原创 | Odaily星球日报(@OdailyChina)

作者|Azuma(@azuma_eth)

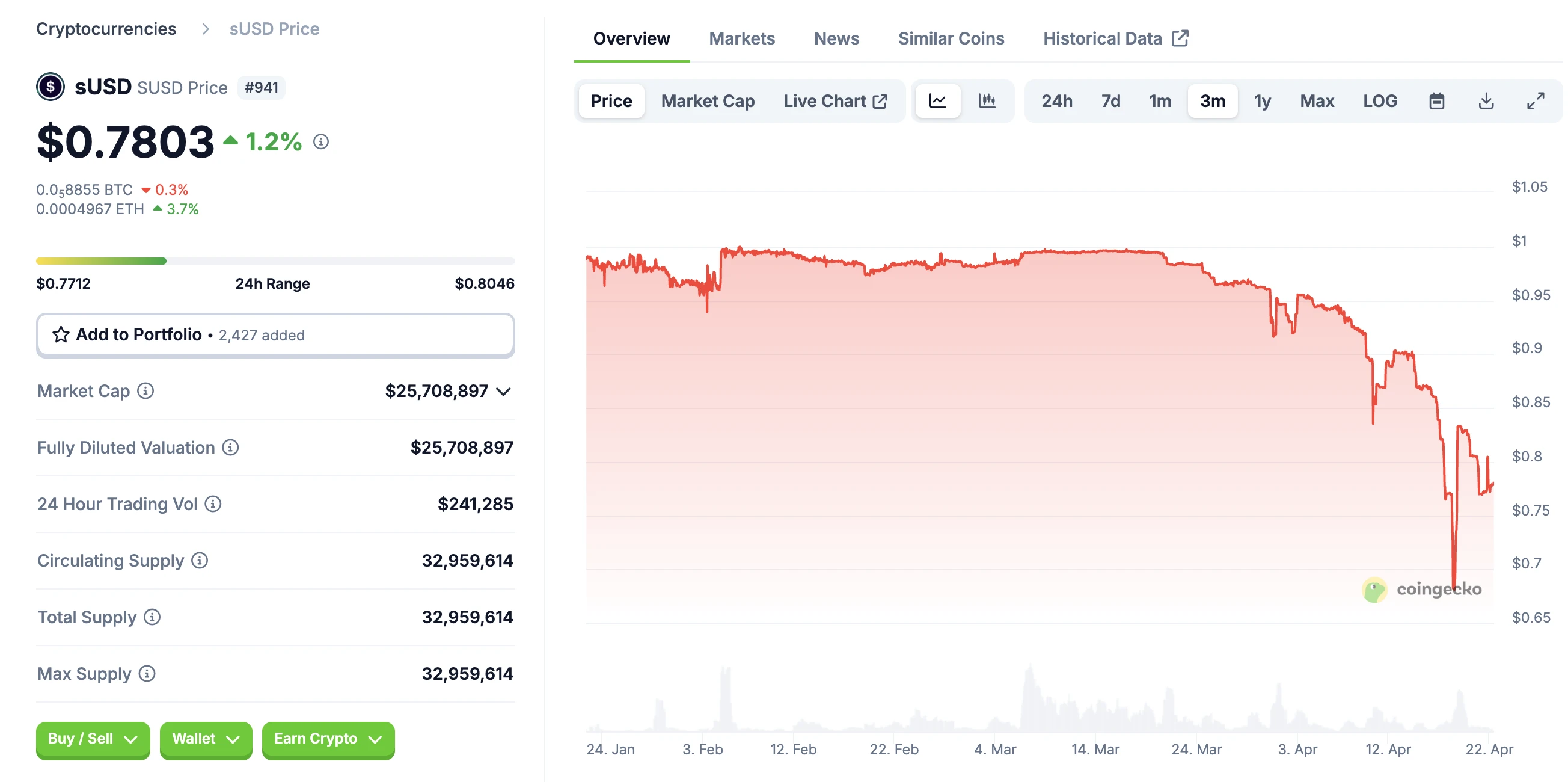

Synthetix 旗下稳定币 sUSD 近期因长时间脱锚而备受市场关注。

自 3 月 20 日初现脱锚迹象以来,sUSD 脱锚幅度持续放大,一度跌破 0.7 美元,截至发文暂报 0.78 美元。随着 Synthetix 陆续推出各项修复错误,sUSD 似乎已在低位有了一定企稳迹象,但能否回锚暂时仍是一个相当复杂的问题。

脱锚原因简析

sUSD 的脱锚需要从 Synthetix 的定位转换以及协议变更讲起。

Synthetix 的原始定位是合成资产(Synths)协议,允许用户通过超额抵押来铸造追踪不同资产(比如 BTC、ETH)表现的合成资产,而 sUSD 是如今仅存的仍具有较广泛效用的合成资产,因为 Synthetix 已逐渐弃用了原始的合成资产模型,转向永续合约 DEX。

此前,Synthetix 用户需抵押 SNX,以 750% 的抵押率铸造 sUSD —— 即每抵押 7.5 美元 SNX,可铸造 1 美元 sUSD。合成资产的铸造机制类似借贷市场,抵押物会被锁定,合成资产则成为了会产生债务的借款。sUSD 的债务以美元计价,但比特币等合成资产的债务则以比特币计价,随代币价格波动。SNX 抵押者需承担系统内相应比例的全局债务,这要求 Synthetix 需设计复杂的对冲策略以避免价格波动带来的风险,这种对冲需求、极高的抵押率及系统复杂性使得 SNX 抵押者兴趣缺缺,因此 Synthetix 近期借 SIP-420 提案推出了一个新模型。

2025 年初,旨在简化 sUSD 铸造流程、提升 sUSD 铸造效率 SIP-420 获治理通过。SIP-420 引入了共享债务池机制,计划在 12 个月内将 sUSD 的铸造方式从个人抵押模式逐步转向了集体资金池模式,SNX 质押者不再需要单独铸造 sUSD 并承担个人债务,而是可将资金委托给公共池,从而实现无清算、无个人债务的结构。与此同时,SIP-420 还将 sUSD 的抵押率将从 750% 降至 200% ,以显著提升系统资本效率。

然而,随着个人债务的免除,在 sUSD 价格偏离锚定值时,SNX 质押者不再有动机以低价回购 sUSD 偿还债务(此前个人抵押者可折价买入 sUSD 偿还债务以稳定价格),协议原有的自我锚定调节机制失效。这也是 sUSD 会出现脱锚的根本原因。

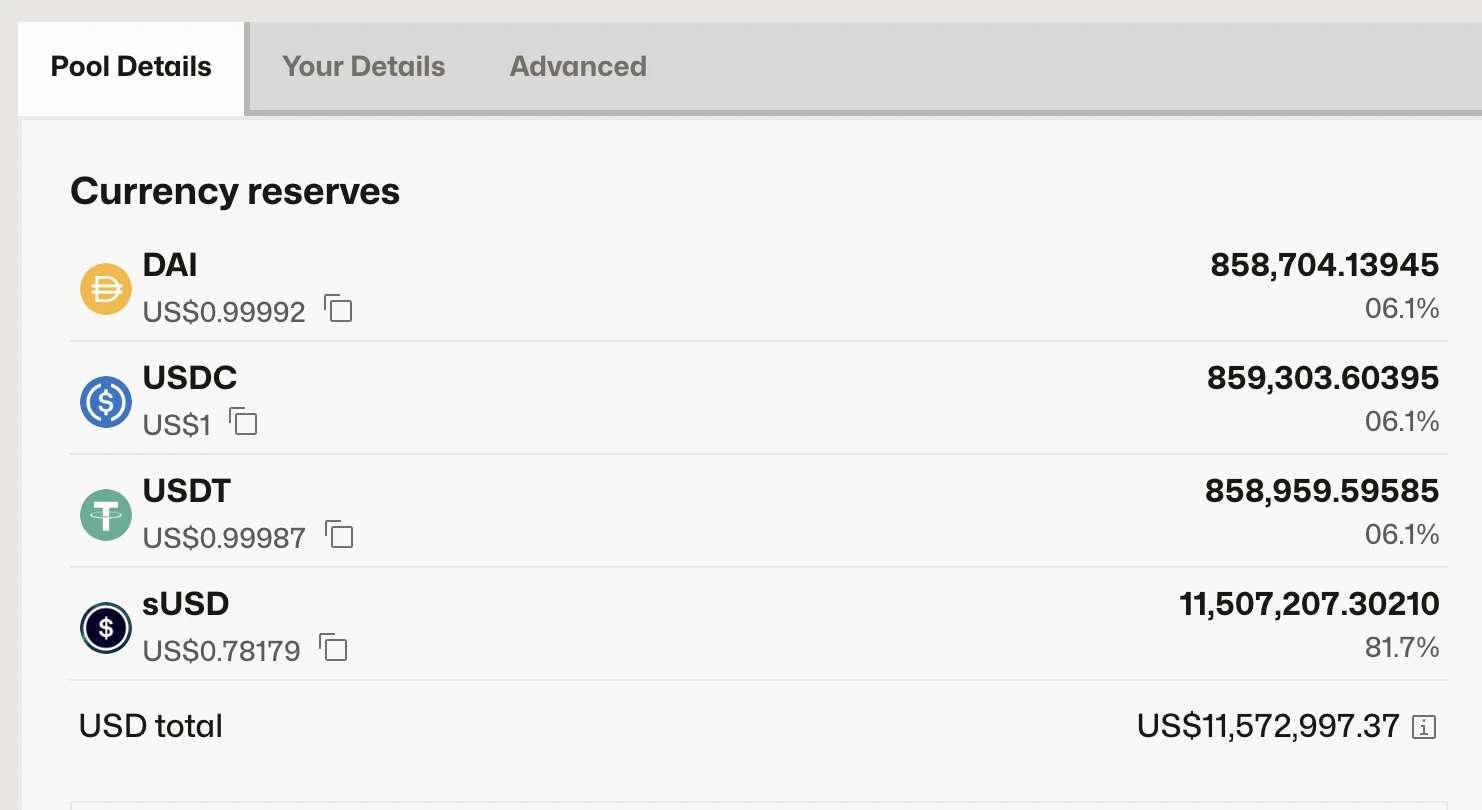

而脱锚情况之所以会逐渐加剧,是因为 sUSD 流动性并没有想象中那么充足。以 Curve 上最大的池子(sUSD/USDC/DAI/USDT)为例,总计约 1151 万美元的流动性中,sUSD 池内份额占比约 81.7% —— 这意味着实际的退出流动性已在脱锚过程被大量消耗。

Synthetix 的应对方案

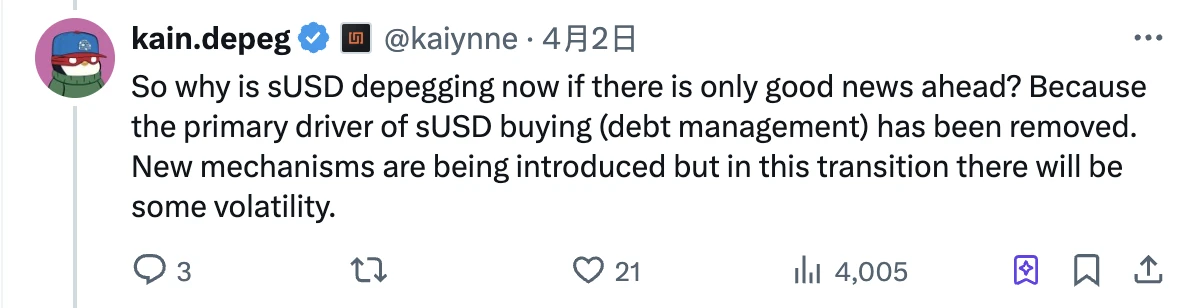

4 月 2 日,Synthetix 创始人 Kain 首次发文回应了 sUSD 的脱锚。Kain 提到,脱锚是因为购买 sUSD 的主要驱动因素(债务管理)已被消除,而新机制正在过渡中,因此出现了短暂脱锚。

前文提到过,SIP-420 希望在 12 个月内实现机制过渡,但社区显然不可能拿着一个脱锚稳定币坐等 12 个月。为此,Synthetix 近期已推出了多项额外措施,以尝试修复 sUSD 的价格。这些措施共有的关键词在于“激励”。

第一项措施是对 sUSD 的流动性提供激励,在最新激励措施上,Convex 之上质押 sUSD/sUSDe LP 的收益率已高达 49.18% ;

第二项措施是通过同一团队开发的另一项目 Infinex 提供对 sUSD 存款行为的激励,激励持续六周,每周对存款超过 1000 sUSD 的用户分发 16000 枚 OP 奖励;

第三项措施则是最新方案,即允许用户向 420 池质押 sUSD,质押后将锁仓一年,但会提供 500 万枚 SNX 作为激励。

显然,上述三项措施都是为了解决 Kain 所提到的“sUSD 购买需求不足”的问题。通过对一些泛锁仓行为提供额外激励,Synthetix 希望能够刺激 sUSD 的购买需求,并限制 sUSD 的潜在抛压,从而逐步推动该稳定币价格的回锚。

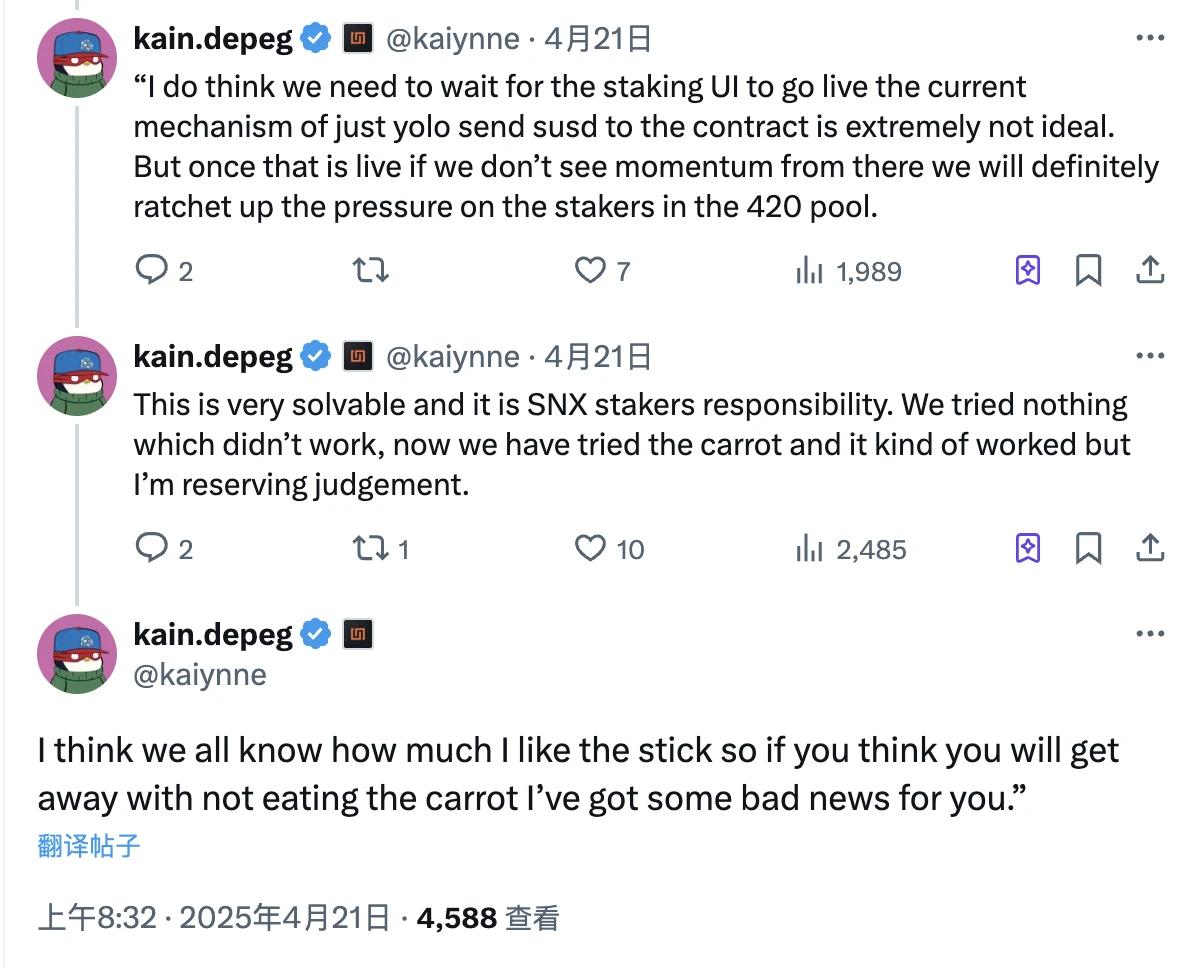

尤其是条件要求更严,激励力度更大的第三项措施,Kain 昨日亦曾发文提到了对该项措施的期望,并强调问题完全可解,团队将通过优化激励机制逐步解决脱锚问题。

值得一提的是,Kain 还提到如果 SNX 质押者不采用新推出的质押机制来帮助解决 sUSD(SUSD)脱锚问题,将会对他们施以“大棒” —— 或暗示在多项激励措施后,接下来将通过惩罚条件来对仍不“配合”修复行动的用户进行施压。

由于 Synthetix 暂未提供 sUSD 质押的用户界面,目前质押操作仍需团队手动处理,所以暂时无法获悉最终会有多少用户在激励之下参与 sUSD 质押,而这将在很大程度上影响 sUSD 的修复效果。

就目前的情况来看,很难判定 Synthetix 是否可以稳住局面。虽然市面上已有了一些抄底声音,但个人不建议当下去“火中取栗”,如果实现忍不住折价诱惑,则需密切关注 SNX 的价格表现 —— 以防止出现“价格下跌,抵押不足,折价加剧,恐慌抛售”的死亡螺旋。

另类套利机会

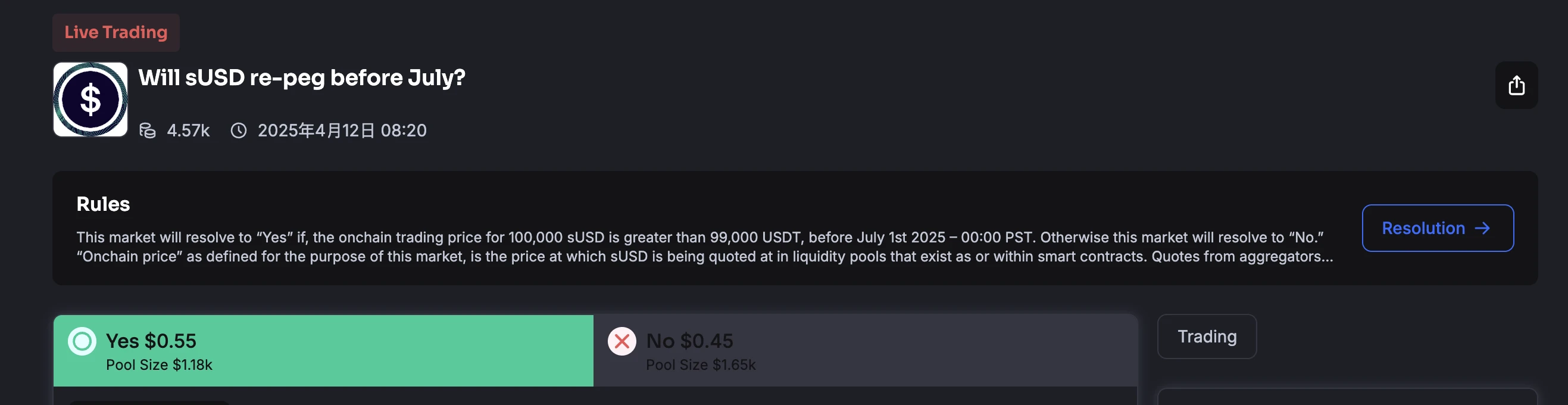

相较于押赌回锚,目前市场上似乎正在另一个套利机会 —— 预测市场。

预测市场 Truemarket 已上线了关于 sUSD 能否在七月之前回锚的预测池,当前 Yes 份额的报价为 0.55 美元,No 份额的报价为 0.45 美元。

由于 sUSD 当前报价 0.78 美元,回锚之后每单位 sUSD 的价格将修复至 1 美元,而每单位 Yes 份额也可从 0.55 美元变为 1 美元,这一价差的存在就提供了一定的套利空间。

然而,Truemarket 之上预测池的深度相对较小,无法承接较大规模的交易,所以该策略的实际操作空间并不大 —— 建议后续关注包括 Polymarket 等其他更主流的预测市场是否会开通类似预测池,并寻找潜在套利机会。