作者:kkk,BlockBeats

7 月 30 日,加密交易平台 Kraken 传出正以 150 亿美元估值寻求筹集约 5 亿美元融资的消息,引发市场高度关注。这一消息恰逢美国监管环境逐步转暖:2025 年 3 月,美国证券交易委员会(SEC)正式撤销对 Kraken 的证券违规指控,而就在上周,《财富》杂志披露 FBI 也已结束对 Kraken 创始人的相关调查,Kraken 由此摆脱多重监管阴影。与此同时,Kraken 官方社交媒体频频暗示潜在的上市计划,进一步激发市场想象。

此前 CRCL 在 6 月完成 IPO 后最高涨幅一度高达 10 倍,为市场预期提供了强烈对照。若 Kraken 成功上市,或将再掀一轮情绪高潮——值得关注的是:哪些标的将成为这场盛宴中的「炒作先锋」?

Pre-IPO 投资热潮来袭,散户也能抢跑上市前

随着 OpenAI、SpaceX 等顶级公司长期维持私有化,大量原始员工和早期投资者希望在上市前提前变现手中股权。而 Forge 正是连接这些「想卖」的人和「想提前买」的投资者的交易市场。如今 Kraken 的上市预期被炒热,若其员工或机构开始抛售股权,Forge 等私募股权交易平台可能成为散户押注的间接入口。

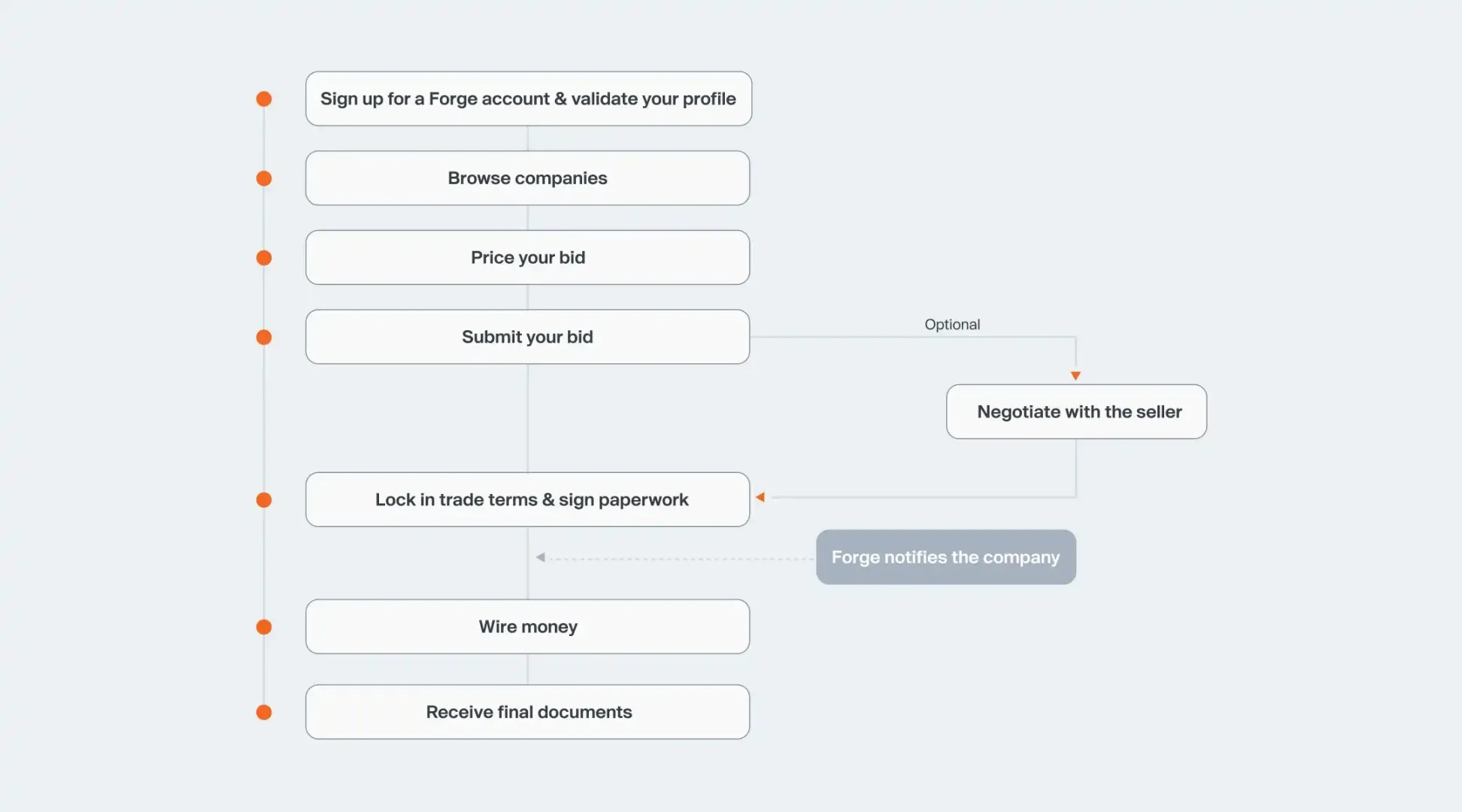

在 Forge 平台上,投资者通常可以通过两种方式购买未上市公司的股份:第一种是直接交易,即你找到某位愿意出售 Kraken 股权的持有者,与之协商价格。Forge 会协助完成 KYC、尽调与合约签署流程。第二种是通过 SPV 交易(Forge Funds),Forge 会设立专门的特殊目的实体(SPV),汇集买家资金后统一购买目标公司股权。你所持有的是 SPV 的份额,而非公司股票本身。这种方式绕开 ROFR,更适合想快速入场的投资者,甚至可在几天内完成交易。等 Kraken 真正 IPO 后,SPV 也有望获得流动性兑现。

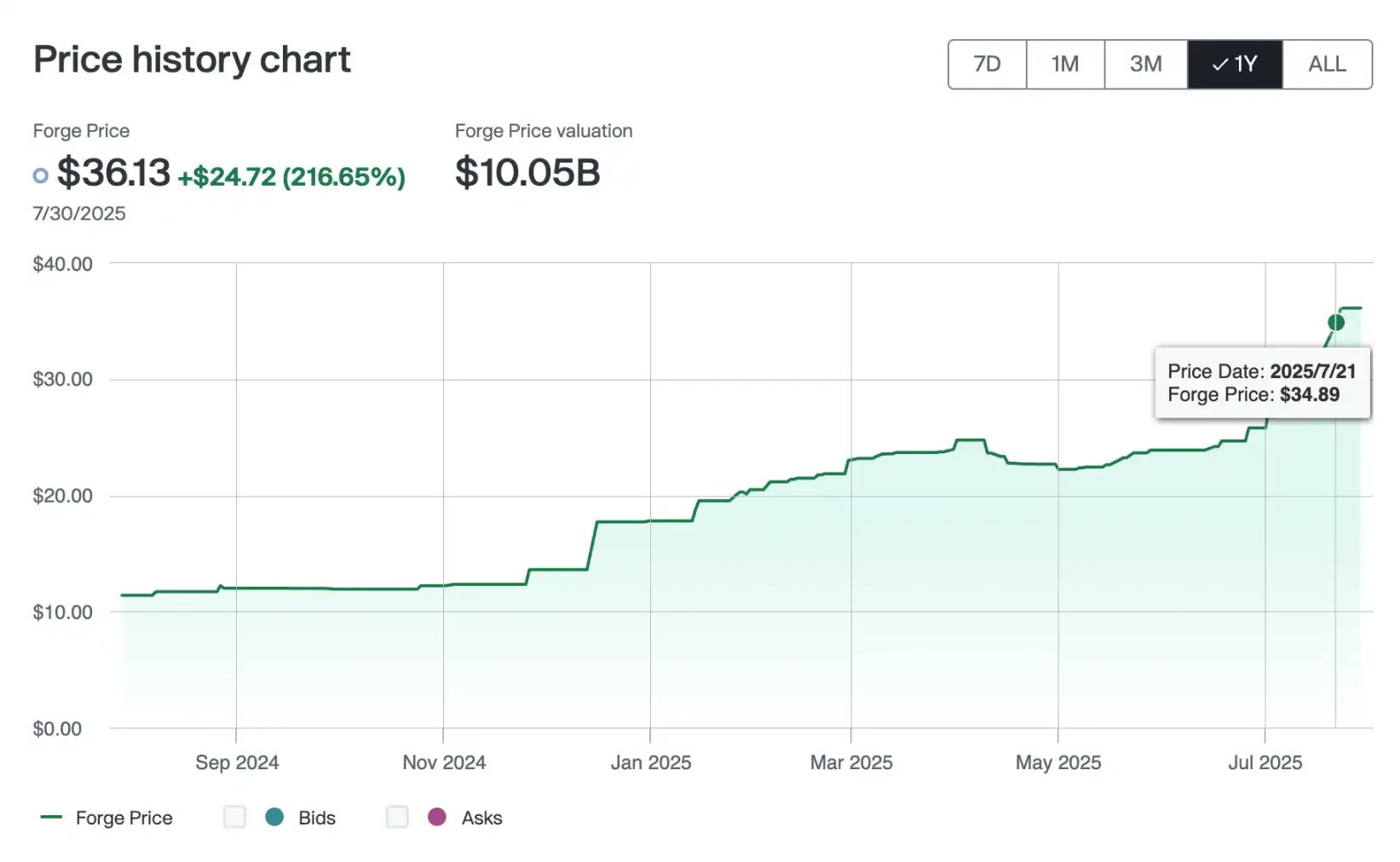

目前 Forge 平台上的价格为 36.13 美元,一年内涨幅高达 200%,体现了市场对 Kraken 上市预期的热情。估值约为 100 亿美元,如果 Kraken 能够顺利以 150 亿美元估值上市,当前入场者或将获得超过 50% 的超额收益。

此外,私募股权的代币化也正在给散户带来全新的投资机会,包括 Republic、Robinhood 等平台已支持 OpenAI、SpaceX 等科技公司,未来是否也将支持 Kraken,同样值得持续关注。

对标 Coinbase 的 Base 链,Ink 成为下一轮 L2 叙事核心

继 Coinbase 推出的 Base 链成为 Layer 2 板块的流量中枢后,Kraken 也正式入局,以 Ink 网络 打响了其 Layer 2 战略的第一枪。Ink 是一条基于以太坊 OP Stack 构建的 Layer 2 区块链,主打高速吞吐、低延迟和对以太坊虚拟机(EVM)的原生兼容,旨在成为 Superchain 上的 DeFi 中枢,为未来的交易、支付及链上金融基础设施提供坚实的底层支撑。该网络由 Kraken 牵头推动,其原生代币 $INK 将由子公司 Ink 基金会发行,并通过 Kraken 交易平台的空投计划分发给符合条件的活跃用户与生态参与者。尽管目前尚未公布具体的分发标准与时间表,但这一消息已成为市场的焦点。

6 月 17 日,Ink 基金会宣布 $INK 总量将永久封顶为 10 亿枚,无增发、无治理权,仅用于生态激励与用户层使用,定位更接近于「燃料」属性,而非传统的治理代币。首个明确的应用场景是由 Aave 驱动的原生流动性协议,这是 Ink 推进 onchain capital stack 的关键一环。该协议将借贷机制原生集成至 Ink 链上,为用户提供高效便捷的链上资金调度服务。

Kraken 联合 CEO Arjun Sethi 表示,Ink 的使命是将「生产级的链上系统」深度整合至 Kraken 产品体系中,推动中心化平台向链上金融体系的战略性迁移。而 Ink 基金会董事会则将此称为「一个关键时刻」,认为 Ink 的启动标志着 CeFi 与 DeFi 开始融合,也是全球统一资本市场愿景迈出的实质一步。

随着主网已正式上线,Ink 的生态初具雏形。平台已开放 memecoin 发射工具 Inkypump,首个吉祥物代币 $ANITA 曾一度冲上 800 万美元市值,目前稳定在 400 万美元附近。虽然 $INK 的 TGE 尚未公布,但在 Base 等 L2 项目的成功案例刺激下,市场对 Ink 的潜力已有强烈预期。

参考 Base 链在生态活跃度、TVL、项目数量上的快速爬升以及 $VIRTUAL、$ZORA 等围绕其构建的生态代币表现,具备 Kraken 团队直接背书、且将自带流量和资源倾斜的 Ink,无疑具备成为下一条热门 L2 主线的可能。可以预期的是,未来一旦 $INK 启动流通并开放交易,势必将成为 CeFi 炒作叙事下的「正统」代表之一,尤其是在 Kraken 有意将其交易能力与链上场景深度绑定的背景下,Ink 不仅是一个 L2,更可能成为 Kraken 的 onchain 战略核心。对于想要提前卡位 Kraken IPO 与下一轮 L2 热点的投资者来说,Ink 与其生态标的值得重点关注。

总结

除了加密交易和 Layer 2 网络建设,Kraken 近来也在积极拓展更广泛的金融版图。2025 年,Kraken 以 15 亿美元重金收购美国领先的零售期货交易平台 Ninja Trader,拿下期货佣金商资格,正式挺进受 CFTC 监管的衍生品市场,打通 CeFi 与 TradFi 之间的关键通道。与此同时,Kraken 还推出支付应用 Krak,支持 300 多种加密与法币资产的即时报酬转账,未来更将扩展至借贷和信用卡服务,打造全方位加密支付体验。这一系列布局不仅为 Kraken 打造超级金融平台奠定基础,也被视为其酝酿多年的 IPO 计划的重要前奏。随着产品线扩张、营收增长和监管环境持续改善,Kraken 距离正式上市的步伐,正在日益加快。