原创 | Odaily星球日报(@OdailyChina)

作者|Azuma(@azuma_eth)

备受关注的 Pudgy Penguins 代币(PENGU)将于今晚正式上线。

Pudgy Penguins 首席执行官 Luca Netz 今晨于 X 发文表示,美东时间明日 8: 00 (北京时间今晚 21: 00),符合条件的参与者(包括 Pudgy Penguins、Lil Pudgys、Rogs 和 SBTs 持有者等等)可以开始申领 PENGU。申领周期共 88 天,所有未领取供应将在第 88 天后永久锁定/销毁。

Pudgy Toys 的买家也将被纳入空投范围,但由于 Pudgy Toys / Pudgy World 建立在 Abstract 上。当 Abstract 主网上线时,通过 LayerZero 申领 PENGU 的桥接功能也将上线,之后 Pudgy Toys 买家也将能够申领他们的 PENGU,更多细节将于明年 1 月 Abstract 主网上线之际公布。

PENGU 代币经济模型

PENGU 总供应量为 88, 888, 888, 888 枚,将基于 Solana 网络发行,代币合约地址为 2 zMMhcVQEXDtdE 6 vsFS 7 S 7 D5 oUodfJHE 8 vd 1 gnBouauv。PENGU 的流通供应量将为 62, 415, 951, 646 枚,约占总供应量的 70.22% 。

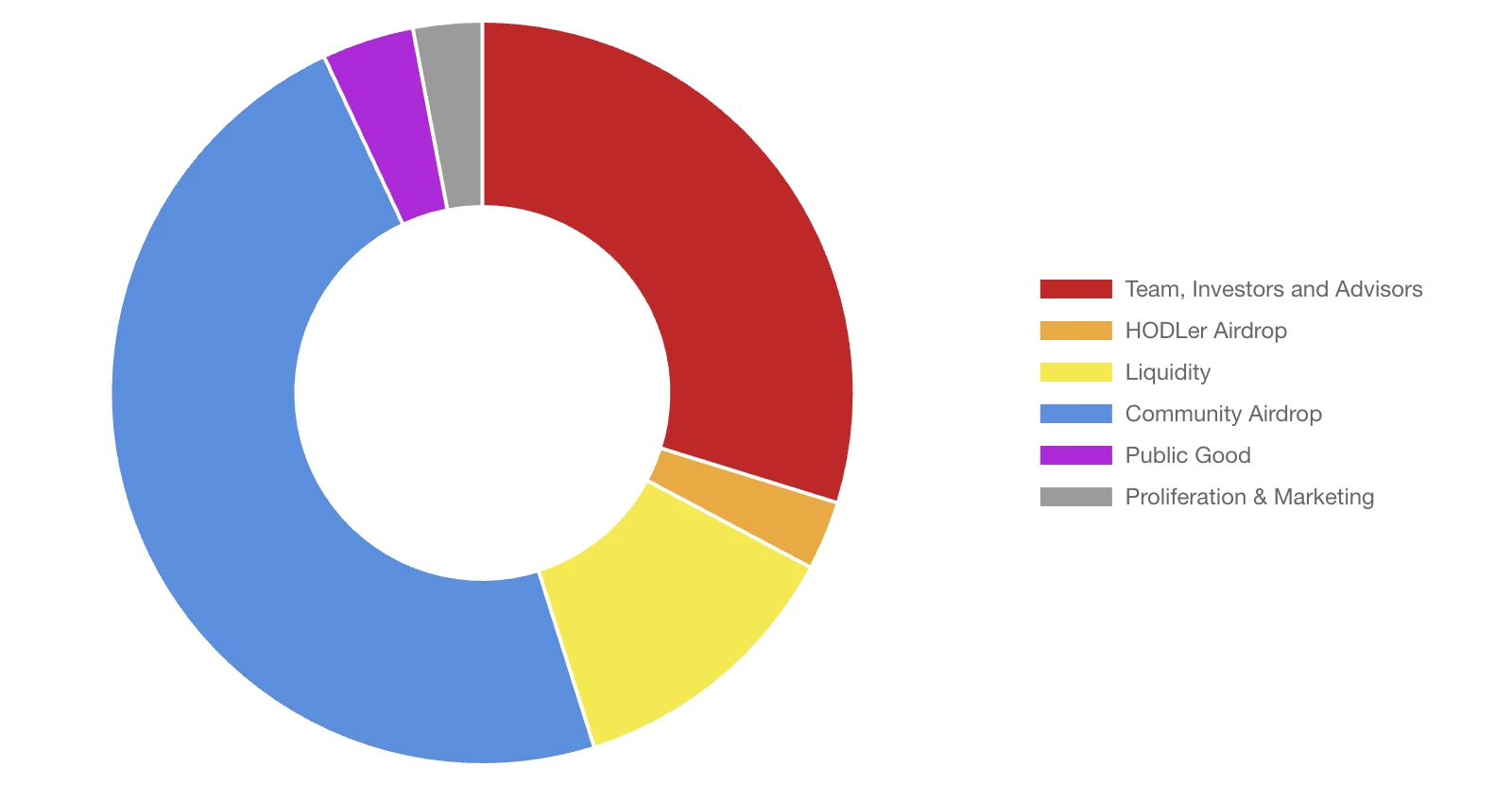

PENGU 的具体分配方案如下:

- 29.78% 的 PENGU 将分配给团队、投资人及顾问,该部分代币将锁仓 1 年,之后分 3 年时间线性释放;

- 47.87% 的 PENGU 将用于社区空投;

- 12.35% 的 PENGU 将用于构建初始流动性;

- 4% 的 PENGU 将用于支持公共事务发展;

- 3% 的 PENGU 将用于营销及扩展。

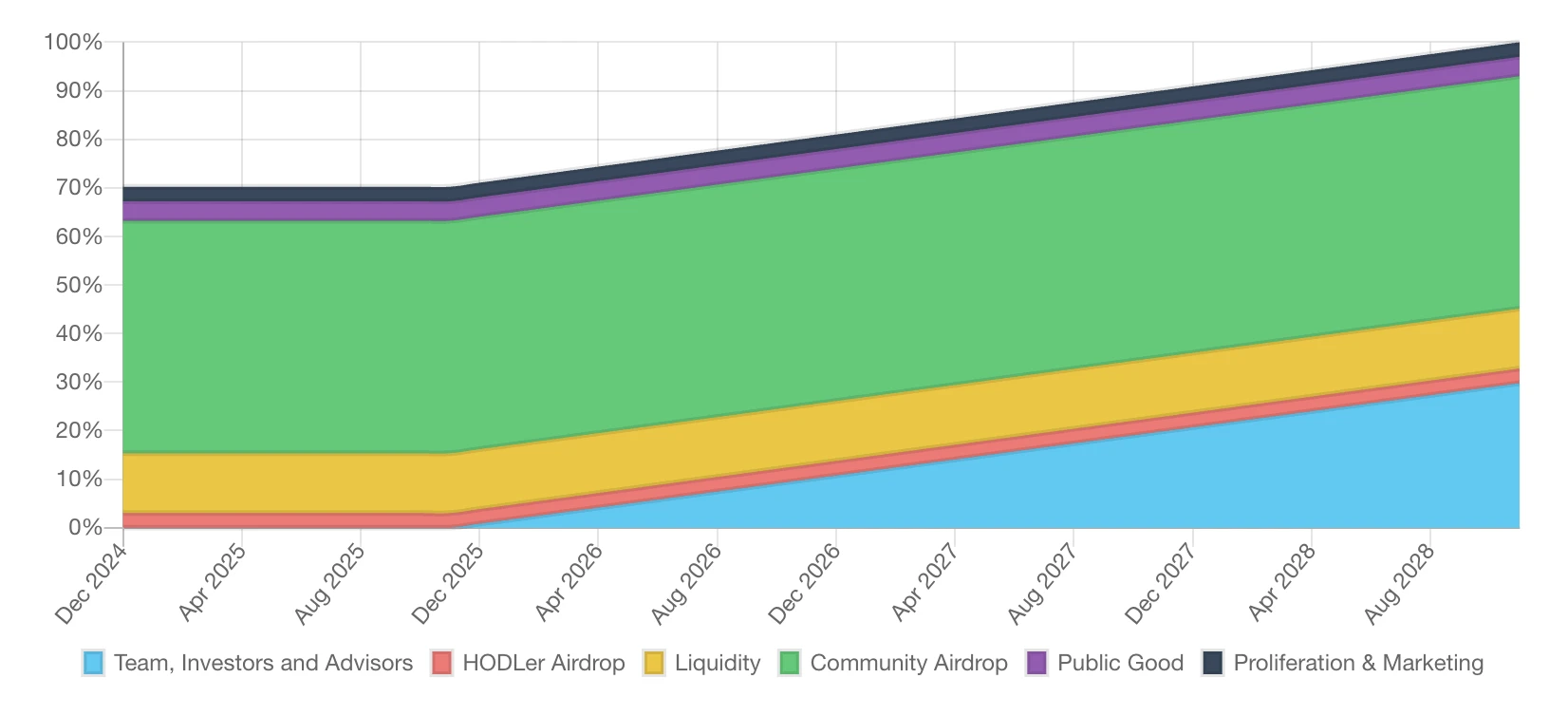

如下图所示,除了团队、投资人及顾问份额之外,其他部分的 PENGU 分配均将于开盘之时解锁。

PENGU 估值预期

当前,多个 pre-launch 交易市场均已开放 PENGU 的盘前交易。截至北京时间 13: 00 左右,各平台估值报价如下。

- Aevo 上 PENGU 暂报 0.04128 美元,对应流通市值(MC)约 25.76 亿美元,对应全流通估值(FDV)约 36.69 亿美元;

- whales.market 上 PENGU 暂报 0.0439 美元,对应流通市值(MC)约 27.4 亿美元,对应全流通估值(FDV)约 39 亿美元;

如果用 APE、MOCA 等 NFT 系代币,以及 PEPE、WIF 等动物系 meme 代币作为参考标的,PENGU 的估值预期如下。

小结

鉴于当前市场的火热情绪,再加之 Pudgy Penguins 在 NFT 细分赛道内日渐稳固的龙头位置,预期 PENGU 开盘之后将会吸引极大流量,但考虑到 PENGU 开盘之初流通比例较大,不可避免地会出现一定的空投获利抛压,各位投资者需结合个人预期理性操作,DYOR。