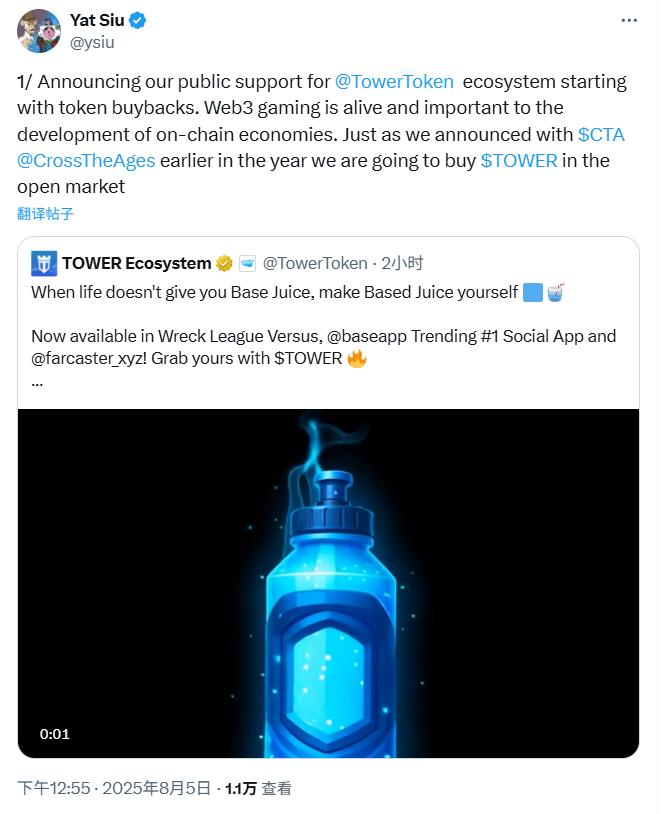

就在今天,2025年8月5日, Brands的联合创始人兼执行主席Yat Siu在X平台上发布的一则简短声明,却如同一颗投入静湖的石子,在Web3游戏领域激起了圈圈涟漪。他宣布,Animoca Brands将“公开承诺支持Tower生态系统”,并将启动TOWER代币的二级市场回购。

市场的反应颇为微妙:TOWER是谁?一个似乎还停留在2021年记忆深处的代币,为何在2025年的今天,被Animoca这位Web3巨头重新从“军火库”中翻出并高调擦拭?这仅仅是一次对旗下“亲儿子”的常规扶持,还是在整个GameFi赛道似乎错过了上一轮牛市的落寞背景下,Animoca Brands发出的一次深思熟虑的战略信号?

答案,远比一次简单的代币回购要复杂得多。

解构TOWER:一枚Web3的“活化石”

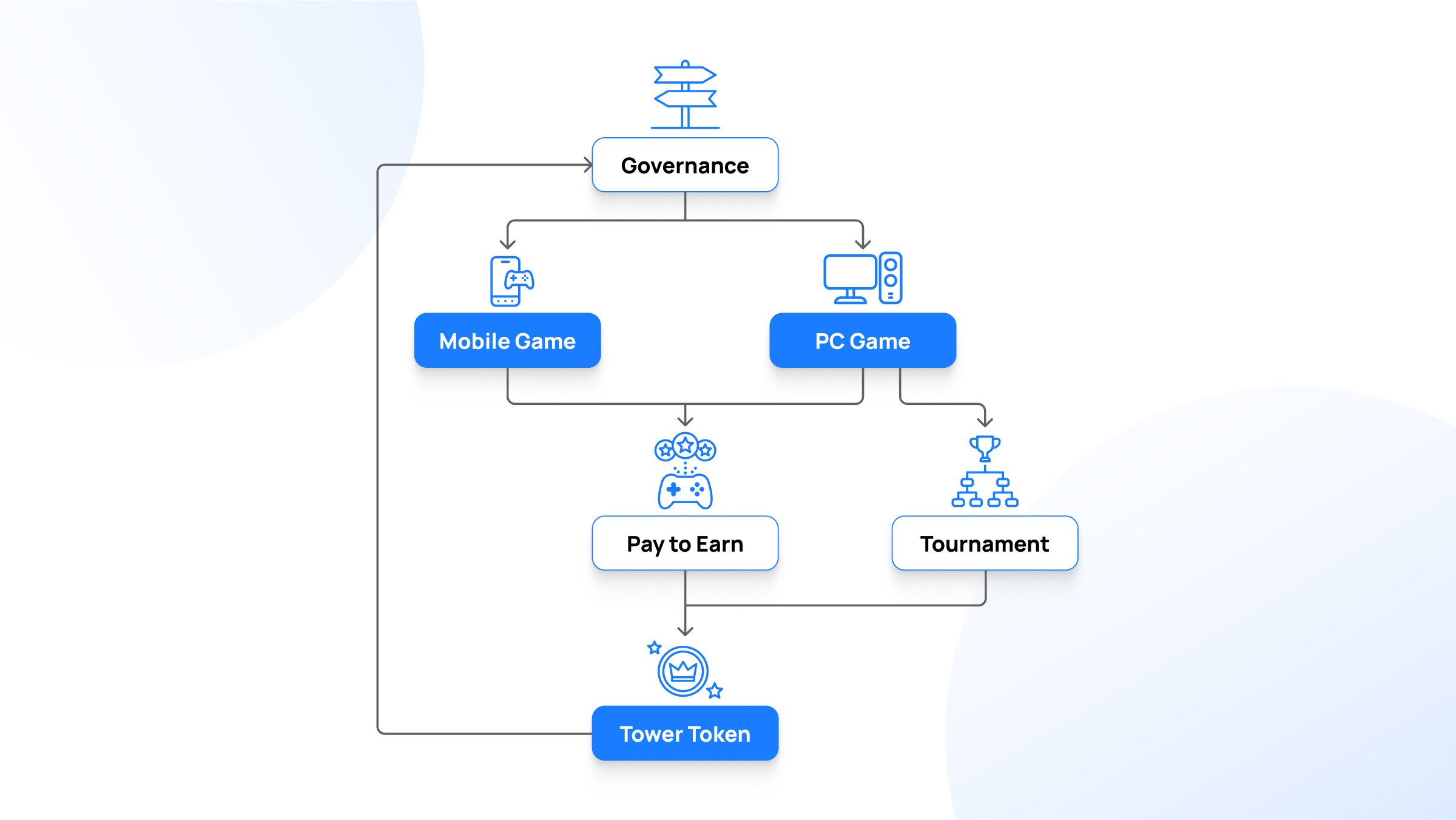

要理解Yat Siu的动机,我们必须先将时钟拨回。TOWER代币及其生态系统,本身就是GameFi赛道演进的一面镜子,甚至可以称之为一枚“活化石”。它诞生于2021年初,那是Play-to-Earn(P2E)概念最炙手可热的时代。Animoca Brands的构想极具前瞻性:将旗下早已获得市场验证的、拥有数百万下载量的免费手游(Free-to-Play),如《Crazy Kings》和《Crazy Defense Heroes》,与Web3的代币经济进行桥接。

这个模式的核心,并非创造一个全新的、以“赚取”为唯一目的的链上游戏,而是为已成功的游戏体验“附加”一个价值层。玩家在《Crazy Defense Heroes》中奋力拼杀,不再仅仅是为了虚拟的积分和徽章,而是通过每月达成一定的游戏内经验值(XP)目标,来赚取真正在链上流通的ERC-20代币——TOWER。这些代币可以在其官方网站上兑换独家的游戏NFT或参与特殊活动,形成了一个完整的“玩-赚-用”经济闭环。

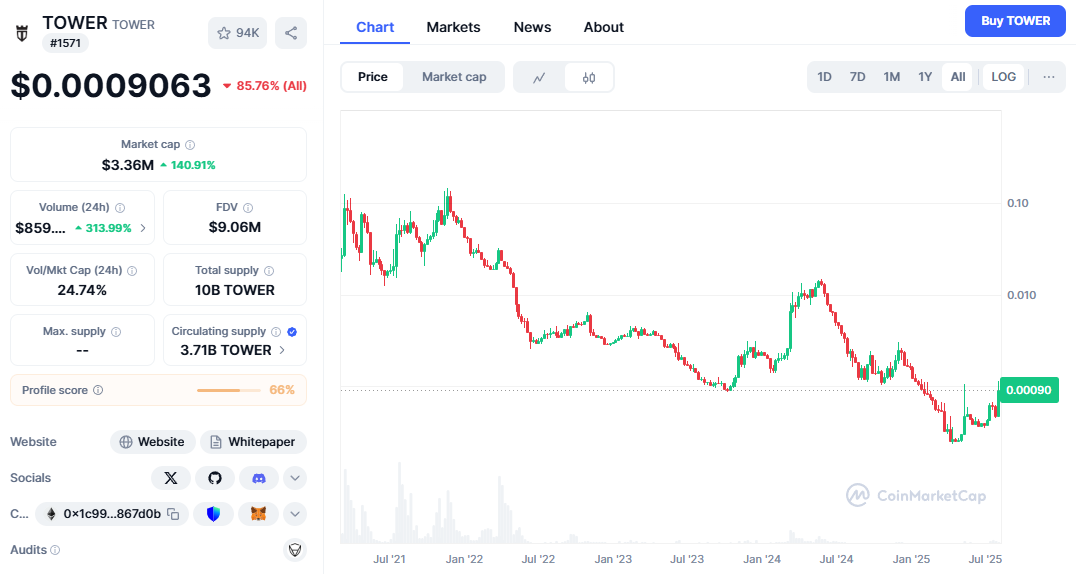

然而,理想丰满,现实骨感。伴随着2022年加密熊市的到来和第一代P2E模型的集体崩溃,TOWER也未能幸免。其代币价格从约0.14美元的历史高点一路下挫,跌幅超过99%,市值一度萎缩至不足200万美元。它就像那个时代大多数的GameFi项目一样,在经历了短暂的辉煌后,迅速被市场遗忘,静静地躺在无数用户的钱包深处。这个项目的初始代币分配(总量100亿枚,其中30%用于P2E奖励池,15%用于市场营销,15%为团队持有)在当时看是行业标准配置,但在流动性枯竭的市场中,这一切都显得那么无力。

动机探寻:Yat Siu的“标准操作”与价值哲学

如果TOWER只是一个失败的昨日黄花,那么Animoca今天的举动就显得毫无道理。但关键的线索,隐藏在Yat Siu声明中引用的一个先例里——他在推文中特意提到了“正如我们今年早些时候针对CTA的声明”。

这里的“CTA”,指的是另一个Web3游戏项目“Cross the Ages”。就在两个月前的2025年6月,Animoca Brands宣布与其达成战略合作时,就曾公开表示将“从二级市场购入CTA代币”。当时官方给出的理由是:Animoca旨在支持那些他们认为“价值被严重低估”且“致力于开发高质量Web3游戏”的生态伙伴。

将这套逻辑应用到TOWER身上,Yat Siu的意图便豁然开朗。截至声明发布前,TOWER代币的总市值仅约140万美元。这是一个什么概念?对于一个背后拥有着千万级下载量、至今仍在稳定运营的成熟游戏系列所支撑的代币项目而言,这个估值低得不成比例。Animoca Brands此时入场回购,不仅成本极低,更能以最直接的方式向市场传递一个强有力的信号:我们认为它被低估了,我们相信它的内在价值。

这并非一次心血来潮的“拉盘”,而更像是一次Animoca Brands投资哲学的“标准操作”。与其在外部寻找新的投资标的,不如回过头来,在自己庞大的投资版图中,激活那些拥有坚实基础但暂时蒙尘的资产。这是一种极其精明的“组合投资管理”策略,只不过是以公开市场操作的形式演繹出来。

GameFi的“失落牛市”与路径反思

Yat Siu的行动,恰好发生在一个对GameFi而言略显尴尬的时间节点。回顾过去一年多的牛市,DePIN、AI、Solana生态乃至各类Memecoin都曾轮番上演财富神话,唯独GameFi赛道,除了少数几个头部项目偶有波澜外,整体表现平平,似乎被主流叙事所遗忘。

究其原因,是第一代GameFi留下的“后遗症”太过深刻。以Axie Infinity的早期模型为代表,那种将“Earn”(赚取)置于“Play”(可玩性)之上的设计,催生了大量以打金为唯一目的的“游戏矿工”,其螺旋增发的代币模型在市场下行时被证明是不可持续的。这种模式的脆弱性,让整个行业对GameFi产生了信任赤字。投资者和玩家都在问:我们究竟是在“玩游戏”,还是在“玩庞氏”?

而TOWER的模式,在今天看来,反而提供了一种不同的解题思路。它的游戏本体——《Crazy Defense Heroes》——首先是一款好玩的、能够依靠自身品质吸引并留住玩家的F2P游戏。TOWER代币是锦上添花的奖励层,而非游戏得以成立的基石。这种“Play-and-Earn”(边玩边赚)的理念,而非“Play-to-Earn”(为赚而玩),正被越来越多的人视作更健康、更可持续的发展方向。

同样在进行反思和迭代的还有Gala Games。面对代币通胀压力,Gala在2023年果断地执行了大规模的代币销毁,并转向其自研的GalaChain,试图从根本上优化其经济生态。这些案例表明,GameFi赛道并未消亡,它只是在经历一场深刻的、必要的集体反思与内部重建。

从“增量扩张”到“存量激活”:Animoca的新棋局

将所有线索串联起来,一幅关于Animoca Brands未来战略的清晰图景便浮出水面。作为Web3领域最庞大的投资帝国之一,Animoca旗下拥有数百个投资项目和子公司。在经历了前几年的高速“圈地”、追求广度的增量扩张阶段后,其战略重心似乎正在悄然转变。

新的棋局,是“存量激活”——即深入挖掘并激活其庞大投资组合内部的潜在价值。TOWER项目无疑是这盘新棋局中一枚完美的“过河卒”。它拥有成功的游戏IP、庞大的现有玩家基础、一个功能完备的代币系统,以及一个被市场极度低估的价格。启动回购,就像一个四两拨千斤的杠杆,以最小的成本,撬动了市场的关注、安抚了现有社区,并向生态内所有其他项目方传递了一个信息:母公司会在关键时刻提供实实在在的支持。这无异于一次精准的“内部定向刺激计划”。

有趣的是,在我们对TOWER生态的研究中,并未发现一份清晰的、面向未来的长期发展路线图(Roadmap)。这在追求“画饼”能力的加密世界中显得有些另类。但这或许也正是Animoca新策略的一部分:告别僵化的、宏大的长期承诺,取而代之的是更敏捷、更具机会主义的战术干预。一次代币回购、一场与新伙伴的联动、一轮精心设计的游戏内活动,这些务实的举措可能比一份华丽的PDF文档更能带来实际的价值。

总而言之,Yat Siu关于TOWER的声明,其意义远超一次单纯的财务操作。它既是对当下GameFi发展困境的一次深刻回应,也是市场从狂热走向成熟的必然反思,更是Animoca Brands这位Web3棋手在棋局中盘阶段落下的一步意味深长的棋。

GameFi或许错过了上一场盛大的舞会,但像Animoca Brands这样的掌舵者显然没有弃船而去。他们正在做的,是回到机舱,仔细检查每一个引擎部件,将那些布满灰尘的“传家宝”重新打磨光亮,为下一段截然不同的航程做准备。这段新航程,将不再依赖于投机泡沫,而是建立在可持续的经济模型和被市场验证过的真实价值之上。Yat Siu的信号,不仅关乎TOWER的未来,更是在安静而坚定地告诉整个行业:游戏,还远未结束。