A single wallet has dumped a massive 285 million UST onto Curve and Binance, resulting in massive outflows that caused UST to briefly depeg.

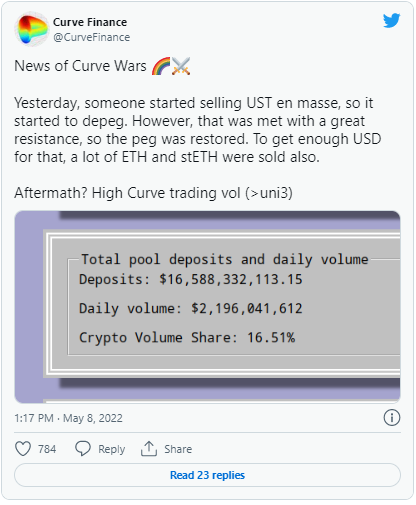

Curve Finance, a decentralized exchange built on the Ethereum blockchain that focuses on stablecoin swapping, reported the massive UST selling: "Yesterday, someone started selling UST en masse, so it started to depeg. However, that was met with great resistance, so the peg was restored. To get enough USD for that, a lot of ETH and stETH were sold also."

LUNA supporters, however, believe that this might be a "deliberate and coordinated attack" that was orchestrated by a single player to cause damage to the project as this was followed subsequently by "massive shorts on LUNA."

On Twitter, Terra co-founder Do Kwon downplayed these concerns, tweeting that he "loves chaos." Subsequently, Terra (LUNA) fell to the ninth spot in terms of market capitalization. Terra UST, however, remains in 10th place in terms of market capitalization while ranking third largest stablecoin in terms of market value.

UST is an algorithmic stablecoin that maintains its peg to the dollar through both Terra's native LUNA tokens and billions of dollars in Bitcoin. Unlike traditional stablecoins, algorithmic stablecoins are supported by an algorithm that creates incentives for traders to keep the price stable.

Justin Sun buys UST

Tron founder Justin Sun, in a tweet, has stated that he was buying UST. As shared by crypto journalist Colin Wu, data shows that Justin Sun's address has purchased about 1 million UST on Curve. TRON had just recently launched its algorithmic stablecoin, USDD, which imitates UST.

According to Terra analytics, UST in Anchor reserves has witnessed a net outflow of about 2.25 billion in the last two days. Presently, UST in Anchor reserves has fallen by 17.93%. The price of Terra (LUNA) has fallen more than 14% over the last 24 hours, becoming the worst-performing cryptocurrency among the top 10 cryptocurrencies by market value.