原文作者:Karen,Foresight News

Crypto 整体市场向好趋势下,NFT 市场出现复苏迹象,蓝筹地板价出现普遍性的反弹,头部 NFT 系列 BAYC、CryptoPunks 在过去 30 天的地板价增幅分别为 19% 和 33% 。

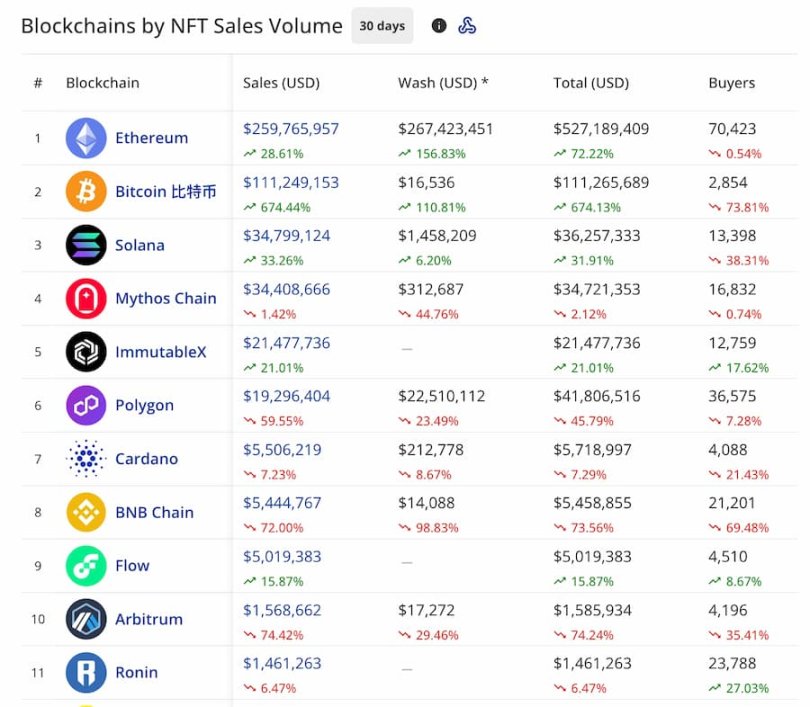

与此同时,近三个月,以太坊 NFT 市场成交量小幅反弹,但是否扭转有待观察。按公链网络来看,过去 1 个月,以太坊 NFT 交易额达 2.6 亿美元,稳坐第一宝座。随着比特币生态崛起,比特币上 NFT 成交量也再次冲到第二,过去 1 个月成交量达到 1.1 亿美元。

从交易数量和地址来看,以太坊 NFT 交易笔数在 7 月份以来稳定蓄力,独立 NFT 交易地址数量虽降速放缓,但未见反弹趋势。

笔者看来,当前 NFT 市场虽有复苏迹象,但能迎来复苏大拐点,需要新系列、新叙事、新金融方式的刺激注入新的活力,也受到 Crypto 整体市场的影响。

以太坊 NFT 成交稳居第一,比特币直冲第二

根据 CryptoSlam 数据,按公链网络来看,截至撰稿时,近一个月,以太坊上 NFT 交易额达到近 2.6 亿美元(剔除对敲交易 2.67 亿美元),稳坐第一宝座。而在比特币生态持续火热的背景下,比特币上 NFT 成交情况也呈现出高增长趋势,继今年 5、 6 月份后再次冲到第二,过去 1 个月成交量达到 1.1 亿美元,其中,本月迄今为止的成交量就超过了 9800 万美元。

来源:CryptoSlam

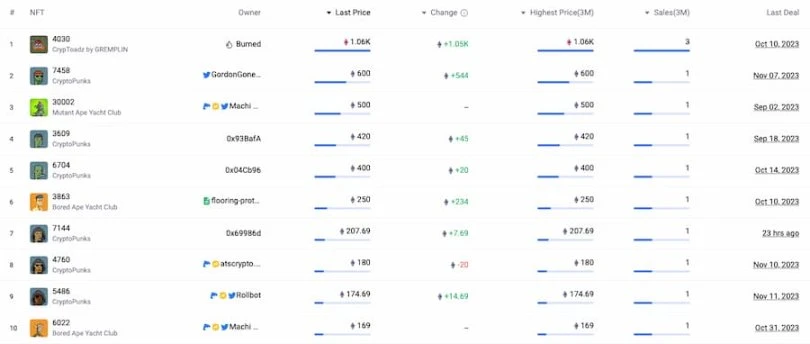

下图是过去 3 个月成交价最高的 10 个 NFT。

来源:NFTGo

其次是 Solana、Mythos Chain、ImmutableX 和 Polygon,这四个网络过去一个月 NFT 成交量均在 2000 万美元至 4000 万美元之间。

这里也提下 Mythos Chain,Mythos Chain 是一个许可 EVM 区块链和游戏生态系统,托管头部链游工作室 Mythical Games 的旗舰游戏资产和 NFT 市场,如 CS:GO 皮肤市场 DMarket(占据 Mythos Chain 链上成交量的 99% )、NFL Rivals(由美国国家橄榄球联盟 NFL 与 Mythical Games 合作推出)、Nitro Nation World Tour 和 Blankos Block Party。Mythical Games 是 Mythos 的初始贡献者和支持者。

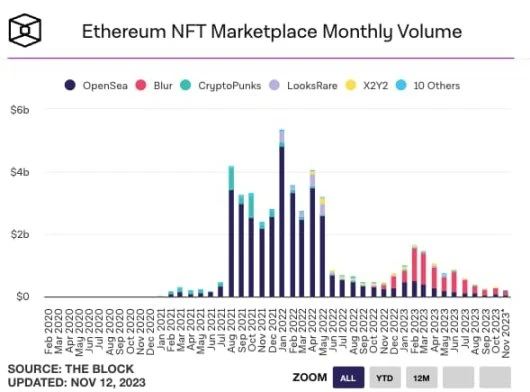

以太坊 NFT 市场成交小幅反弹,是否扭转有待观察

下面 The Block Data 这张图表能直观地反映出以太坊 NFT 市场成交量的变动情况(过滤掉清洗交易),可以看到,今年 2 月份以来,以太坊 NFT 市场成交状况呈逐步下降趋势, 9 月份后结束下降趋势, 10 月份的成交量超过 3 亿美元, 11 月份至今的成交量为 2.3 亿美元,出现反弹趋势,但目前说开始扭转可能还为时尚早。

来源:The Block Data

若细分 NFT 市场, 3 月份以来,大部分时间段内 Blur 成交量占比稳定在 50% 到 70% 之间,OpenSea 的市场占比在 6 月份一度跌至 16% 左右,随后逐步恢复,在 10 月 15 日至 10 月 22 日短时占据 68% 的市场份额,目前降到 25% 左右。

来源:The Block Data

以太坊 NFT 交易笔数在 7 月份以来稳定蓄力

交易笔数方面,根据 The Block Data 数据,和成交量趋势类似,年初开始,NFT 交易笔数一直延续下降趋势,尤其是 3、 4、 5 月份从每月 200 万笔骤降到每月 50 万笔,不过 7 月份以来稳定在每月 50 万到 60 万笔。

来源:The Block Data

以太坊独立 NFT 交易地址未见反弹趋势

独立交易用户的变动情况也能在很大程度反应出 NFT 玩家的整体情况。较为失望的是, 2 月份以来 NFT 交易用户持续减少, 10 月份每月交易用户为 15 万,相较 5 月份的 45 万已跌去 66% ,不过下降幅度在减缓,尚未看到反弹趋势。

来源:The Block Data

以太坊累计 NFT 玩家数量统计图也能体现出当前 NFT 玩家的增长曲线趋于平缓。

来源:The Block Data

以太坊 NFT 地板价普遍反弹

来自 WGMI.io 的数据显示,按照近 30 日的成交量来看,成交量最多的前 20 个 NFT 系列的地板价均出现了上涨,平均涨幅为 47% ,其中,头部 NFT 系列 Bored Ape Yacht Club(BAYC)、CryptoPunks 在过去 30 天的地板价增幅分别为 19% 和 33% 。

由 Animoca Brands 支持的跨媒体 NFT 项目 The Grapes 系列增幅最大,达到 200% ,第一代 Pixelmon 和 CrypToadz by GREMPLIN 的增幅也超过 100% ,Doodles 在遭受重创后在过去一个月反弹 93% 。头部 NFT 系列 Bored Ape Yacht Club(BAYC)、CryptoPunks 在过去 30 天的地板价增幅分别为 19% 和 33% 。

来源:WGMI.io

下面这张图能直观地显示近一年半蓝筹 NFT 地板价变动情况。

来源:The Block Data

NFT 谷歌趋势热度持续低迷

谷歌趋势可以在一定程度上反映出圈外对 NFT 的关注程度。下图显示了 2021 年以来全球范围内 NFT 的搜索热度。如果将 2022 年 1 月份最高搜索热度的值视作 100 分, 2022 年 12 月份的小高峰为 19 ,今年 5 月份以来的热度值在 5 到 7 之间。

来源:Google Trends

若按区域显示,中国大陆地区的搜索热度最高,其次为香港地区、新加坡、直布罗陀、尼日利亚、澳门地区、开曼群岛和韩国。

盈亏地址数比严重失衡

根据 NFTGo 数据,排除疑似清洗交易后,过去 30 日,盈利大于 1 ETH 的唯一地址的数量为 5.77 万个,亏损大于 1 ETH 的唯一地址数量为 49.55 万个,数值比例为 1 比 8.6 。30 天盈亏是指过去 30 天内销售产生的已实现利润与每个地址持有的 NFT 的预计未实现利润之和。

来源:NFTGo

比特币上累计铭刻 3895 万枚 NFT,近 68 万个钱包持有

OKLink 比特币浏览器统计到的比特币 NFT 系列有 2382 个,下面是持仓地址数最多的 10 个系列。

来源:OKLink 比特币浏览器

据 Bitcoin NFTScan 数据显示,截止到 11 月 13 日,比特币网络上累计铭刻了 3895 万枚 NFT,在链上创造了 2482 枚 BTC 的 Gas 费消耗,目前持有比特币 NFT 资产的钱包地址有 67.89 万个。

下面两张图可以看出今年以来比特币 Ordinals 铭刻数量和费用的变动情况,Ordinals 热度高峰期在今年 5 月份、三季度以及本月。

来源:Dune

来源:Dune