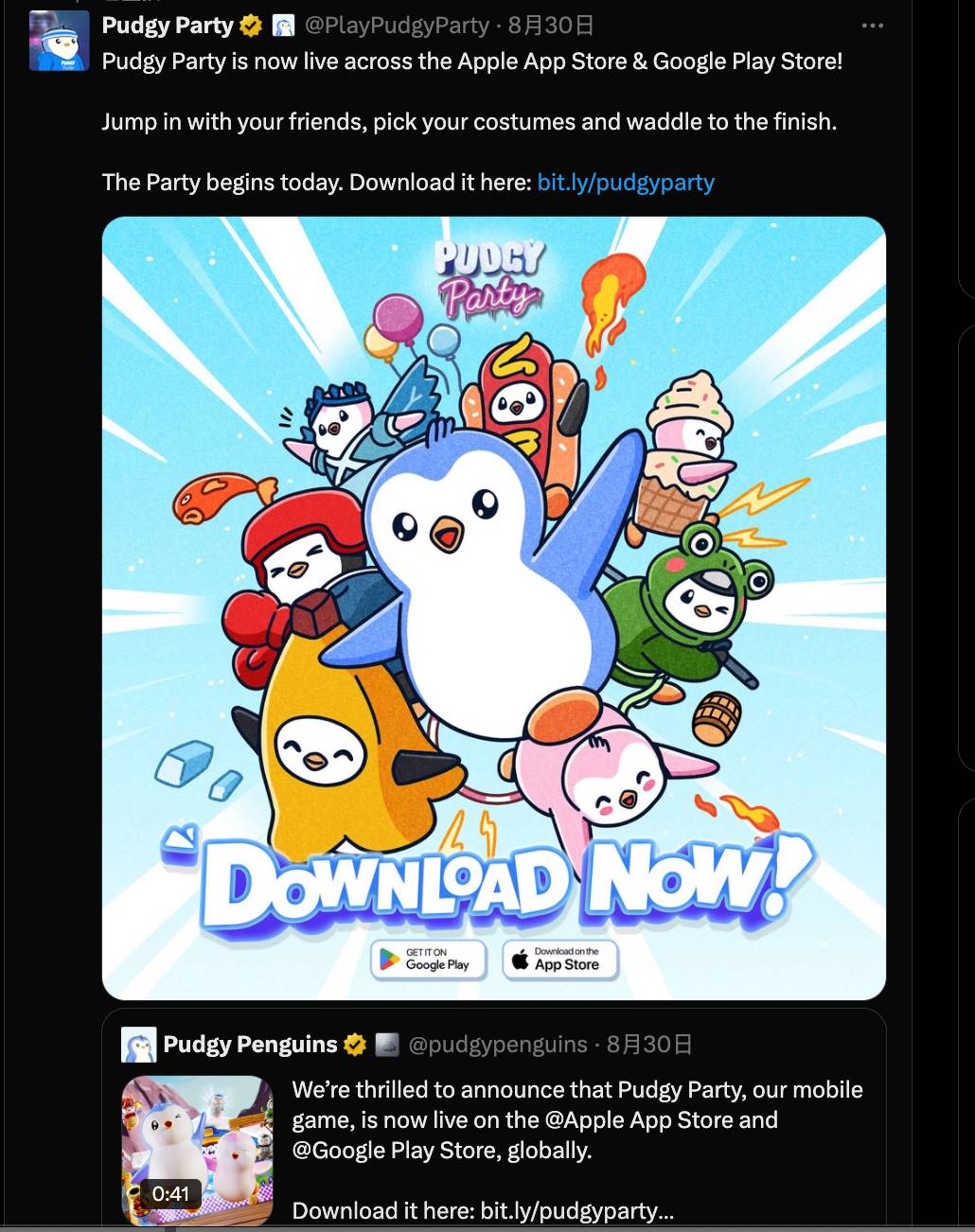

而在 8月30日,Pudgy Penguins 的新游戏 Pudgy Party 上线各大手机游戏商店,更进一步将自己的 IP 也游戏化了。同时,据一些海外 KOL 分析,该游戏登录商店后,一度来到了免费游戏榜的前10。

小编最近也下载了这个游戏试了下,发现它和上个周期刻意强调加密和游戏融合的链游有着很大的区别:

Pudgy Party里没有钱包连接、没有NFT商城、没有链上代币奖励...什么都没有。这就是一个普普通通的手机派对游戏,和你在 App Store 随便下载的休闲游戏没什么两样。

更有意思的是,游戏还挺好玩的。

如果你玩过糖豆人,那肯定在进入游戏界面时会会心一笑,一个多人互相竞争闯关活到最后的小游戏,轻松休闲没有任何“打金”的气息,纯净的甚至没有加密味。

一个NFT项目做了个完全不提NFT的游戏,在体验了一阵子后,我也想想聊聊这个"不太Web3"的Web3游戏。

没有链,只有游

打开Pudgy Party,第一反应是钱包连接在哪?没有。

那 NFT Marketplace 呢?也没有。代币奖励系统?还是没有。

作为对比,上个周期的链游标杆Axie Infinity,你需要先买三只NFT宠物才能开始游戏。StepN需要买NFT鞋子。即便是相对"轻度"的链游,至少也会在显眼位置放个"Connect Wallet"按钮。

如果不是 Pudgy Penguins 标志性的小企鹅形象出现在游戏里,你可能会以为这就是个普通的派对游戏。

点击"Play",几秒钟匹配后,你就会和其他19个玩家一起进入第一轮游戏。每个人控制一只憨态可掬的企鹅,在各种奇奇怪怪的关卡里比赛。

从体验来看,这是一个纯休闲 + 小企鹅 IP 的游戏。

比如一个典型的障碍赛跑关卡,20只企鹅就是20个玩家,在一条充满陷阱的赛道上狂奔,前面是旋转大锤、移动的平台、突然倒塌的地板。你要做的就是别掉下去,跑到终点就行。

但当20只企鹅挤在一起时,场面就变得特别混乱和好笑:有人被锤子抡飞,有人在独木桥上被挤下去,还有人明明快到终点了却踩空掉落。

是那种轻和链游这两个字不沾边的轻松。

第一,没有段位压力。游戏虽然有等级系统,但纯粹是为了解锁新的企鹅皮肤和动作表情,不影响匹配;

第二,输了也有奖励。即使第一轮就被淘汰,你也能获得经验值和一些装扮碎片。系统还很贴心地显示"Better luck next time!"配上企鹅的安慰表情。

第三,随时可以退出。中途退出没有任何惩罚,也没有啥学习各种升级和资源投入进行打金的环节。

特意寻找了一下是否游戏里会藏一些加密元素,但事实证明确实没有,至少游戏一开始没有。

游戏商店里确实有两种装扮,不可交易的和限量版的;理论上限量装扮可以变成NFT。但问题是,你找不到任何铸造或交易的入口。

但根据开发商 Mythical Games 的说法,游戏确实有Web3元素:

首先,每个玩家会自动创建一个基于 Mythos Chain(Polkadot生态)的钱包。但这个钱包完全在后台,用户看不到地址、私钥、助记词,什么都看不到。你甚至不知道这个钱包是否真的存在。

最后是PENGU代币。官方说"正在探索整合方案",但游戏里完全没有代币的影子。没有质押、没有奖励、没有消费场景。

换句话说,所有Web3功能都处于"画饼"和设计的极为克制的状态;这种去Web3化很可能是刻意为之。

大人,时代变了

从时机看,Pudgy Party 发布时正值加密市场的叙事重构期。

GameFi叙事已经冷却,Play to Earn模式被证明不可持续,大家对链游和 NFT 早已祛魅,更有一种“狗都不玩”的调侃。

更重要的是,Apple和Google对含有NFT交易功能的应用仍有诸多限制,之前也有新闻显示各大应用商店要求对所有NFT交易抽取30%的佣金,这对Web3游戏来说几乎是致命的。

从受众看,Pudgy Penguins显然想触达更广泛的用户群体。全球手游玩家超过30亿,而活跃的链上用户可能不到1亿。如果一开始就设置Web3门槛,就自动排除了99%的潜在用户。

从产品策略看,这像是一种"特洛伊木马"策略。

先用一个好玩的免费游戏吸引用户,建立用户基础和游戏习惯,未来再逐步引入Web3元素。当用户已经喜欢上游戏和IP后,接受钱包和NFT的阻力会小很多。

其实上个周期里,很多链游项目基本也在后期采用了这个模式,但都没有持续的长久做下去。这里的关键区别或许在于,小企鹅有着更强的IP号召力,用这个玩法做下去更容易见效。

这就带来一个有趣的悖论:一个Web3项目最成功的产品,可能恰恰是最不Web3的产品。

当 Pudgy Penguins 的毛绒玩具在沃尔玛卖到脱销时,买家其实不需要知道什么是NFT;当企鹅表情包在社交媒体疯传时,使用者甚至不需要连接钱包。

当Web3不再强调Web3

Pudgy Party的推出,可能标志着NFT项目发展思路的分水岭。

过去,NFT项目做游戏的逻辑是:我有NFT→持有者需要更多权益→做个游戏给他们玩→顺便发个币。这是一个由内而外的闭环,服务的是已有的几千个持有者。

Pudgy Penguins反过来了:做个好玩的游戏→吸引千万用户→他们可能会买玩具→极少数人可能买NFT。这是由外而内的漏斗,目标是圈外的手游玩家。

单纯依靠代币激励和投机炒作无法持续,真正的价值还是要回归到产品和用户体验。

更有趣的观察是,Pudgy Penguins 似乎把Web3元素变成了一个"高级选项":

-

普通用户:玩免费游戏,买个10美金的毛绒玩具

-

进阶用户:收集限量版装扮,参与社区活动

-

核心用户:购买NFT,持有PENGU代币

这有点像是互联网产品的"免费增值"模式,先用免费产品吸引海量用户,再从中转化付费用户。

只不过这里的"付费",变成了"上链"。

如果这个模式成功,意味着部分 Web3 项目找到了一条可持续的商业路径,即不依赖牛市,不依赖新韭菜,而是像正常公司一样靠产品和IP赚钱。

但代币怎么办?

这就是Pudgy模式的最大争议:如果不需要代币也能成功,那代币的价值支撑在哪里?

目前看,PENGU更像是Pudgy生态的股票,你买它是在赌这个IP会越做越大,而不是因为它有什么实际用途。

但换个角度想,迪士尼的股票也不能让你免费进迪士尼乐园,可这不妨碍它成为优质资产。关键是企业能否持续创造价值,而不是股票本身有什么"赋能"。

当然,这个类比并不完全恰当。

股票有分红和投票权,而PENGU目前什么都没有。这也是团队需要解决的问题,如何在不破坏产品体验的前提下,给代币持有者一些实在的好处。

如果说上个周期的叙事是"Everything on chain",那这个周期可能是"Chain as backend": 区块链退居幕后,成为技术基础设施而非产品卖点。

Pudgy Penguins可能无意中提供了一个落地的范例,即不是让所有人都变成crypto native,而是让crypto对普通人不可见。

至于这种模式能否成功,能否被其他项目复制,现在下结论还为时尚早。

但至少,Pudgy Penguins提供了一种不同的可能性:

在一个人人都在喊“Web3”的时代,最成功的可能是那个不提“Web3”的。