原文作者:Mary Liu,比推 BitpushNews

周四美国备受期待的消费者价格指数(CPI)报告好于预期, 6 月份通胀率降至三年多以来的最低水平。CPI 同比上涨 3% ,好过预期的 3.1% ,核心 CPI 同比下跌至 3.3% ,低于预期的 3.4% 。

CPI 数据暗示通胀在继续降温,增强了投资者押注美联储今年晚些时候降息的信心。CME Fed Watch 数据显示, 9 月降息几乎是「板上钉钉」了,数据显示美联储 9 月降息 25 个基点的概率为 84.6% ,累计降息 50 个基点的概率为 8.1% 。

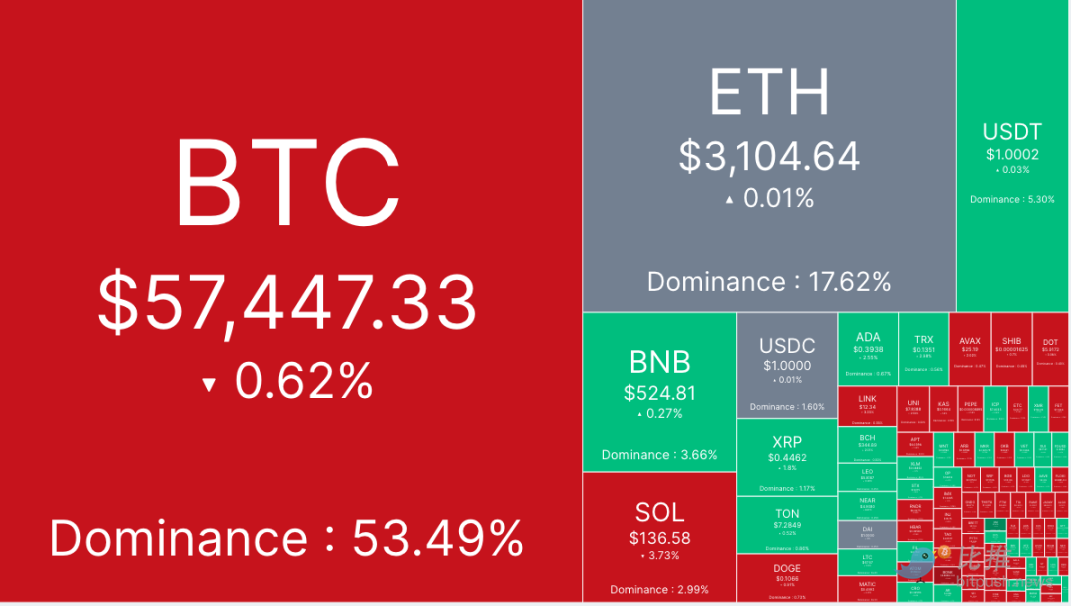

BTC 走出「过山车」行情。比推数据显示,在 CPI 发布后,比特币触及 59, 540 美元附近的高位,随后经历较大抛售,下午跌至 57, 200 美元的低点,截至发稿时交易价格为 57, 447 美元, 24 小时跌幅 0.5% 。

山寨币市场好坏参半,排名前 200 位的山寨币涨跌互现。MANTRA (OM) 表现最佳,涨幅达 12.5% ,其次是 Galxe (GAL) 上涨 9.4% ,Stacks(STX) 上涨 7.4% 。BinaryX (BNX) 跌幅最大,下跌 27.5% ,Bonk (BONK) 下跌 8.2% ,Render (RNDR) 下跌 6.9% 。

目前加密货币整体市值为 2.13 万亿美元,比特币的占有率为 53.49% 。

美股方面, 英伟达 (NVDA)、微软 (MSFT) 和 Meta (META) 等大型科技股均出现下跌,特斯拉 (TSLA) 则结束了连续 11 天的上涨势头,跌幅超过 7.5% 。 截至当天收盘时,标普指数和纳斯达克指数分别下跌 0.88% 和 1.95% ,道琼斯指数上涨 0.08% 。

德国政府 30 亿美元的抛售狂潮即将结束

Arkham Intelligence 的区块链数据显示,与德国政府有关的比特币钱包当天分批向加密货币交易所 Bitstamp、Coinbase、Kraken 以及 Flow Traders 和 Cumberland DRW 等其他服务提供商转移了总计 10, 567 个 BTC,价值超过 6 亿美元。

经过今天的交易,与德国当局相关的钱包仅持有 4, 925 个 BTC,按当前价格计算价值 2.85 亿美元,这仅占最初从 Movie 2 k 扣押的比特币的 9.9% 。

这意味着,按照目前的速度来计算,德国的比特币抛售可能最早在周五或下周初结束,因为本周迄今为止该钱包已经售出了大约 35, 000 枚比特币。

这可能有助于缓和市场的担忧情绪,过去几周,交易员一直关注市场上潜在大型卖家的链上动向,将近期的下跌与抛压联系起来。

摩根大通:预计市场将从 8 月份开始反弹

尽管比特币由于多种因素而难以获得反弹动力,但包括摩根大通在内的大多数分析师都认为前景将出现转机。

根据摩根大通发布的一份研究报告,加密市场的清算应该会在 7 月份开始消退,预计市场将从 8 月份开始反弹。

尽管预计市场情绪将出现好转,但该银行将今年迄今的加密货币净流量预测从 120 亿美元下调至 80 亿美元,并表示,考虑到比特币相对于其生产成本的高昂价格,他们怀疑之前估计的 120 亿美元的水平能否在今年剩余时间内持续下去。

以 Nikolaos Panigirtzoglou 为首的分析师表示:「预计净流量减少主要是由于过去一个月各交易所比特币储备的下降。」

分析师强调,Mt.Gox 债权人清算比特币,以及德国政府抛售比特币,可能是储备下降的原因。

Off the Chain Capital 首席执行官 Brian Dixon 在一份报告中表示:「在我看来,过去一周比特币价格的下跌是由于德国政府出售了此前查获的非法交易中的比特币。他们的政府已经将数千枚比特币转移到交易所和做市商进行销售。」

他补充道:「我认为德国政府出售比特币是一个错误,因为它应该将比特币持有在国库储备中,随着比特币的持续升值,这将为德国带来战略地缘政治优势。」

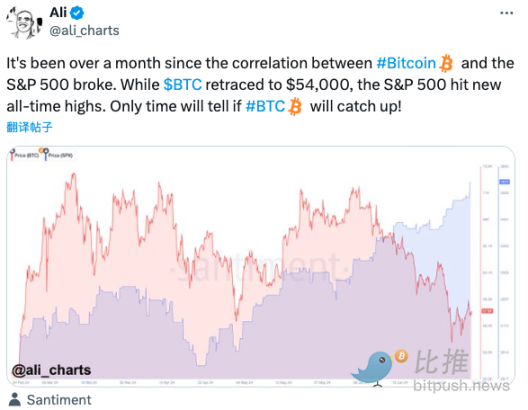

从历史上看,比特币与标准普尔指数呈正相关关系;然而,随着美股大涨而比特币在横盘整理和下跌中挣扎,这种相关性在 5 月底开始减弱。 市场分析师 Ali Martinez 在 X 平台表示,这种情况可能很快就会改变,比特币有可能通过快速的价格上涨迅速追赶上来。

他在后续推文中指出: 「比特币积累趋势得分表明投资者情绪发生了变化,自 4 月份以来经历了一段抛压阶段后,许多人现在选择积累 BTC。」

据 Bitcoin Therapy 作者 Arsen 称,近期的横盘价格走势是比特币牛市周期的典型特征。他认为,在本轮牛市结束之前,BTC 价格将达到 30 万美元左右。

他在文章中表示:「当你感到害怕时,聪明钱却在加倍下注,这是因为这种下跌并不是什么新鲜事。正如你所见,比特币每 4 年就会创下历史新高: 2012 年:比特币从 12 美元涨到 1000 美元 = 涨幅约 9, 000% ;2016 年:比特币从 650 美元涨到 19, 000 美元 = 涨幅约 3, 000% ;2020 年:比特币从 8, 000 美元涨到 69, 000 美元 = 涨幅约 1, 200% ;2024 年:?」

Arsen 补充称:「请注意,在每个连续周期中,比特币的回报率都会有个约 60% 的降幅,这意味着本周期的涨幅可能是 450% ,即每枚比特币的价格达到约 33 万美元。」