原创 | Odaily星球日报

作者 | Asher

编辑 | 秦晓峰

近期由于 BTC 的持续下跌使得铭文市场无论是一级打新,还是二级交易都相对冷清。但 ARC-20 板块的铭文仍存在一定热度,尤其是夸克(QUARK)、智子(SOPHON)。Odaily星球日报带大家详细了解 ARC-20 代币以及该生态的热门项目。温馨提示,市场波动巨大,投资前务必进行充分的研究。

ARC-20 资产

夸克与智子都属于 ARC-20 代币,ARC-20 代币是一种染色币模型,注册信息被刻入交易脚本,余额使用 UTXO 的 Satoshi 数量表示,转账功能完全由 BTC 主网处理。ARC-20 标准规定每个 ARC-20 代币的最小单位是 1 Satoshi。这不仅确保了代币的最低价值,还使得创建和管理 AEC-20 资产变得高效,灵活。值得一提的是,ARC-20 命名系统的唯一性降低了山寨代币带来的负面影响,使整个系统清晰和统一。下面,着重介绍该板块热度较高的两个项目——QUARK 与 SOPHON。

QUARK:持币地址最多

在 12 月的最后一周,比特币生态几乎全网都在挖夸克(QUARK),其英文含义 QUARK 是构成物质的基本单位,与组成 Bitcoin 的最小单位 SATS 类似,夸克在一定程度上具有 Meme 属性。由于夸克拥有持币地址多、基础共识强等特点,许多社区成员认为夸克有望成为 Atomicals 生态中能出圈的 Meme 币。

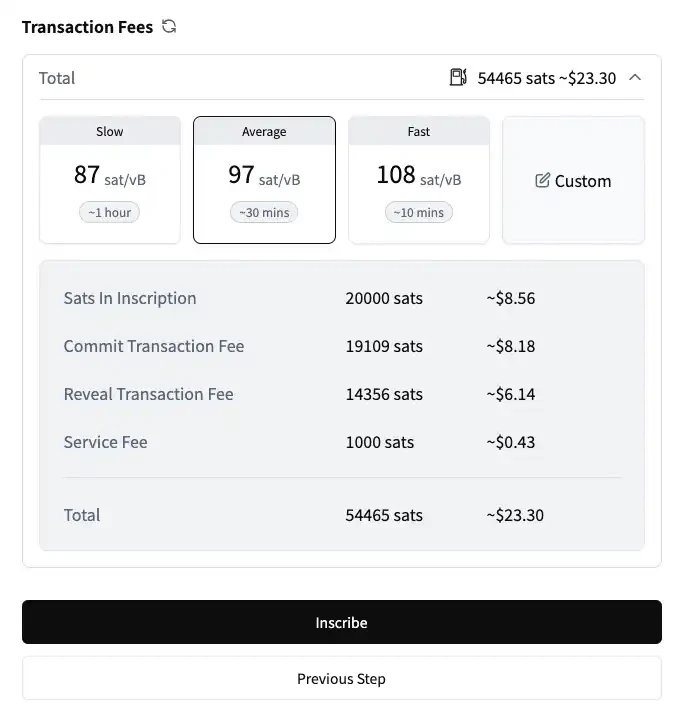

从参与度的角度来看,夸克的设计具有一定优势。一方面,夸克的总量为 50 万,每张夸克包含 2 万枚,这意味着需要相当长的时间才能铸造完毕。这样的设计可以吸引更多人参与,形成一定的共识。另一方面,夸克挖矿的难度为 6 ,相对于 Electron 和 Neutron 来说相对简单,能让更多的人参与一级的铸造过程。整个铸造过程,每张夸克的平均成本大约在 20-30 美元,下图为 BTC 网络 Gas 在 97 左右的铸造成本,约为 23.2 美元。

夸克铸造成本(Gas= 97)

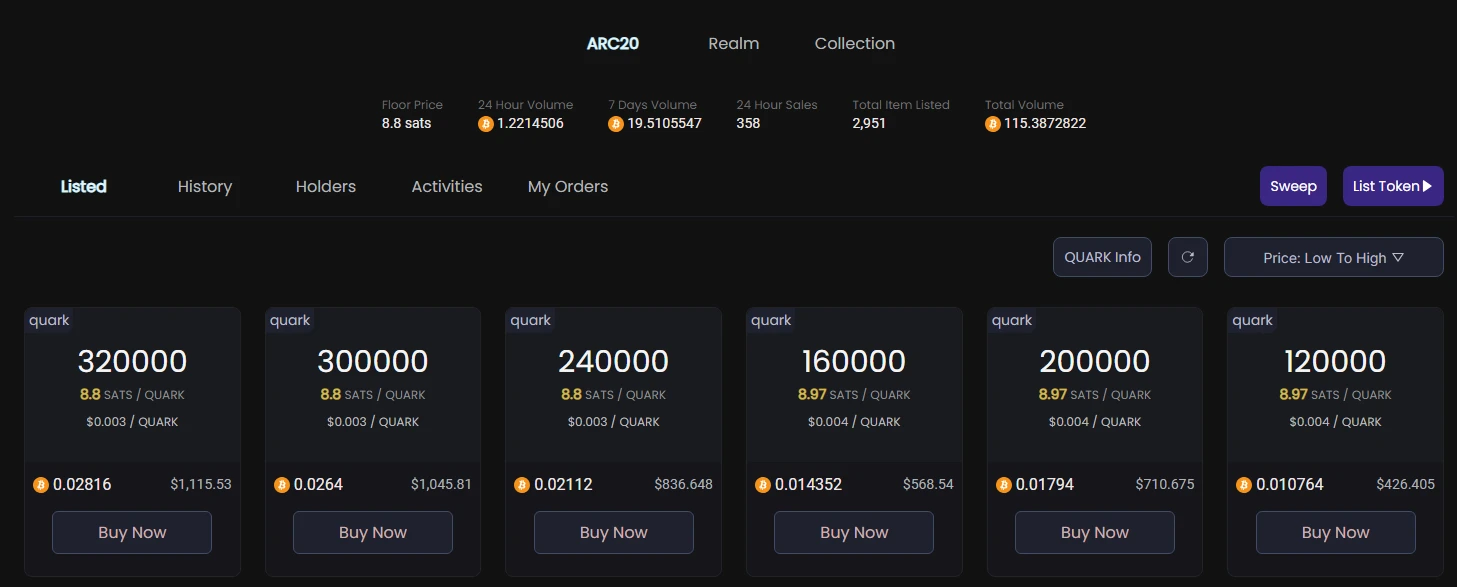

在二级市场方面,夸克的价格最高为 17.4 SATS,折算成每张(即 2 万枚夸克)的价值为 0.00348 BTC,约为 139 美元,相较于一级铸造的平均成本,最高涨幅 450% ,目前价格为 8.73 SATS。夸克的持币地址高达 14181 ,为 ARC-20 资产中持币地址最多的代币。

夸克二级市场

二级市场购买链接:https://atomicalmarket.com/market/token/quark。

SOPHON:每张需锁仓 10 万聪 BTC

简介

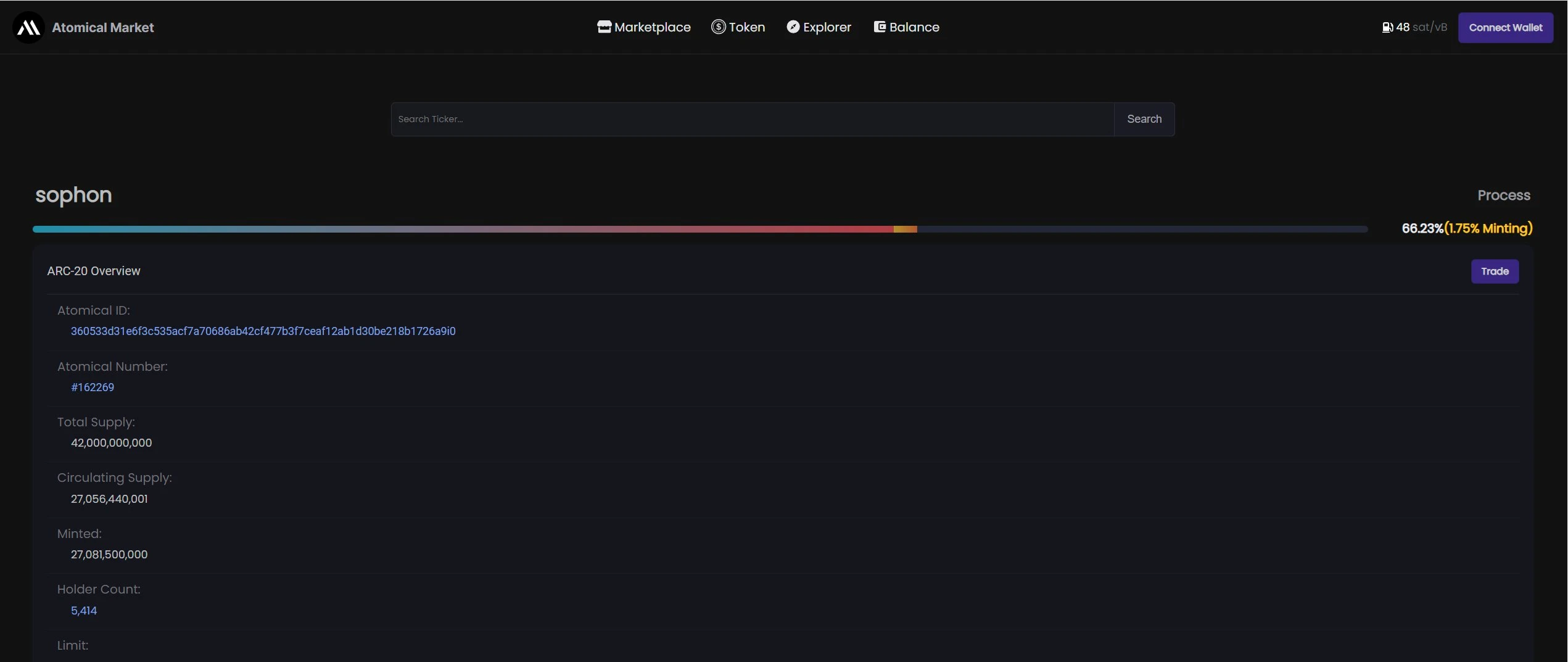

智子(SOPHON)与夸克不同。简而言之,每挖一张智子都需要锁定 10 万聪的 BTC,假设当前 BTC 价格为每枚 40000 美元,那么需要锁定相当于 40 美元价值的 BTC,并额外支付一笔 Gas 费用。考虑到智子的总量为 42 万张,根据挖智子的规则,全部智子挖完相对于锁仓 420 枚 BTC。

根据铸造智子的几天来看,除了每张智子必须锁定的 10 万聪 BTC 外,Gas 成本大约在 5 到 7 美元之间。因此,即便智子归零,本体依然价值 0.001 BTC。实际上,铸造或购买智子相当于以另一种形式储存 BTC。如果对未来市场看好,持有智子可能是一个不错的选择。

智子铸造时

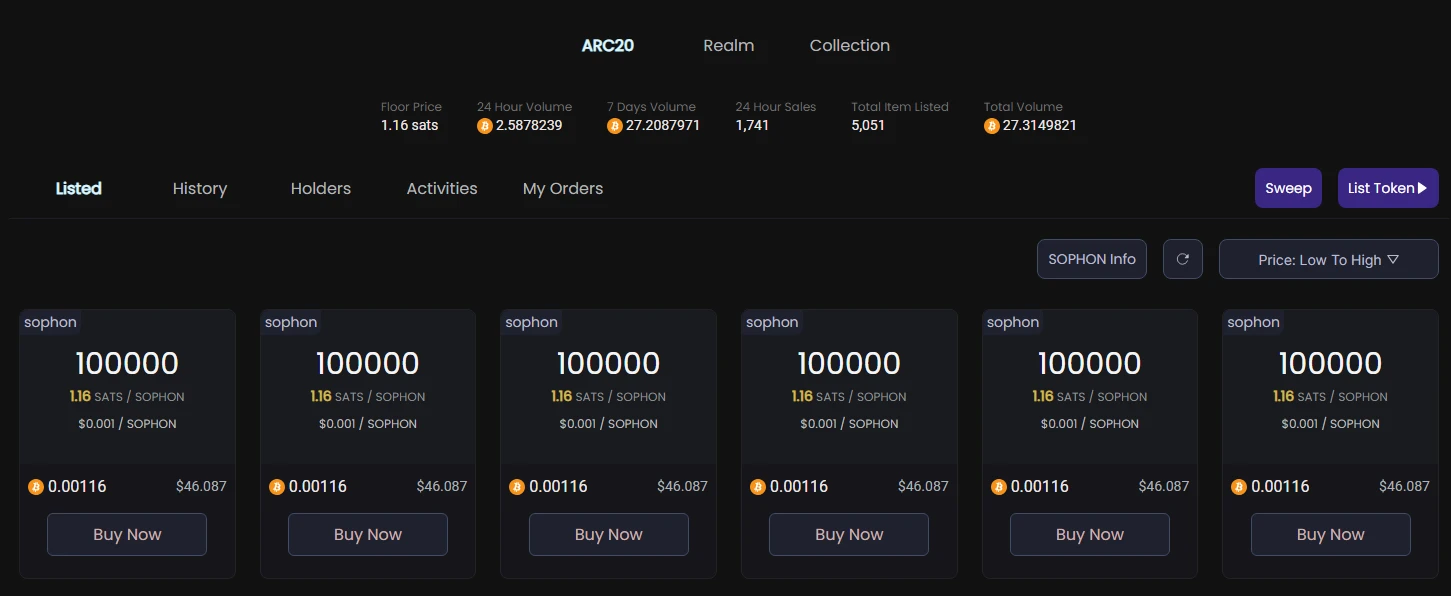

在二级市场方面,智子的主要成交价格维持在 1.16 SATS 至 1.2 SATS 之间,折算成每张(即 10 万枚智子) 的价值约为 0.00116 BTC 至 0.0012 BTC,相当于 46.5 到 48 美元。24 小时交易量方面,智子目前仅次于 ATOM,为 2.35 BTC(约 9.4 万美元)。持币地址方面,智子目前仅次于夸克,为 7474 。因此,从二级市场表现来看,虽然持币地址多、交易量大,但是智子相较于一级铸造并没有明显的涨幅。

智子二级市场

二级市场购买链接:https://atomicalmarket.com/market/token/sophon。

综述

对于 ARC-20 资产,社区普遍期待两个可能落地的利好:一是 OKX Web3 钱包会上线 ARC-20 市场;二是币安钱包若推出铭文市场,那么 ARC-20 也可能会同步推出。若利好兑现,夸克与智子将有机会成为 ARC-20 板块的焦点,或许会有一个不错的投资回报率。