撰文:BUBBLE

加密货币 OTC 平台的发展以来有两个引爆点,对 2024 年来说是比特币和以太坊 ETF 的通过,而欧盟和迪拜等地区也逐渐引入了框架(MiCA、VARA),允许场外交易柜台合法大规模运营,机构需要快速采购标的资产。到 2025 年则是自美国总统特朗普提出「加密货币之都」的概念之后,传统金融的整体倾向 360 度大转弯,在出台各类加密新政之后,2025 年初比特币创新高、以太坊强劲上涨,机构资产配置热潮铸就 OTC 平台交易爆炸性增长。

通常来说 OTC 交易撮合是直接匹配买家和卖家。他们提供单一报价,因此其没有滑点没有竞价,转账通过托管钱包 、机构账户完成。因为订单永远不会触及公开的限价簿,所以市场永远不会看到你的手牌。作为「加密货币市场」的暗池,OTC 机构并不会公开自己用户的具体交易细则,但不同于传统金融,我们能从链上查询找蛛丝马迹。

2025 年 7 月发生了迄今最大规模之一的比特币场外交易,共 80,000 枚 BTC 以约 90 亿美元价格易手,但公开市场几乎无波澜,这一幕后操手便是当今最受华尔街欢迎的「加密场外交易机构」Galaxy Digital,这也让其 Q2 财报同比收入拉升了 268 倍。

OTC 平台在这股合规浪潮中究竟起了什么作用?Galaxy Digital 又是如何运用自己的资源在币股交易中翻转腾挪。律动 BlockBeats 就此选题进行了一系列的研究。

加密第三大流动性支柱

伴随这轮机构热潮,OTC 平台俨然已成为继中心化交易平台(CEX)和去中心化交易平台(DEX)之外,加密市场「第三大流动性支柱」。对于大额资金来说,CEX/DEX 难以直接承载数亿美元级别的买盘而不引发剧烈波动,于是 OTC 平台扮演了机构的「白手套」角色,代其在幕后完成建仓或清仓。

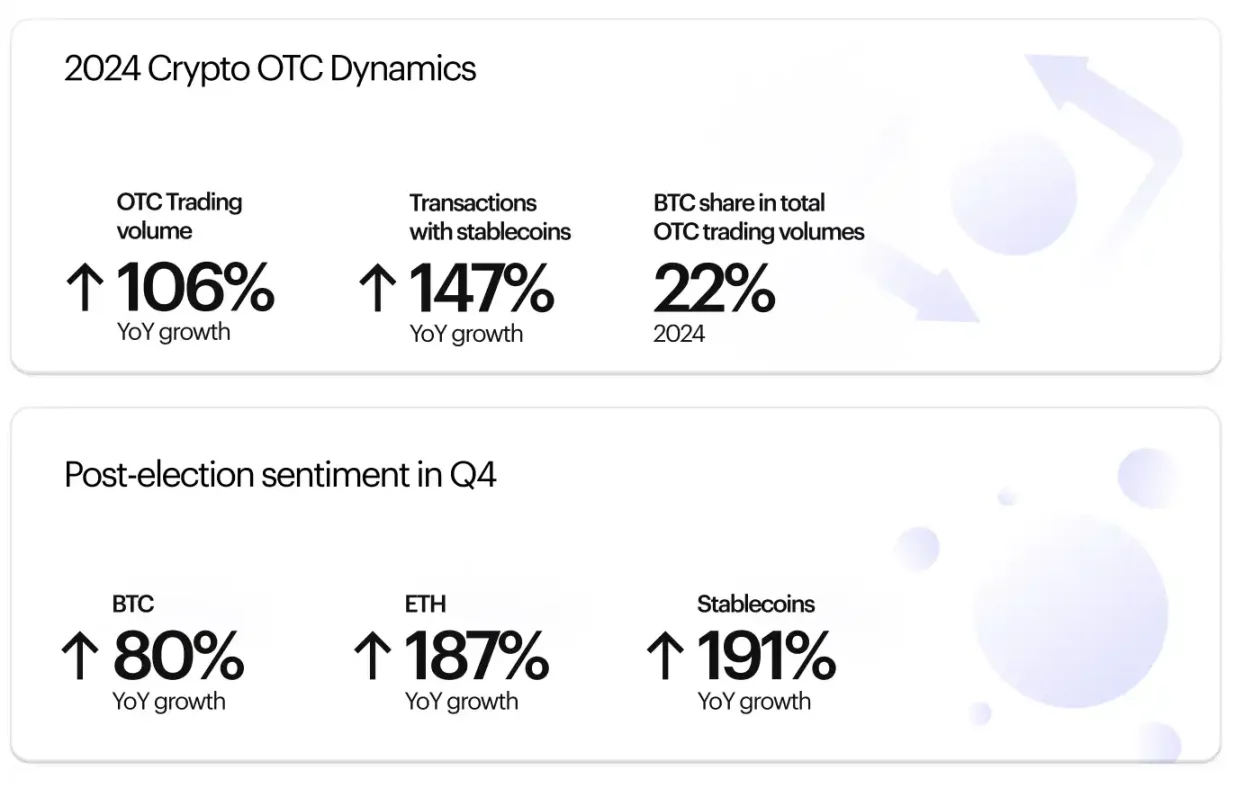

2024 年整年没有任何一个月的 OTC 交易量低于上年同期水平,表明市场参与者越来越倾向通过私密渠道交易,而非在公开市场明牌下注。加密行业在他们眼中从边缘投机逐渐变成了可接受的资产配置选项,华尔街从怀疑者变成了参与者。而在 2025 年这一增长情况更是指数性上升。

Finery Markets 指出,愈发多的传统金融领袖从观「望转向中立或接受」,是场外交易量飙升的重要原因。当更多交易在暗池中进行时,表面上的市场波动可能被显著平滑。根据 Finery Markets 公布的 2024 年 Q4 的报告,其中提到 OTC 平台的整体交易量较前一年需求量增长了 106%,2025 上半年 OTC 现货量较 2024 年上半年更是同比增长 112.6%。

值得注意的是,在欧美合规环境改善的同时,亚洲 OTC 市场也在兴起。香港持牌 OTC 平台 OSL、阿联酋及东南亚的新兴平台,均在吸引全球大单流动性。同时,一些传统大宗交易做市商如 Flow Traders 等也活跃其中,利用高频和量化策略为机构客户提供加密大额交易的双边报价,提高执行效率并降低冲击成本。这些因素共同巩固了 OTC 作为加密市场隐形水池的地位。

风头正盛的 Galaxy Digital

在众多 OTC 玩家中,Mike Novogratz 创立的 Galaxy Digital 无疑是这一波机构买盘狂潮中的明星。Galaxy 既是知名加密投行,又运营高触达的场外交易业务,主要涵盖交易、投资、资产管理、咨询和挖矿几条业务线。其客户涵盖上市公司、对冲基金等顶级玩家。但是其中盈利的主要支柱就是场外现货交易与投资。背靠着创始人 20 年华尔街从业经验以及公司上市的合规塑形,越来越多机构资金涌入,Galaxy 的平台上演了一幕幕惊人的大宗交易剧目,涵盖 ETH、BTC 等主流资产以及 SOL、BNB 等热门币种。

史诗级八万枚 BTC 交易平稳落地

前文提到 4 天内一次性 8 万枚比特币的 OTC,价值高达 90 亿美元一举创下加密史上最大的单笔交易之一,这场交易的中间商正是 Galaxy Digital。

Galaxy Digital 在 7 月 25 日发布公告,披露其受委托为一位「中本聪时代」的早期投资者完成了这笔巨额 BTC 出售。据称,这是该投资者进行遗产规划的一部分,Galaxy 并未透露客户身份,只表示交易是广泛财富管理策略中的一步。而令人惊讶的是这 8 万枚 BTC 的出清几乎没有冲击市场,从 7 月 17 日开始链上远古地址异动,在几天内将比特币转入 Galaxy Digital 的 OTC 地址,而这 8 万枚比特币的出清在比特币价格上却未体现,虽然几天后 Galaxy 的消息公布后短时下跌近 4% 并一度跌破 11.5 万美元关口,但几个小时内价格便迅速回升至约 11.73 万美元。

分析人士 Jason Williams 指出,这笔天量抛售已被市场「完全吸收」,另一位分析师 Joe Consorti 也感叹「80,000 枚比特币(逾 90 亿美元)以市价卖出,而 BTC 价格几乎纹丝不动」。一方面来说这再次测试了当前市场的 OTC 深度,在交易所撮合后短时间内有对手能够承接如此大量的卖单,另一方面也体现了「暗池交易」在如今的加密货币领域的重要性,事实上就现已公开的 OTC 地址(bc1q0)单地址依照市场情绪不同,Galaxy OTC Deck 每周经手的比特币总价值达数亿至数十亿美元,而现实情况可能比这个数字还多。

ETH 币股公司的偏爱

2025 年 Q2 以太坊链上出现多笔异常巨额买单,引发社区密切关注。自 7 月 9 日以来,有 14 个新钱包地址通过 Galaxy Digital 或 FalconX 等 OTC 台累计买入了惊人的 856,554 枚 ETH,价值约 31.6 亿美元,这些钱包均在链上一度毫无历史,然后突然在 OTC 渠道大额收币,显示有「大玩家正在悄悄增持 ETH」。

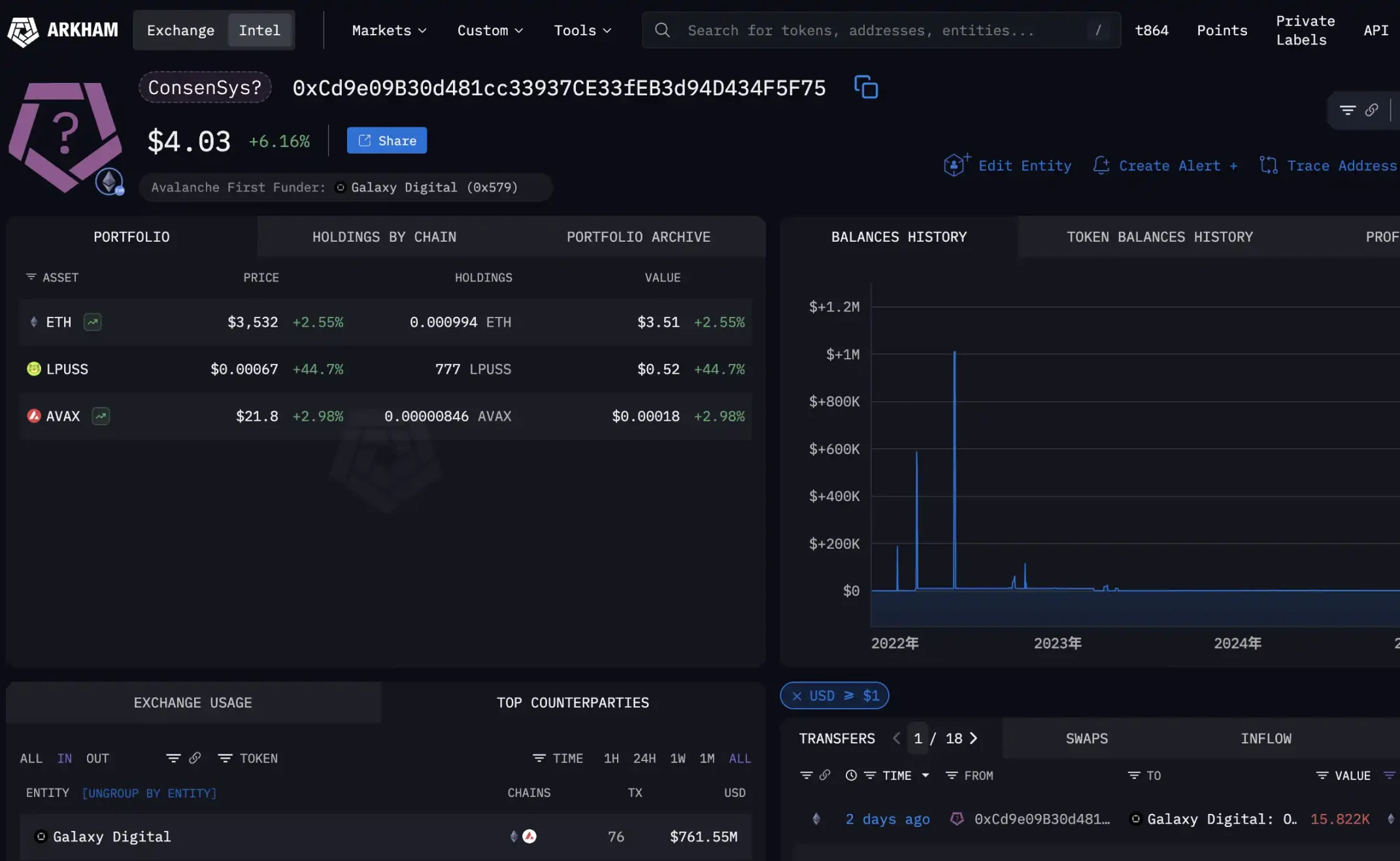

链上分析公司 Arkham Intelligence 指出,从 7 月下旬开始,一个新创建的钱包地址(0xdf0A…2EF3)在短短 3 天内通过 Galaxy Digital 的场外交易席位累计买入了价值约 3 亿美元的 ETH。该地址一度持有 79,461 枚 ETH,成本约 3 亿美元,按当时市值约 2.825 亿美元计算,账面一度浮亏约 2,600 万美元(约回撤 8.7%)。这表明该巨鲸买入均价相对较高,但依然在坚定加仓。

而仅仅在今天 8 月 5 日,就有 3 个新地址通过 Galaxy 和 FalconX 获取了共 63,837 ETH,价值约 2.36 亿美元。EyeOnChain 公示了其中一些买家地址,包括 0x55CF…679、0x8C6b…60、0x86F9…446 等。据推算,这些地址的累计买入力度分别达到数千万至数亿美元级别,有单个钱包持仓一度超 11 万枚 ETH(市值逾 4 亿美元)。

这一买盘究竟来自谁?有迹象将其指向 SharpLink Gaming,其自 2025 年 6 月起高调宣称效仿 MicroStrategy 战略,将以太坊作为主要国库资产持续增持。根据其公告和链上数据,SharpLink 在 6 月至 7 月底通过 ATM 增发融资和场外交易,疯狂扫货了将近 50 万枚 ETH,截至 7 月 27 日该公司持有 438,190 ETH,较一周前激增 21%,单周购入超 77,000 ETH,周均价约 $3,756。

截至 7 月末,SharpLink 累计购入约 44.9 万枚 ETH,进入 8 月,该公司继续逢低再囤 7 月 31 日再斥资 4,309 万美元买入 11,259 ETH,8 月 4 日再度从 Galaxy 处购入 18,680 枚 ETH。有分析称 SharpLink 的总持仓已突破 49.9 万枚 ETH,成本均价约 $3,064,目前市值约 18 亿美元,浮盈约 2.75 亿美元。如此大规模的以太坊买盘,几乎全程通过 Galaxy、FalconX 等 OTC 柜台完成,连 Wintermute 的创始人都开玩笑称「现在想在我们的场外台买到 ETH 几乎不可能,因为巨鲸们早已将供给一扫而空。除了当前 ETH 持币第二的 SharpLink 以外,当前 ETH 持币第一的 Bitmine 也是 Galaxy 的深度合作伙伴。

关联地址 0xCd9 目前已向 SharpLink 转移超过 8 亿美元的 ETH。1.53 亿美元的 ETH 0xdf0 、0x286 约 3 亿美元,等多个地址关联两者。

我们虽然无法一一理清如此密集的大额场外建仓都从何而来,但无论如何,这股暗流正在成为左右 ETH 供求的关键力量。律动 BlockBeats 根据几个 Galaxy 主要链上 OTC 地址的粗略计算过去 90 天在 ETH 的场外交易已经达到了 54.44 亿美元,月均处理约 18 亿美元的 ETH。

根据 Arkham 公开的四个 OTC 钱包 0x335、0x15、0x46f、0xb9c 四个钱包所得

又当裁判又当选手,MicroStrategy 戏码在 BNB Chain 上演

如果说 2024 年的主角是 BTC 和 ETH,那么 2025 年下半年开始,BNB 也登上了机构布局的舞台。7 月,一则令人意想不到的消息传出:美国纳斯达克上市的 CEA 工业公司(股票代码 VAPE,一家原主营农业温控和电子烟的公司)宣布将彻底转型为「BNB 国库公司」,拟通过私募融资和行权筹集最多达 12.5 亿美元资金用于购买 BNB,这一计划让 VAPE 股价单日暴涨 550%。

更引人注目的是,VAPE 此番加密 pivot 的操刀手正是 Galaxy Digital 的联合创始人 David Namdar。他将出任 VAPE 的新 CEO,另一位来自 10X Capital 的合伙人、前加州公共员工退休系统(CalPERS)首席投资官 Russell Read 则担任 CIO。Namdar 表示,将利用这笔高达 5 亿美元(最高可扩募至 12.5 亿)的资金在未来 24 个月内积极建立 BNB 头寸,包括公开市场购买、战略交易,以及通过质押和去中心化金融获取收益。

这意味着 BNB 将迎来首个大规模公开市场的机构买家,而 OTC 渠道无疑将在其中扮演关键角色。由于 BNB 的发行和流通高度集中,币安及其创始人赵长鹏 CZ 据报道控制了流通 BNB 的 71%,要在不引发市场剧烈波动的情况下吸收数亿美元的 BNB,只能求助于场外大宗交易或协议转让。Galaxy Digital 丰富的 OTC 网络和流动性资源,将为 Namdar 执掌的这场「BNB 版 MicroStrategy 行动」提供有力支持。BNB 作为全球第三大市值加密资产,此举标志着其正式进入机构资产配置视野。

不管是 Coinbase 主打的托管、交易、链上生态一体式的交易平台,还是 Galaxy Digital 这类咨询 +OTC 交易的币股关系的撮合,抑或是当前传统券商和交易平台的快速融合,加密货币领域的各个行业都开始走向合规化以及资源向头部聚合化转移。近日 Crypto Project 的启动可能便是这一显著趋向的公示,合规机构的霸权时代将近,而加密货币的 OTC 平台这一「透明的暗池」在未来可能占据更重要的生态位。