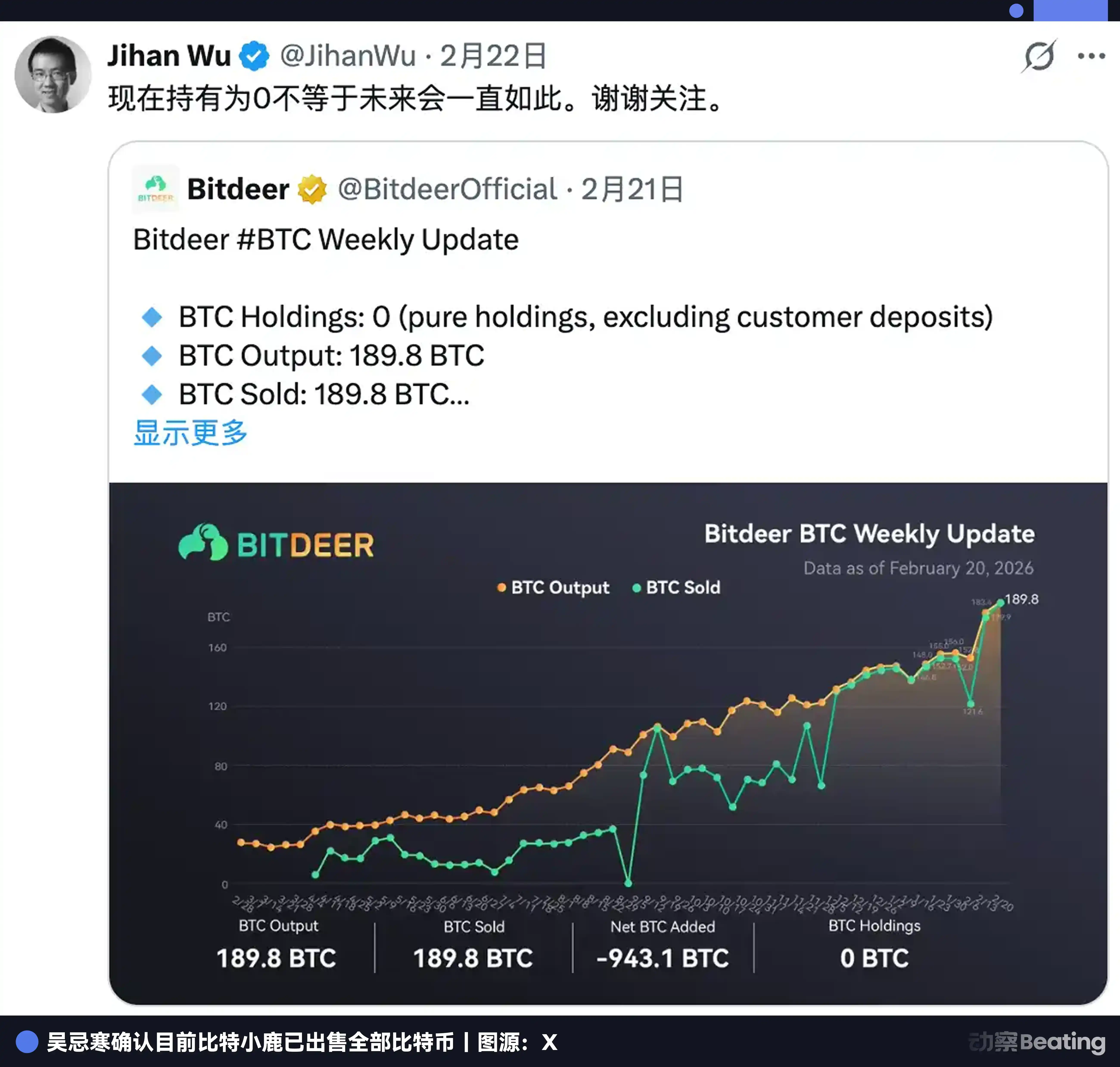

On February 20, 2026, Bitdeer posted its weekly production update on X: 189.8 BTC self-mined that week, sold. Remaining inventory of 943.1 BTC, sold in one go.

Bitcoin balance: 0.

In fact, from day one, Bitcoin mining has been a form of time arbitrage.

Using today's electricity and machines to exchange for tomorrow's Bitcoin. No garage workshops, no need for customers, no need for a brand. What's invested is the cost of the present, betting on the price of the future. If the judgment is correct, time makes you money.

This logic has run for over a decade. What Jihan Wu is doing now is changing the target of this logic.

The target has shifted from the coin price to the long-term price of computing power demand in the AI climate. The method has changed from using electricity to exchange for coins, to borrowing money to buy land. The object of arbitrage has changed, the structure of arbitrage has not.

In the same week it cleared out its Bitcoin, Bitdeer also priced a new $325 million bond.

According to Bitdeer's financial report, as of December 31, 2025, Bitdeer's book borrowings were $1 billion. So the total debt is approximately $1.3 billion.

The debt is real, the land purchases are real, but the outcome of this tough battle might not be known until 2029.

I. A Mining Company That Doesn't Want to Do AI Isn't a Good Company

Bitdeer was established in 2018, starting as a shared mining platform. It is currently one of the world's largest listed mining companies, with a self-mining hashrate of 63.2 EH/s, ranking first in self-mining hashrate among global listed mining companies, accounting for about 6% of the entire Bitcoin network's hashrate.

But now, Jihan Wu doesn't want to sell computing power anymore, he wants to get into power.

Looking at Bitdeer's financial report, as of early 2026, Bitdeer's global power pipeline total capacity is 3002 MW, of which 1658 MW is already online and operational, and 1344 MW is under construction or planned. A single hyperscale data center for Microsoft or Google is typically in the 100 to 300 MW range.

In other words, 3002 MW is equivalent to packing the power demand of 10 to 30 Google hyperscale data centers into one company. So Bitdeer's pipeline, on paper, is very substantial.

The main use of the $1.3 billion debt is to lock in power and land assets globally, paving the way for the transition to AI data centers.

The first is Rockdale, Texas, 563 MW (including 179 MW expansion), operational, primarily for mining. This is the core business, with stable cash flow.

Second, Clarington, Ohio, 570 MW, 30-year lease, power contract signed, originally planned for completion in Q2 2027, positioned as an HPC/AI core site. This is the core of the entire AI transition plan. It is also currently the biggest risk, which we will detail later.

Then, Tydal, Norway, 175 MW, currently converting a mining farm into an AI data center, expected completion by the end of 2026, capable of providing 164 MW of effective IT load. Hydropower resources, competitive energy costs. Conversion cost is much lower than new construction. Currently the fastest progressing, lowest risk card.

Land, power, and facilities—these three things are known in the AI industry as "the hardest assets to replicate." Bitdeer has spent a decade in mining farm operations accumulating these for itself.

Worth mentioning separately is something rarely discussed: SEALMINER. Bitdeer is not just building facilities; it is also developing its own mining machine chips. The SEAL series has iterated to the third generation; SEAL03 has an efficiency of 9.7 joules per terahash; the A3 Pro, mass-produced in September 2025, is already in the global first tier. SEAL04 aims for 5 joules per terahash; if achieved, it will surpass all mass-produced mining machines on the market. The gross margin for self-developed chips exceeds 40%, far higher than mining itself.

This is him replaying what he did at Bitmain: from buying shovels from others, to making shovels himself.

II. How Much Was Borrowed, and How Much Can AI Bring In

To pursue AI, by the end of 2025, Bitdeer's book borrowings exceeded $1 billion. Adding the new $325 million bond in February 2026, the total debt scale exceeds $1.3 billion.

In less than two years, multiple rounds of financing. In May 2024, Tether invested $100 million to become the second largest shareholder,附带认股权证,可以再追加 5000 万 (with attached warrants, allowing for an additional $50 million). Three months later, the first $150 million convertible bond landed, with an 8.5% annual interest rate. In November of the same year, a second $360 million, with the interest rate pressed down to 5.25%.

In November 2025, a package deal: $400 million convertible bond plus $148.4 million equity issuance, two matching tranches. In February 2026, another $325 million convertible bond plus $43.5 million equity, while using $135 million of it to repurchase the earliest batch of 2029 debt, pushing the repayment deadline to 2032.

Total over $1.4 billion. Money flows to mining machines, data centers, AI infrastructure, plus rolling debt extensions.

However, with each bond issuance, Bitdeer's stock price fell 10% to 17%. This has become a fixed market reflex. But fortunately, the company got the money each time.

The heart of the borrowing structure is the convertible bonds. This new 2032 bond has an initial conversion price of about $9.93, a 25% premium over the simultaneous equity issue price of $7.94. If the stock price rises to that level, the bondholders convert to stock, not taking cash. The company doesn't actually have to repay the money, it just needs the stock price to rise.

The logic of convertible bonds is betting that one's own stock price will rise. This itself is a gamble on whether the AI narrative will be recognized by the market. The annual interest burden, calculated at an average 5% interest rate on a $1.3 billion principal, is over $65 million per year. And the full-year 2025 AI/HPC Cloud revenue was less than the spare change for 6 months of interest.

Currently, this interest is being rolled over by issuing more debt. It's impossible to say the pressure isn't great.

With such large investment, there must be the expectation of more objective returns. So let's look at Bitdeer, how much can AI bring in?

The AI business now makes $10 million a year, accounting for less than 2% of total revenue. For a company with a market cap of nearly $2 billion, this number is almost negligible.

Of course, this won't be the final outcome.

Bitdeer's GPUs increased from 584 to 1792 in three months, tripling. Utilization rate dropped from 87% to 41%, mainly because machines were added too fast; B200/GB200 are still in the customer testing phase and haven't started generating revenue yet. The power is ready, machines are being installed, the denominator is exploding, just the revenue hasn't caught up.

How high is the ceiling?

Roth/MKM estimates that with full HPC capacity落地, the annualized revenue potential is $850 million. Management is more aggressive: 200 MW fully dedicated to AI cloud, annualized over $2 billion, three times the full-year 2025 mining revenue.

But both numbers come with three prerequisites: construction completed on schedule, securing hyperscaler-level long-term contracts, GPUs running at full capacity.

None of these three conditions have been met yet.

This is the battle Bitdeer is fighting: mining supports AI, AI is painting a picture of the future, whether that picture can become reality depends on execution over the next two or three years.

III. The Tough Battle Lies in How Narrow the Time Window Is

$1.3 billion in debt sounds dangerous. But Bitdeer's debt structure is designed to be more stable than it appears.

Highly leveraged companies usually die for the same reason: debt matures集中, cash is insufficient, forced to sell assets at a loss.

Bitdeer set the maturity dates for three batches of convertible bonds in 2029, 2031, and 2032 respectively.

To some extent, this is a deliberately created buffer zone. When the first batch matures, Tydal and Clarington should theoretically be operational; when the second batch matures, AI revenue should already be able to speak for itself; when the third batch matures, what kind of company this is, the market will have its own judgment by then. Three nodes, three opportunities to renegotiate.

But while the convertible bonds buy time, Wall Street isn't buying it because of that. Keefe Bruyette cut the target price from $26.5 to $14. The current stock price is around $8. The market's signal is realistic: for a transformation story, we need to see revenue.

But all this pressure gives Jihan Wu the thing he needs most, and the most cruel thing: time.

The smooth path might run like this: By the end of 2026, the Tydal conversion is complete, the 164 MW hydropower data center in Norway goes online, European customer contracts start coming in. In 2027, the Clarington lawsuit is won, the Ohio 570 MW officially starts construction, US major customers follow. By 2028 to 2029, the two core assets are operating at full capacity, revenue moves towards the $1 billion level, analysts re-label Bitdeer from a mining company discount to an AI infrastructure premium. In 2029, the first batch of bonds matures, bondholders look at the stock price and most likely choose to convert to equity, not cash.

Every tough battle in this, Jihan Wu must hit the timeline.

Then there's Clarington.

Within the same industrial park in Ohio, there is a steel manufacturer called American Heavy Plate Solutions, which signed a 30-year lease for 9.9 acres of land in 2018. They are suing Bitdeer: building an AI data center will interfere with shared power, roads, railways, communication lines, violating restrictive covenants. The demand is for the court to issue a permanent injunction, preventing Bitdeer from starting construction.

Clarington represents 42% of the pipeline under construction. If it gets stuck, the entire timeline must be rewritten.

So Bitdeer's current biggest single-point risk is not debt, not the stock price, but a steel mill.

The mining side isn't idle either, catching its breath. In February 2026, the Bitcoin network difficulty surged 14.7%, the largest single jump since May 2021. With the same electricity cost, fewer coins are mined. Q4 gross margin has dropped from 7.4% a year ago to 4.7%. The mining leg is slowly thinning.

The worst path is also clear: The Clarington lawsuit drags on for two years, construction is halted; Tydal is delayed, GPU utilization continues to hover from 41%; the first batch of bonds matures in 2029, insufficient cash on hand, forced to refinance, stock price continues to dilute, the conversion threshold becomes increasingly difficult to reach.

Both paths真实 exist.

IV. Sold All the Bitcoin, Then What

There's a tradition in the mining circle: hoarding coins is faith, a endorsement of Bitcoin's long-term value.

MARA hoards 53,250 BTC, Riot hoards 18,000 BTC, Strategy hoards 710,000 BTC. The more you hoard, the more the market thinks you believe.

Bitdeer now has zero.

The official explanation is: selling coins was to provide liquidity for buying land. This makes sense. Peers are also moving in the same direction; Riot sold $200 million worth of Bitcoin for AI expansion, Bitfarms is abandoning its定位 as a "Bitcoin company," MARA is also布局 HPC.

But there's something more fundamental here than identity iteration.

From day one, the mining industry has been betting on the same thing: that something in the future will be more expensive than today's cost. Mining ten years ago bet that the coin price would rise. Buying land now bets that computing power demand will explode.

The object has changed, the logic of time arbitrage has never changed.

What Jihan Wu is really buying is the position of "no matter who wins, they have to pay me for electricity."

Not betting on which赛道 wins, just卡住 the entrance to the赛道. Amazon didn't bet on which internet company would win, it just rented servers to everyone. AT&T doesn't care what you talk about on the phone, it just cares if you made the call.

From selling products, to selling services, to collecting rent, the direction of industry evolution has only ever been this one path.

The difference is only whether you walk there yourself, or are pushed there.

Jihan Wu bought this window with over a billion dollars. He is waiting for AI money to catch up with the speed of debt.