原创|Odaily星球日报(@OdailyChina)

作者|Wenser(@wenser2010 )

8 月 12 日,一篇据说由“耶鲁大学教授”发表的论文提出“ServerFi”概念,称其“强调通过资产合成实现私有化,以及一个专注于为高留存玩家提供持续奖励的模型”,而且“研究结果表明,ServerFi 在保持玩家参与度和确保游戏生态系统的长期可行性方面特别有效,为未来的区块链游戏发展提供了有希望的方向。”尽管后来经0xUClub 创始人 Jack考证,此文大概率是假借耶鲁大学之名发表的“套皮内容”,但对 GameFi 领域有着或多或少期待的用户还是对此提出疑问:ServerFi 会是后续的 GameFi 游戏的“救命稻草”吗?

Odaily星球日报将于本文简要梳理不同观点,并对此问题予以分析解答。

市场观点:褒贬不一,整体表示看好

在 ServerFi 概念出现后,市场上掀起了一轮不小的讨论,概念详情可以参考《耶鲁大学:ServerFi,游戏与玩家之间的新型共生关系》一文。

整体而言,中文区 KOL 及从业者的正面观点居多,甚至Web3 MMORPG 游戏 MetaCene 直接将 X 平台账号后缀改为“ServerFi”,并发文表示:“很高兴推出世界首个 ServerFi 产品”,并直言“让服务器属于你自己(指玩家)”。以下是部分代表性观点:

Folius Ventures 投资人、Myshell 团队成员 Aiko 表示,“在我看来,ServerFi 特点包括:

- 不同服务器之间的贸易和征税

- 服务器文化各异:高度竞争与和平

- 新的生产和消费曲线

- 解决单一环境中由过度开发引起的资源枯竭和死亡螺旋

- 为服务器管理者(分发商,代理等)提供荣誉和收入

如果一个经济系统不可持续,那是因为它不够复杂或多样化。就像热带雨林一样。当它拥有广阔的环境(或地图)和多样的物种时,自然会趋向于平衡。”

加密研究员、华语 KOL Haotian 发文表示,“ServerFi 的新运行框架包括 3 个特性: 1)侧重长期参与和价值创造;2)降低 Ponzi 结构性风险并减少投机行为;3)由web3的去中心化社区精神驱动。”

加密 KOL Dr.Jinglee 对此话题表示,“作为学术文章,对其文章所使用的‘熵增’理论,以及在模拟实验的方式进行论证的过程存在一些疑问,包括玩家如何对服务器的”贡献”的定义等也有不清楚的地方。”

AC Capital 合伙人、Open-Rug 主理人 CryptoV(加密韦陀)表示,“这一模式跟 play to earn 没有本质的区别,只是说把‘参与游戏会赚钱’这个假设变成了‘游戏本身能搞到钱’,本质都是(给玩家分润收益的)分红盘。”

Eureka Guild 联创、GameFi 领域研究员 Leslie 认为,“ServerFi 确实提出了一些有用的逻辑,但本身不应该是被 fomo 的概念。Web3游戏要成功需满足游戏性、博弈性、经济适配等方面的条件。如何积蓄核心玩家以及新老玩家的平衡是一款游戏需要着重考虑的问题。”

看得出来,对于 ServerFi 的落地而言,目前大家只能更多从“服务器所有权”、“游戏项目与玩家之间的利益分配”等角度去谈论,而很难深入讨论“经济模型”、“游戏生命周期”、“具体资源交换”等话题,包括 ServerFi 原文也更加偏向于数学拟合推演,而非实际项目对比。

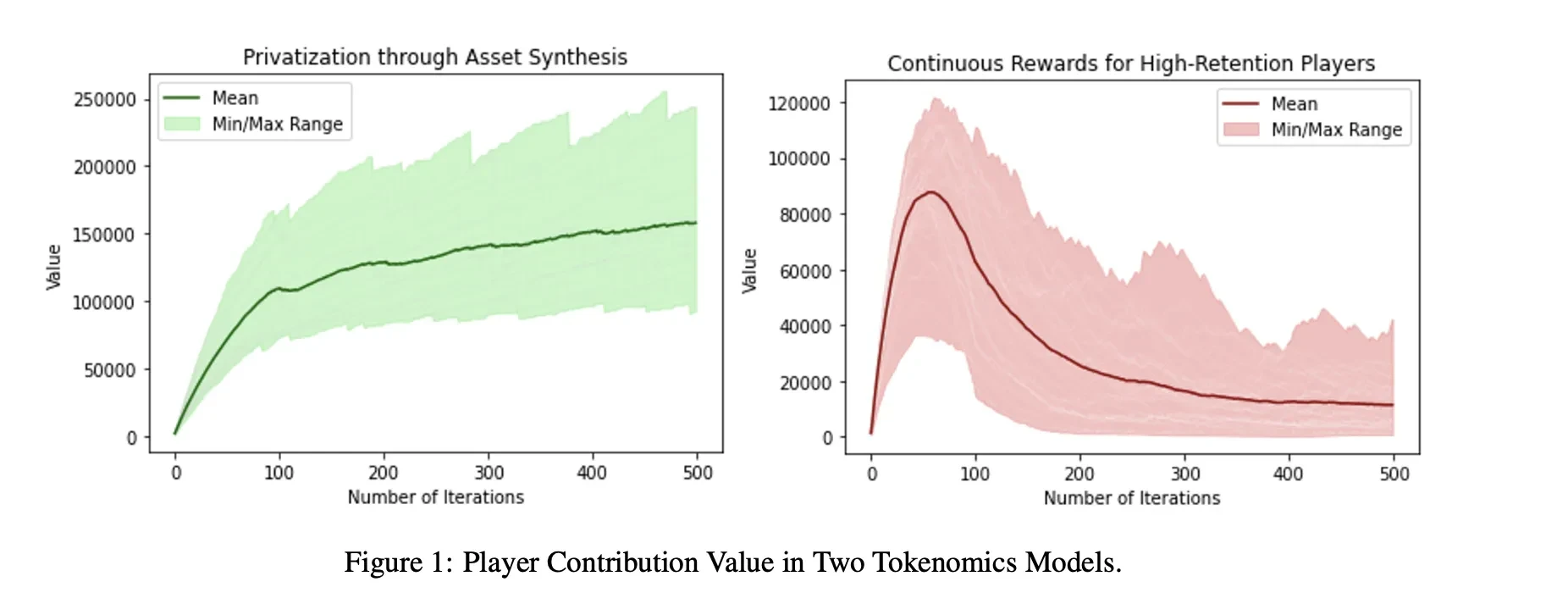

2 种经济模型中的玩家贡献价值数据

ServerFi:缔结一种“想象中的利益共同体”

细究下来,ServerFi 的核心命题其实主要在于以下 3 个方面:

3 大核心命题:游戏人数、服务器价值、贡献回报比

首先,游戏人数是 ServerFi 成立的前提。因为如果游戏人数无法满足一定量级的话,ServerFi 的条件仍然不成立:没有足够的玩家,没有相对而言的“老玩家”和“新玩家”,没有“游戏内资产”的创造链路。而这,恰恰是当前 GameFi 领域游戏的一大“难关”——游戏性不足,游戏玩家数量相比而言屈指可数。

其次,服务器价值是 ServerFi 运转的核心。当游戏玩家分层体系逐步建立,游戏内经济体系逐渐完善后,因为内部货币、道具等“资产”的交易流通,这个服务器才具备了对应的“可量化价值”——通常是可以与法币体系挂钩的。换言之,ServerFi 运转的核心在于一个通过积累产生价值的“ Server ”,这也是很多人现在仍然在传奇私服的搭建和玩耍上面大把撒钱的原因——大 R 玩家喜欢一刀 999 的爽感,私服厂商为其提供对应的服务场景与服务体验;如果这个服务器的“价值”无法积累或者货币化,那么 ServerFi 同样无法运转。

最后,贡献回报比是 ServerFi 可调的参数。如果说传统 GameFi 游戏如 Axie Infinity、STEPN 等中可以调整的“数值参数”是道具的生产速度、代币的产出速率,那么 ServerFi 可以说是实现了“参数的模糊化和升维化”:游戏玩家获得游戏内资产并合成仅仅是做出贡献的第一步,获得回报的多少和快慢更多取决于“游戏服务器的运行、运营”与“服务器之间的交易”。以往的 GameFi 游戏层次仅仅局限于“玩家 PVP”、“玩家系统 PVE”的维度,游戏项目方以“上帝视角”行使着“上帝”的角色权柄,而现在,玩家、服务器、项目方需要缔结为一个“利益共同体”,由此激发不同角色主体之间对“服务器”这一核心介质的投入、维护和扩张发展的积极性。

ServerFi:设想中的另类“去旁氏解法”

基于以上核心命题,我们可以继续推导 ServerFi 类型的 GameFi 游戏下一步需要“以清养旁”或者说“以清抑旁”的操作了:

游戏的情绪价值、娱乐价值是 ServerFi 模式无法解决而必须依靠 GameFi 游戏自身产品提供,可以是“道具收藏”、“卡片抽奖”、“社交排名”、“现实反馈”,少一点没关系,但是不能没有,否则没人“入局”。

服务器的归属权、游戏内资产合成条件以及二者之间的明确是 ServerFi 模式设计之初需要分阶段考虑的问题,这之中就涉及到了“项目方、大 R 玩家、小 R 玩家、免费玩家”之间的利益分配,以及“游戏内资产和游戏外服务器的经济模型设计”。

引入类似多签协议的“罚没机制”或“惩罚机制”,确保“贡献回报比”的调参行为能够处于动态平衡或者各方无异议的状态。这一点,恰恰是当今 GameFi 游戏缺少或者无能为力的一点,毕竟成本大头在项目方身上,为了实现“快速收割”和“短期获利”,无论成功程度如何,项目方都很难抵御诱惑,把回报周期拉长;与之相对,玩家也很难做到在投入时间、精力、资金等成本后做到“长期主义”。

所以,ServerFi 的真正落地,很难是一朝一夕就可以完成的。

小结:扩展 Server 范围或将改变“游戏规则”

无数 GameFi 项目方和玩家都对梦幻西游推崇备至,皆因其在特定的时代背景和不同的游戏人群之间找到了一条“晃悠悠但稳住了”的“钢丝绳走法”,由此实现了游戏性、经济性的双重适配,但类似案例很难成为一种模式。

与此相比, ServerFi 不失为一种“新的视角”,尤其是在将不同的“服务器类型”予以扩展之后。以下图示尽管与 GameFi 游戏行业关系不大,但是也有可资借鉴的部分,那就是,如果将现有的“游戏服务器”概念予以泛在化,这样不同服务器之间也可被视为“玩家帮派”,由此可以实现更大范围内的流动性交换,进而为 GameFi 游戏的建设不断升维。

毕竟,换句话说,整个地球不也是一台巨大的“服务器”吗?