8 月 7 日美国财政部宣布发行 580 亿美元 3 年期国债,中标收益率报 3.810% ,低于发行前交易水平( 3.812% ),除两年期国债外,基准收益率小幅上升至盘中高点。收益率逼近结束倒挂,十年期美债收益率抹去了上周五自非农就业数据发布以来的跌幅,现报 3.908% 。

另一方面,日本央行重新转鸽,副行长内田真一出面喊话,称不会在市场不稳定的时候进行加息,出现了一些因素使得央行对加息的态度更加谨慎,日元承压下跌。

Source: Investing 美国十年期国债收益率;USD/JPY 汇率

数字货币方面,Ripple 和 SEC 达成和解,罚款从 SEC 最初提出的 20 亿美元大幅减少到 1.25 美元。公告发布后,市场信心得到提振,XRP 交易量增加 254% 至 53 亿美元,价格上涨 20% 。

BTC 方面,前天价格从 56000 震荡反弹回到 57000 后,收敛的实际波动率使得 IV 短暂出现熊陡走势,但价格在高点并未维持多久,晚上十点后便开始一轮新的下跌行情,并在 54800 附近得到支撑,亚盘开始后再度拉升收复所有所有失地,日间波动率大幅扩大,隐含波动率整体上涨。

Source: TradingView

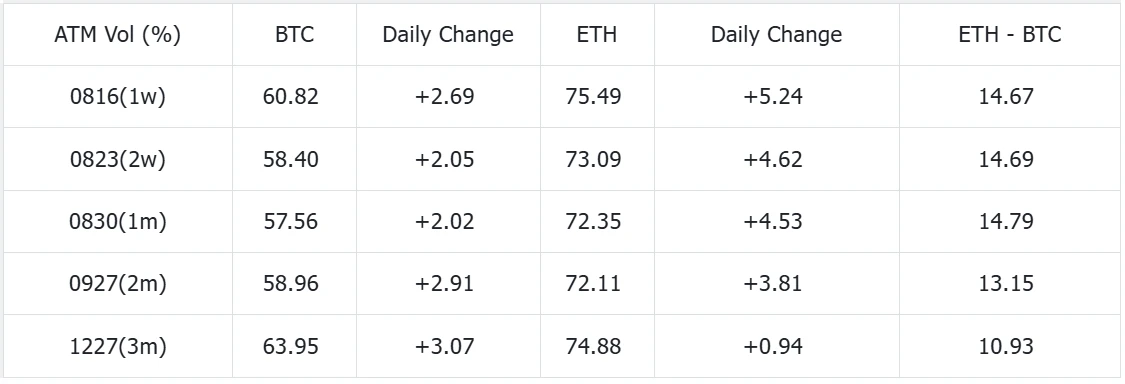

从细节上来看,BTC 远端的 IV 连日的上涨更需要引起关注,美国总统竞选和对后续美联储加息路线带来的不确定性都是市场增加押注的因素,对比 ETH 走势,这个变化区别明显,昨日的波动使得 ETH IV 大幅走平, 1 w-1 m 前端涨 4.5% 左右,远端如 12 月仅动了 0.94% (相比 BTC 动了 3.07% )。另一方面,币价再度下跌引起了看跌期权需求量的增长,两币种的 Vol Skew 出现全面下跌。

Source: Deribit (截至 8 AUG 16: 00 UTC+ 8)

Source: SignalPlus

Source: SignalPlus,Vol Skew 出现全面下跌

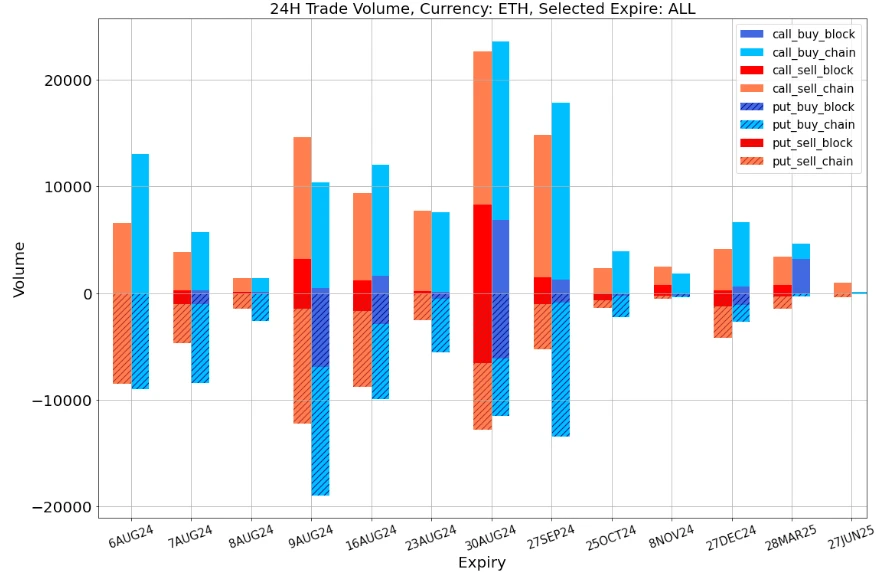

Data Source: Deribit, ETH 交易总体分布

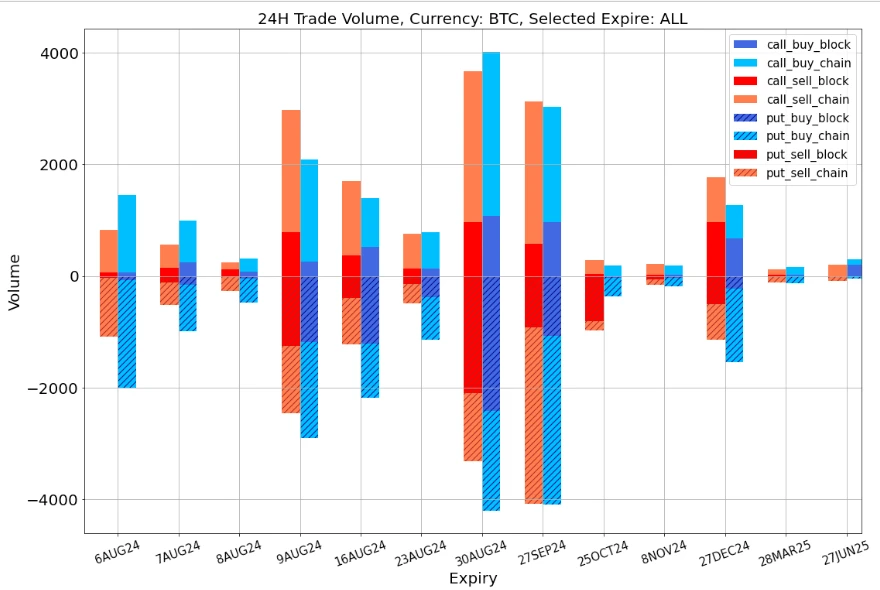

Data Source: Deribit, BTC 交易总体分布

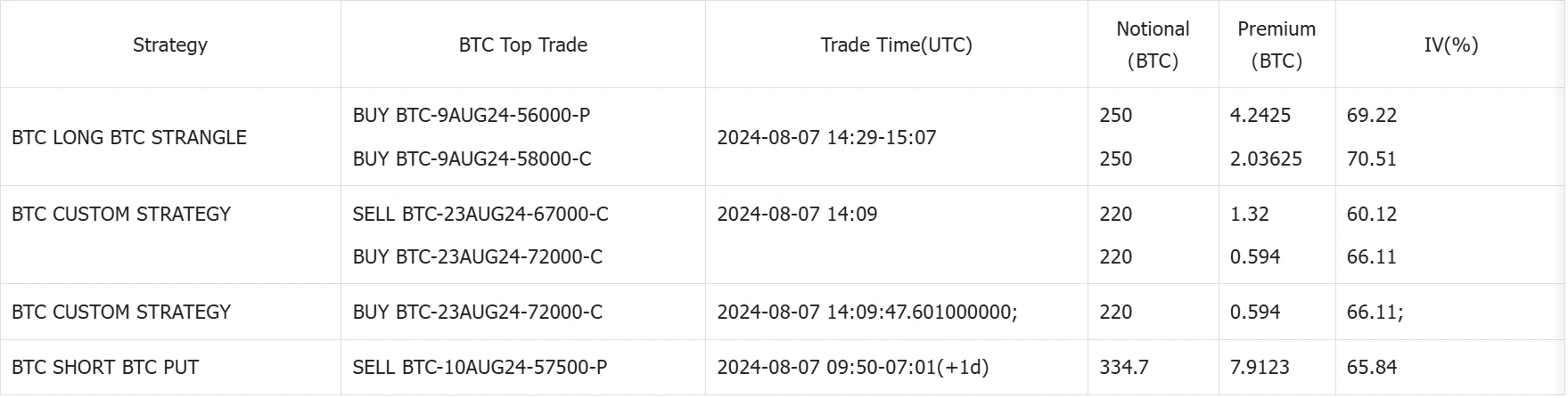

Source: Deribit Block Trade

Source: Deribit Block Trade

您可在 t.signalplus.com 使用 SignalPlus 交易风向标功能,获取更多实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlusCN,或者加入我们的微信群(添加小助手微信:SignalPlus 123)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。SignalPlus Official Website:https://www.signalplus.com