过去 24 小时,加密货币市场集中关注两个焦点,一是 IV 为什么垮了,二是为什么涨了?我们可以顺着时间线找到一些线索。

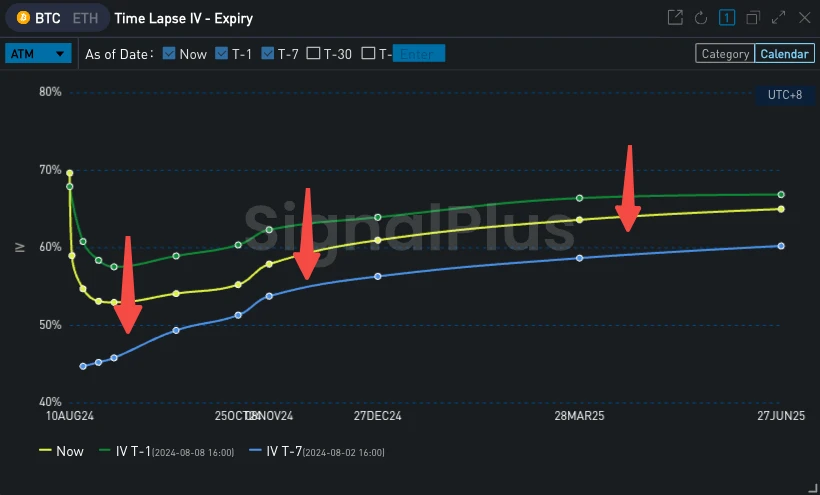

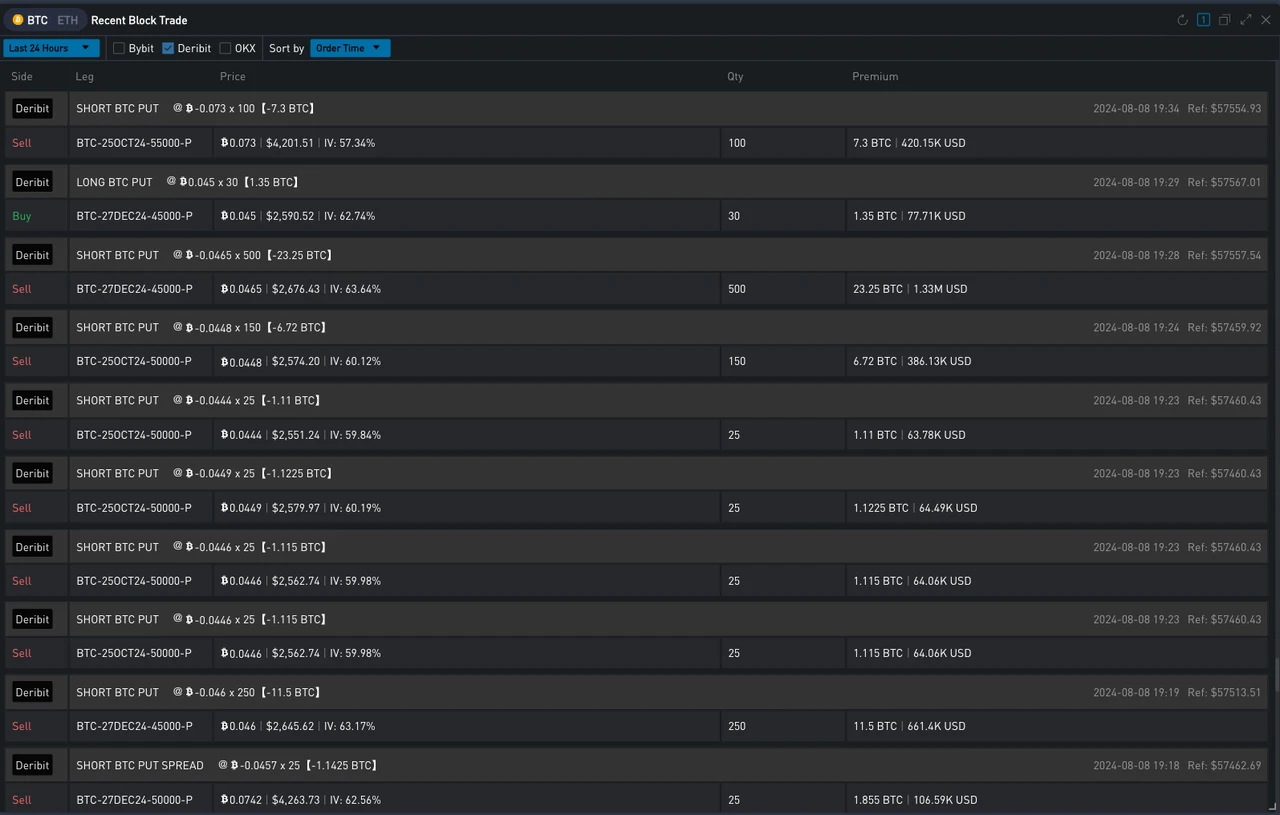

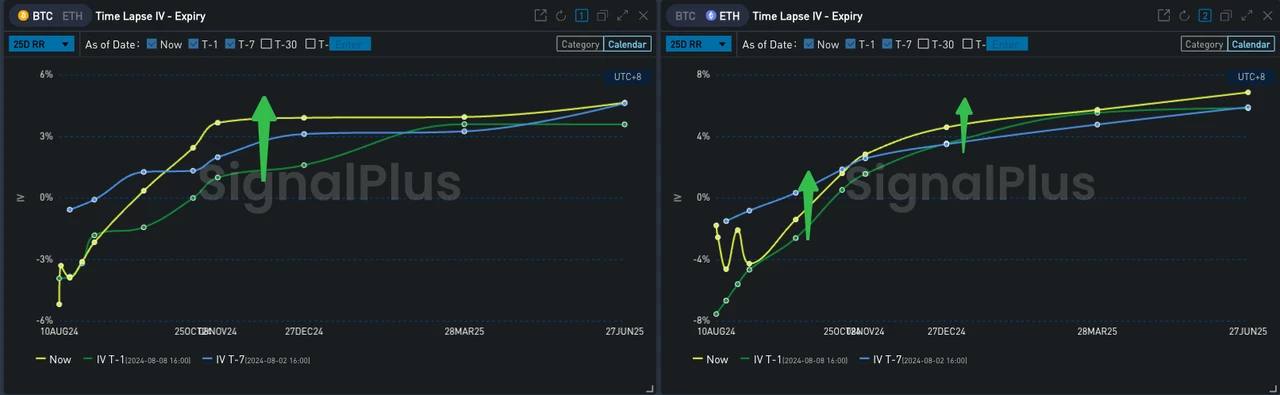

事情开始于 8 月 8 日晚上 7: 30 左右。在此之前,昨日 BTC 的画门行情将市场整体隐含波动率逐步推至高点,而正当价格恢复平静在 57500 附近小幅整盘时,Deribit 市场上突然出现大量 Dec 和 Oct 的卖出看跌期权成交,年底的 IV 短时间内被砸低 3% Vol,带动整条 Vol Curve 大幅向下平移。

Source: SignalPlus Time Lapse IV / Historical IV

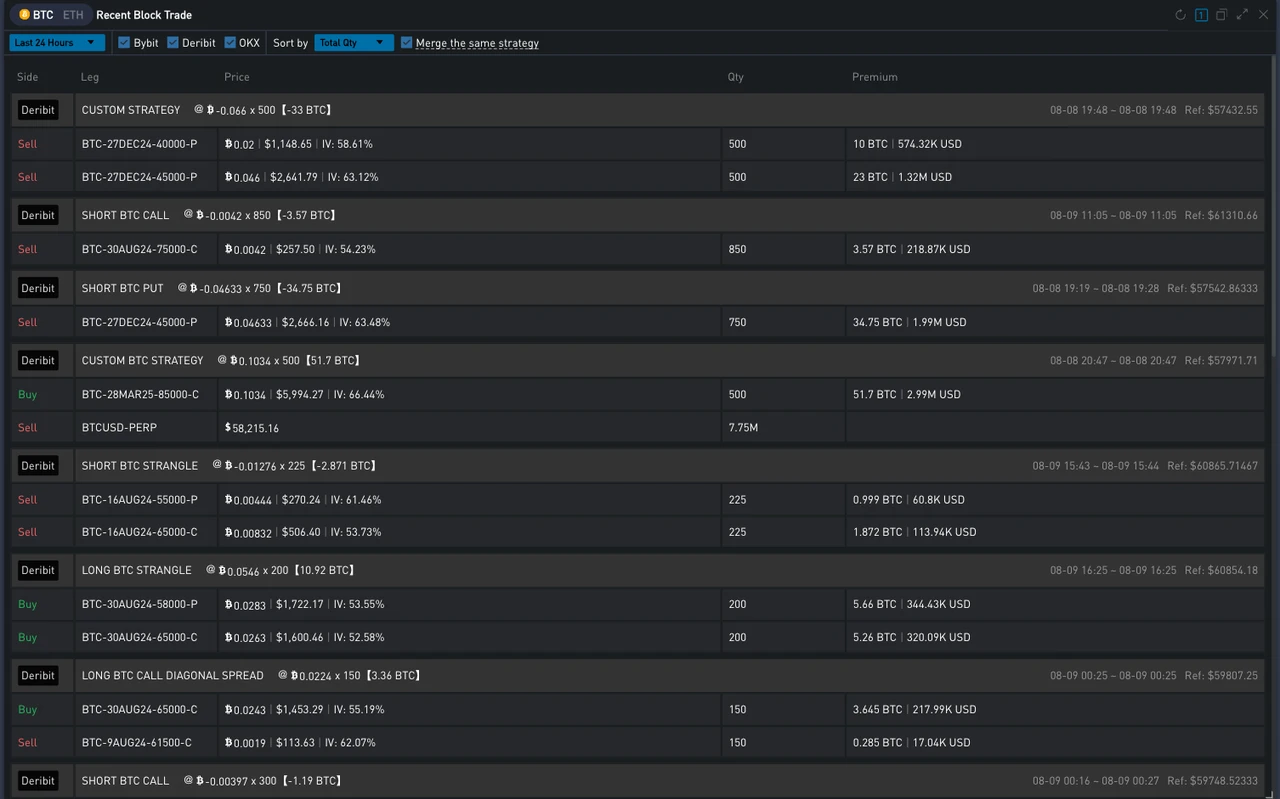

Source: SignalPlus Trade Volume by Expiry; Recent Block Trade

Source: Deribit (截至 9 AUG 16: 00 UTC+ 8)

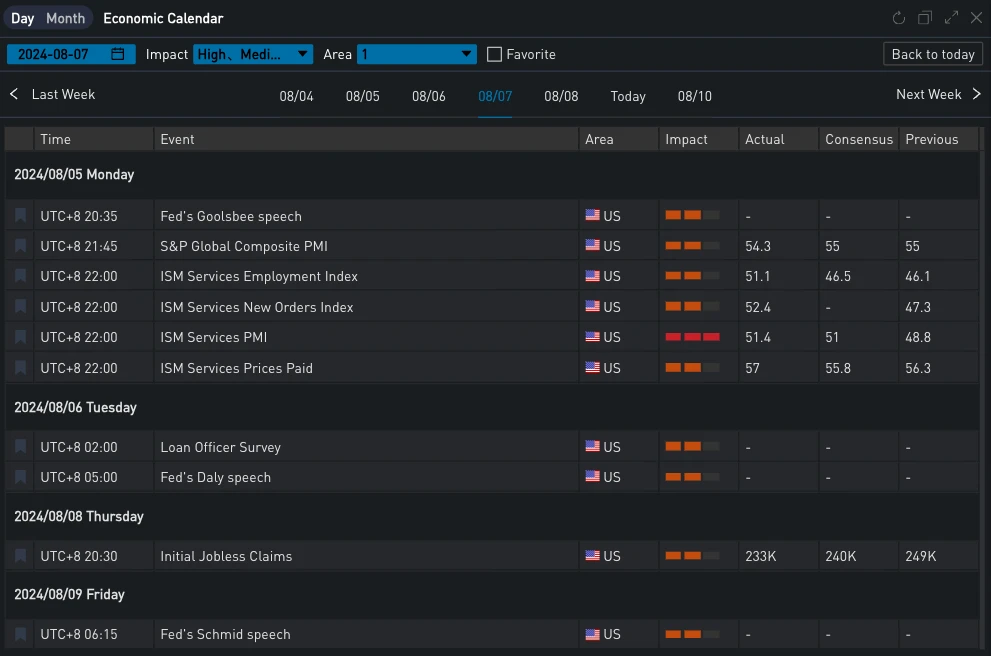

而后来到晚上 08: 30 ,美国公布了新一轮的初请失业金人数,数据下降幅度接近一年来最大,缓解了人们对全球最大经济体经济放缓的担忧,美股强劲反弹(道指/标普/纳指分别收涨 1.76% /2.3% /2.87% ),美债收益率走高。作为与美指高度正相关的风险资产,BTC 价格也受到提振,从 57500 一路上行突破 60000 美元,并一度挑战 62000 这道关键支撑位。

但说回宏观这件事,这周对全球投资者来说都是相当艰难,SoFi 的 Liz Young Thomas 对此评论:“起伏不定,四处皆是。我们了解到市场对美国经济数据的敏感程度,日元套利交易影响的广泛性,以及投资者对降息作为解决一切问题的习惯。”

也正是在如此波动的行情中,市场的焦虑和不安逐渐累积,投资者的情绪一直处于低迷的状态,才让这份通常没被人放在“High-Importance”的数据引如此大的波动。或许本月初开始的恐慌有些夸大,但这份数据并不见得平息了衰退的恐慌。摩根大通的 Lakos-Bujas 向市场发出警告,股市不再是单向上行交易,而是越来越对围绕经济增长下行风险,美联储降息的时机,仓位过多,估值过高,以及总统选举和地缘政治不确定性上升展开的双向辩论。

Source: TradingView; SignalPlus, Economic Calendar

另外,经过这两轮事件后我们观察到,币价的上涨带动 Vol Skew 回升,自看跌一侧的大量抛售更是显著增加了 BTC 十月到年底斜率,使得 25 dRR 指标在局部范围内大幅上行,波动率曲面在一夜之间发生了明显的转变。

Source: SignalPlus

Data Source: SignalPlus, ETH Top Trade

Data Source: SignalPlus, BTC Top Trade

您可在 t.signalplus.com 使用 SignalPlus 交易风向标功能,获取更多实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlusCN,或者加入我们的微信群(添加小助手微信:SignalPlus 123)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。SignalPlus Official Website:https://www.signalplus.com