Written by: Kyle Saunders

Compiled by: Chopper, Foresight News

Most research revolves around a simple question: Who holds it? Who doesn't?

Admittedly, this is a reasonable starting point for research. Holding behavior is observable, quantifiable, and actual. But for a market with a market cap in the trillions, it might not be the most critical question.

If you are concerned with market development, regulatory policy, political discourse, or the future direction of crypto assets, there is a question that might be more practically significant: Who is considering acquiring cryptocurrency?

Because the acceptance and adoption of an asset is never a binary, either-or choice, but a gradual process.

If you only study the final stage of this process, you miss the entire conversion funnel.

Rejection → Consideration → Holding: The Three Stages of Crypto Acceptance

In a new paper I recently co-authored with Erin Fitz, we did not treat crypto acceptance as a black-and-white outcome, but defined it as a gradual process.

From late 2024 to 2025, we conducted three independent representative surveys of US adults. Based on the results, we categorized respondents into three groups:

- Do not hold and have no intention to hold cryptocurrency

- Do not hold but are considering holding cryptocurrency

- Currently hold cryptocurrency

Our first finding was straightforward yet crucial: About one-fifth of Americans do not hold cryptocurrency but are considering it.

This group is by no means an insignificant niche, a statistical error, or a group 'destined to hold.' They are a distinct segment with unique psychological characteristics and behavioral patterns, and this attribute makes them critically important.

Why is the 'Potential Holder' Group So Critical?

If the research perspective is limited to the binary comparison of 'holders' vs. 'non-holders,' it assumes all those not in the market are an undifferentiated whole.

But real-world behavioral choices are never like that.

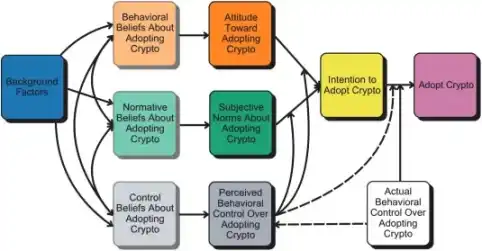

The classic social psychology Theory of Planned Behavior posits that human behavior evolves through a series of preceding stages: beliefs, attitudes, perceived control, behavioral intention. One first 'considers' before forming a 'behavioral intention'; a 'behavioral intention' precedes taking actual action. And each stage does not necessarily transition to the next.

In other words, all holders were once potential holders; but not all potential holders will ultimately become actual holders.

When we view people's engagement with cryptocurrency as an ordered, gradual process rather than a binary characteristic, an interesting conclusion emerges: The factors influencing 'consideration to hold' are not entirely the same as those driving 'actual holding.'

There is a filtering mechanism at work in this conversion funnel.

Which Factors Influence 'Consideration'? Which Drive 'Actual Holding'?

Some common influencing factors aligned with expectations: Younger individuals, men, those more open to new experiences, and those with a higher tolerance for financial risk were more likely to cross both the 'rejection→consideration' and 'consideration→holding' thresholds.

But two sets of significantly different patterns are worth highlighting.

Factors more strongly associated with 'Consideration to Hold':

- More conservative operational ideology

- Support for AI technology development

These factors play a role in the early stages of the crypto acceptance process, explaining why people might be open to cryptocurrency, but not necessarily pushing them to take the final step to 'actually hold.'

Factors more strongly associated with 'Actual Holding':

- Already hold stocks

- Need for chaos

Risk tolerance was the most influential factor overall: From the lowest to the highest levels, the probability of behavioral choice changed dramatically, with the probability of rejecting crypto decreasing by 32 percentage points and the probability of actually holding crypto increasing by 27 percentage points.

Here is a brief summary of the core differences:

Our survey data also aligns closely with the actual crypto market landscape: Bitcoin dominates overwhelmingly among both 'potential' and 'actual' holders (with Ethereum second), and many are open to multiple cryptocurrencies. The market itself corroborates this finding.

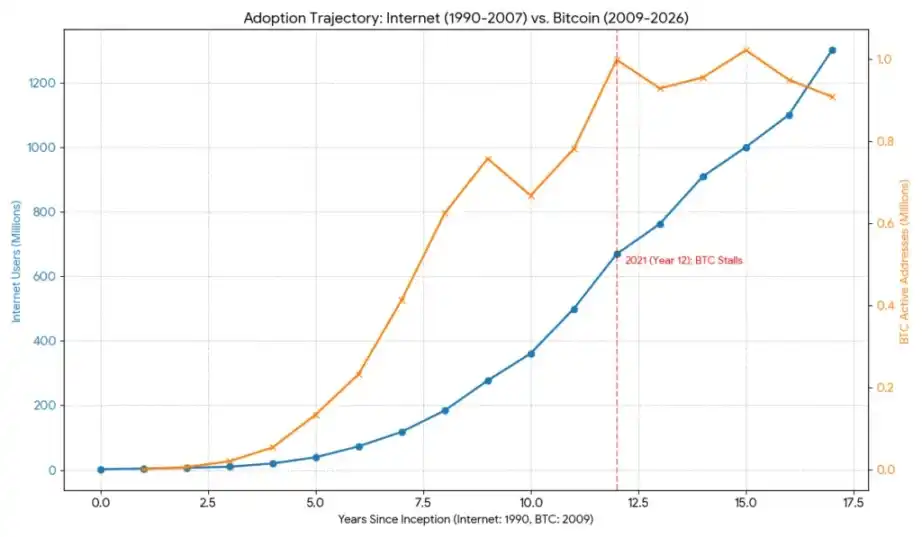

To understand how this landscape fits the broader technology diffusion curve (and why the 'potential holder' stage will determine whether crypto development stalls or scales), one can compare Bitcoin's adoption trajectory with that of the early internet. Survey data shows AI technology acceptance in the US reached about 55% in 2026.

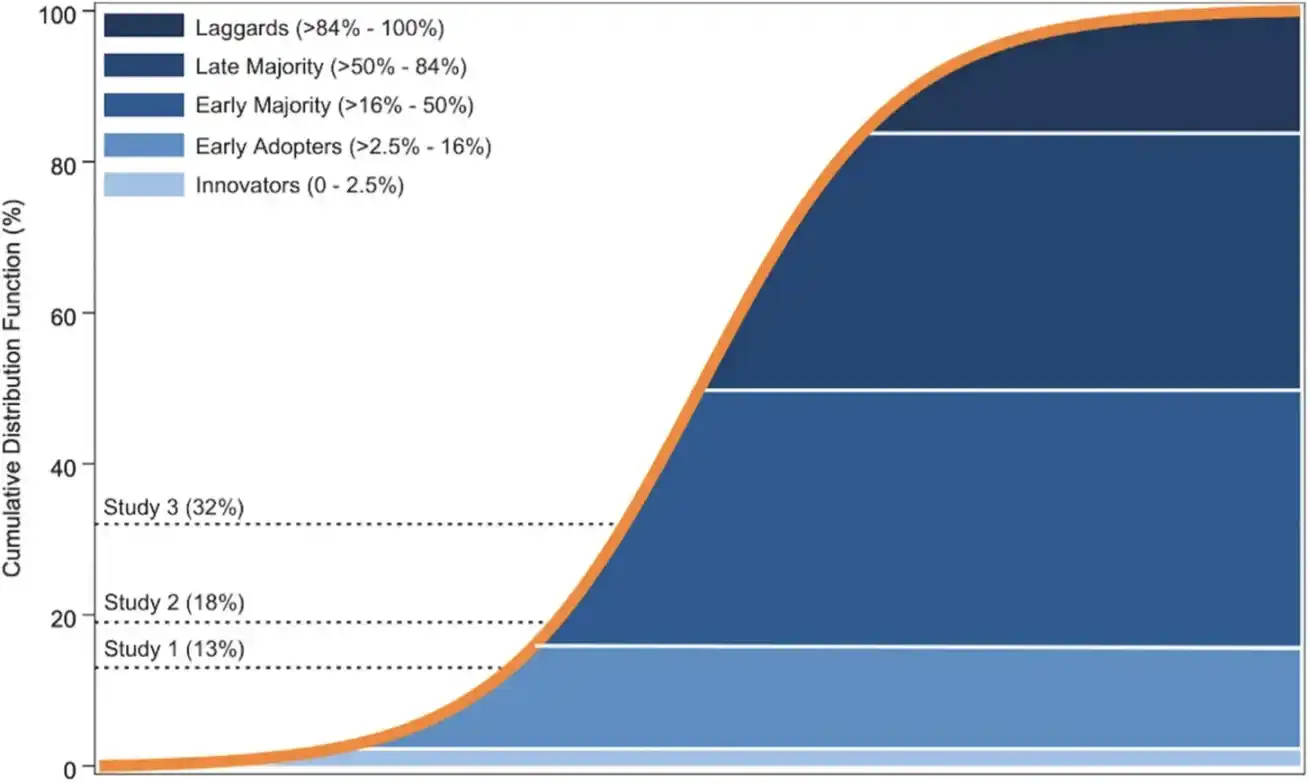

Furthermore, this chart from the paper shows how crypto acceptance fits the Rogers Diffusion of Innovations curve:

This is an adapted version of Rogers' 2003 Diffusion of Innovations curve. The solid orange line is the S-curve (the cumulative distribution function, with the scale on the left vertical axis). The blue area under the curve represents the probability distribution of the five adopter categories in Rogers' model, divided based on standard deviations from the mean in a normal distribution. In a normal distribution, these areas represent the probability proportion of each category in the whole population: Innovators (2.5%, 0 to mean minus 2 SD), Early Adopters (13.5%, mean minus 2 SD to mean minus 1 SD), Early Majority (34%, mean minus 1 SD to mean), Late Majority (34%, mean to mean plus 1 SD), Laggards (16%, mean plus 1 SD to 100%). The black dashed lines represent the self-reported cryptocurrency holding rates from our three studies (Study 1: 13%, Study 2: 18%, Study 3: 32%).

The Implications of These Findings Extend Beyond Crypto

You could interpret these results narrowly as consumer segmentation, but they have broader significance.

For Market Growth

The expansion potential of the crypto market lies not in converting staunch 'rejecters' into holders, but in figuring out what prevents potential holders from becoming actual holders. This barrier might not be ideological, but rather people's perception of their behavioral control, concerns about market volatility, or issues with asset liquidity.

For Regulatory Policy

If policymakers view only current cryptocurrency holders as the group with political influence, they misjudge the market's current state. The policy direction in the digital asset space will likely be determined by these open-minded yet undecided potential holders. Their preferences, risk profiles, and trust in institutions are critically important, especially as the crypto regulatory framework takes shape in 2026.

For Public Discourse

Online discussions often fall into polarization: either pro-crypto or anti-crypto. But our survey data shows a large, psychologically distinct middle group exists in reality. Historical experience suggests that it is this middle group, not the early adopters, that ultimately determines whether an innovation achieves widespread adoption, stalls, or triggers a backlash.

Acceptance and adoption are inherently gradual processes.

The core insight of this research is not just specific to the crypto space, but also a shift in research methodology and perspective.

When we simplify complex behaviors into binary, either-or choices, we risk conflating the behavioral rules of different stages. The factors that make people open to a new thing are not necessarily the same ones that drive them to take actual action.

This applies not only to cryptocurrency but also to the acceptance of AI technology, political participation, trust in institutions, and many other behavioral choices I've explored in this column.

The overlooked middle stage often holds the most intriguing behavioral patterns.

The acceptance and adoption of cryptocurrency is never simply a personality trait or an ideological signal, but a step-by-step behavioral process.

If you ignore this intermediate 'potential holding' stage, you will misjudge both the true direction of the market and the underlying political and social logic.