作者:慢雾安全团队

概览

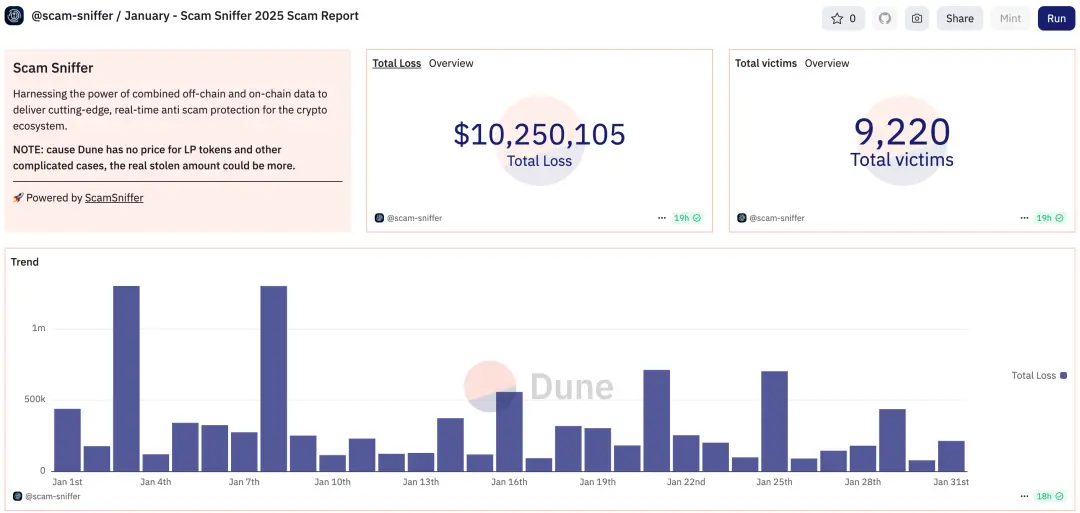

2025 年 1 月,Web3 安全事件总损失约 9,819 万美元。其中,据慢雾区块链被黑档案库 (https://hacked.slowmist.io) 统计,共发生 40 起被黑事件,导致损失约 8,794 万美元,有 147 万美元得到返还,事件原因涉及合约漏洞、账号被黑和私钥泄露等。此外,据 Web3 反诈骗平台 Scam Sniffer 统计,本月有 9,220 名钓鱼事件受害者,损失规模达 1,025 万美元。

(https://dune.com/scam-sniffer/january-scam-sniffer-2025-scam-report)

安全大事件

Phemex

2025 年 1 月 23 日,总部位于新加坡的加密货币交易所 Phemex 的热钱包被攻击,导致约 7 千万美元的损失。Phemex CEO Federico Variola 在 X 平台表示:「大家好,我们正在调查有关某个热钱包的报告,请放心,冷钱包依然安全,任何人都可以查验。我们会尽快带来更多更新。」

(https://x.com/MistTrack_io/status/1882412516518789500)

NoOnes

2025 年 1 月 1 日,P2P 交易平台 NoOnes 遭攻击,其热钱包在 Ethereum、Tron、Solana 和 BSC 上出现了数百笔可疑转出交易,损失约 720 万美元。首席执行官 Ray Youssef 解释说,此次事件的原因是其 Solana 桥遭利用。

(https://x.com/ray_noOnes/status/1882744360812306885)

AdsPower

2025 年 1 月 24 日,AdsPower 的安全团队发现了一起入侵事件,黑客散播了恶意代码导致部分第三方浏览器插件遭到篡改,超 470 万美金被盗,慢雾安全团队已介入分析。如果用户有使用 AdsPower,且在 1 月 21 日 18:00 至 1 月 24 日 18:00 (UTC+8) 安装过扩展钱包或手动更新过扩展钱包,那么用户 AdsPower 上的扩展钱包可能是带后门的版本(助记词 / 私钥存在被盗风险),请尽快转移相关钱包的资产。

(https://x.com/AdsPowerBrowser/status/1882983731419570220)

Moby

2025 年 1 月 8 日,攻击者控制了用于授权 Moby 核心合约升级的私钥,导致协议遭到破坏。这次攻击导致 sOLP 和 mOLP 流动性池中的 3.77 wBTC、207.76 wETH 和 1,500,351.5 USDC 曝露于风险之中。Moby 在 Seal911 团队的协助下已追回了约 147 万枚 USDC。

(https://medium.com/moby-trade/moby-post-mortem-report-growth-plan-504ad5b0dd35)

Orange Finance

2025 年 1 月 8 日,基于 Arbitrum 的流动性管理项目 Orange Finance 由于多签配置错误被利用,导致价值 83 万美元的资产被盗。攻击者获取了每个金库的所有权,修改了它们的实现,并提取了存入的资产以及过度授权的资金。总损失中约 94%(约 78 万美元)来源于存入资产,其余 6%(约 4.7 万美元)则是由于过度授权造成的。

(https://mirror.xyz/0x6FA2aF9a4d6fFe654361F713780963C10412e7c3/gN17YMrLhKKg9YT9a391U74pWr9IhqBUDWUqDyDamjE)

特征分析及安全建议

近期账号被盗事件频发,据慢雾区块链被黑档案库统计,一月发生了 21 起账号被盗事件,约占总事件数的一半,其中政治人物或政治内容相关的账号被盗情况尤为突出。黑客或恶意行为者使用社交媒体推广 Meme 币,利用用户们的 FOMO 情绪吸引资金,然后卷款跑路,例如,X 账号 @TrumpDailyPosts 发布了 4 条推广 Meme 币的推文,在几分钟内迅速删除,卷走了约 125 万美元。因此,建议用户提高警惕,购买代币前核实信息来源,不要轻信社交媒体上的突然公告,尤其是涉及政治人物、知名机构或明星的 Meme 币,避免落入骗局。

此外,慢雾安全团队注意到,近期收到的众多受害者的求助信息均与 Telegram 上的「假 Safeguard」骗局有关,相关作恶手法和应对措施见新型手法|Telegram 假 Safeguard 骗局。