原文作者:1mpal

原文编译:Luffy,Foresight News

我热爱 Web3 游戏,很大一部分资金都投资在游戏 NFT 和代币上。不过,我对单纯的游戏代币非常不看好。

市场需要正常化。目前,我对那些自 TGE 以来就完全失去增长势头的游戏项目没有任何好感。

如果我是一名交易员,我会认为那些交易 Memecoin 或押注蓬勃发展的人工智能领域的人是聪明人。目前没有理由在游戏代币上押注巨额筹码,市场的实际情况也恰恰如此。造成这种情况的原因有很多,但主要原因是游戏代币缺乏关键因素来支撑被高估的市场估值。

1. 游戏代币被高估

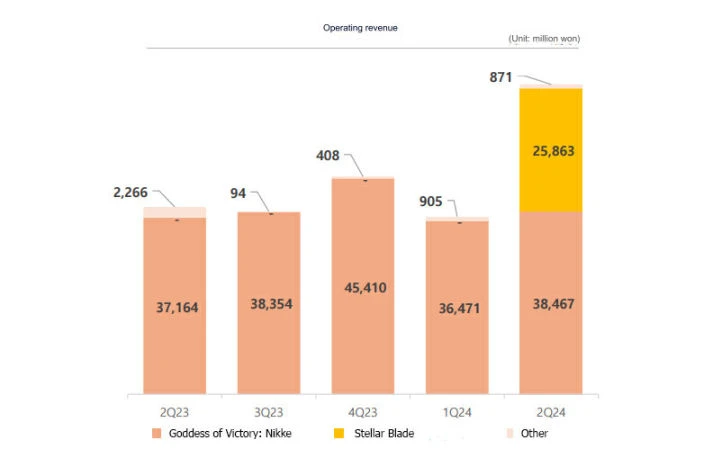

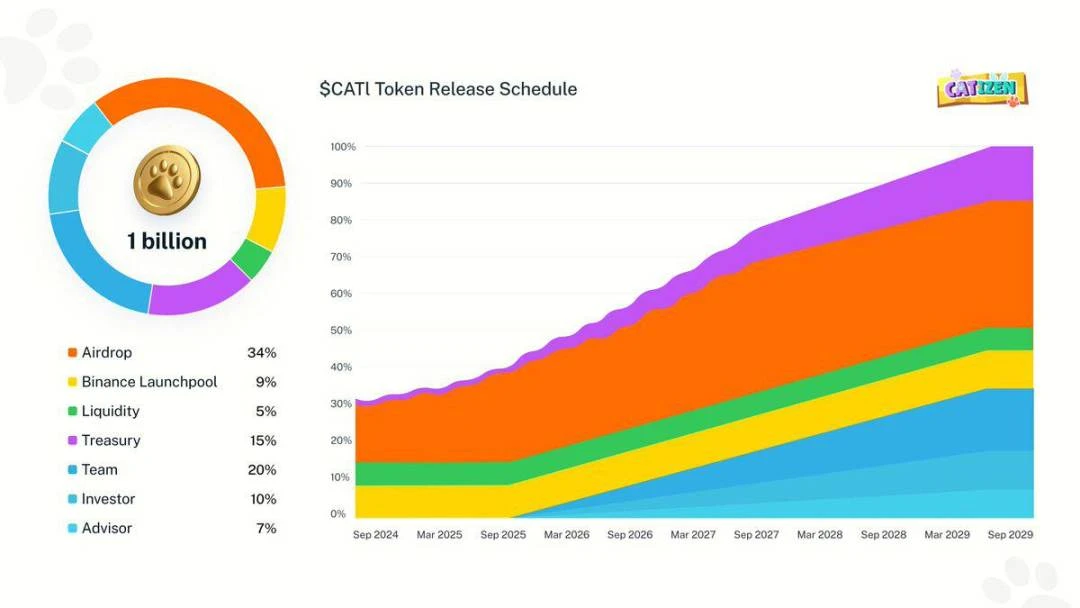

很少有 Web3 游戏能够匹配其市场估值。即使按流通市值而不是 FDV 计算,Web3 游戏也被高估了。例如,CATIZEN 是近期表现最突出的游戏之一,目前市值约为 2 亿美元,假设其年收入为 2000 万美元。

为了简单理解,你可以拿代币与股票对比,以评估它们的估值。韩国游戏公司 Shift Up 最近上市,市值约为 24 亿美元, 2023 年营收为 1.4 亿美元。市场认为它被高估,因为它具有巨大的未来潜力。

Nexon 的市值为 163 亿美元,年收入为 30 亿美元。Krafton 的市值为 123 亿美元,年收入为 15 亿美元。Take-Two Interactive 的市值为 263 亿美元,年收入为 53 亿美元。对于大多数大型游戏公司来说,年利润通常占其市值的 10-20% 。

代币经济学建立在游戏会无条件增长的前提下

还是以 CATIZEN 为例,从市值来看,这似乎是一个非常健康的项目,但问题在于解锁机制,主流游戏公司需要融资才能扩大规模,但 Web3 游戏项目的代币是自动解锁的。

事实上,单纯的游戏项目如果没有基础设施,是不可能实现增长的。除非有特殊情况,大多数游戏在发布时的用户数量最高,然后呈缓慢下降趋势,这是很常见的情况。换句话说,Web3 游戏自我增值的想法是违背市场规律的。

2. Memecoin 比游戏代币更有吸引力

在交易中发现低市值宝石的能力是一种宝贵的才能,最简单可靠的信号就是交易量。交易量不大意味着市场不太感兴趣,自然会导致上涨势头疲软。谁愿意交易自上市以来一直在下跌的行业?

如果您是一位赌徒,流动性再次进入加密货币时,您会押注哪种代币?

对比币安上 NEIRO、CATI、HMSTR 的走势图,我们可以看出明显的区别。尽管 CATI 在游戏收入方面明显优于传统 Web3 游戏,在外部社交媒体收入方面也明显优于 HMSTR,但市场表现却并不理想。在币安上,NEIRO 和 CATI 的交易量相差约 10 倍。

考虑到当前的市场情绪和交易所上市的意愿,这是典型的游戏代币进行 TGE 的最糟糕时机之一。游戏不可避免地由风险投资驱动,无法在当前市场中竞争的项目会迅速通过 NFT 销售、节点销售和 TGE,然后退出。因此,交易和持有 memecoin 比游戏代币更好。

我认为决定股票价格的三个原则是:对公司未来价值的预期、公司的业绩记录以及市场供需波动。目前,游戏代币没有业绩记录,供应超过需求,除非它们有特殊的营销手段,否则它们作为纯游戏的未来竞争力是不可靠的。

虽然将游戏代币与股票进行比较可能并不完全合适,但也有参考价值。关键在于哪些项目拥有推动市场叙事的关键。如果一家公司的未来价值仅仅取决于其游戏,那么它将无法生存。它需要基础设施,它需要技术推动力。

或者,从一开始就解锁全部代币并让市场决定价格。

最后的想法

我相信 2025 年第一季度加密货币将迎来显著的上涨。我和很多人一样喜欢 Web3 游戏,但是,我觉得纯 Web3 游戏代币的 FDV 需要降低。当然,如果你有基础设施或技术护城河(比如游戏链),你就可以获得更高的估值。但现在,有很多游戏虽然估值很高,但只服务于游戏本身。

这可能是游戏项目最糟糕的时候,或者可以将其视为一个常态化过程。今年我参加了几轮游戏项目的 KOL 融资,大多数都是亏损。VC 的加入让 FDV 越来越高,代币锁定结构违背了平均法则。

然而,一些游戏项目将在这一过程中生存下来,我们希望押注那些能够根据收入扩展到平台和基础设施的项目。请记住,推动市场的是一两个巨头,而我们处于交易者之前的阵地,可以优先挑选主角。然而,我们的弱点可能是过于痴迷于游戏的未来。即使我们热爱游戏,也需要尝试将其商业化。