Compiled by: Ken, Chaincatcher

Legendary investor Warren Buffett holds an almost religious, steadfast opposition to the concept of "stock splits."

The reason Berkshire Hathaway Class A shares trade at over $700,000 per share is that Buffett believes stock splits are merely a formalistic move that does not change the fundamental value of the enterprise. In Buffett's world, if you cut a pizza into eight slices instead of four, you don't get more pizza. You just have more dishes to wash.

While stock splits may not be a "big deal" from a valuation perspective, they are highly regulated activities overseen by the U.S. Securities and Exchange Commission and enforced by exchanges.

When a company announces a stock split, it must file a Form 8-K and notify shareholders in advance before the change takes effect. This critical time window allows transfer agents to adjust the share register, brokers to update internal systems, and data providers like Bloomberg to update their data feeds—so that a $500 stock doesn't appear to have crashed to $50 overnight after a 10-for-1 split.

Stock splits are not the only corporate actions that require this high level of coordination. Dividend distributions present similar complexities.

On the ex-dividend date, the stock price is adjusted downward by the amount of the dividend. Some funds, particularly high-yield income funds, take this practice to the extreme. They frequently distribute income, but these distributions are largely return of capital, essentially returning the investor's principal to them rather than paying investment profits. While the number of shares remains the same, the net asset value (NAV) is steadily eroded over time.

Tracking the performance of these funds requires a clear distinction between price return and total return.

Assume you hold 100 shares of a high-yield ETF, priced at $100 per share (an investment of $10,000). The fund distributes $5 per share monthly, with 90% classified as return of capital. After 12 months, you received $60 per share in cash (total $6,000), but the fund's NAV has dropped from $100 to $46. At this point, the total price return is negative $5,400, but the total return is $10,600 (remaining NAV $4,600 plus distributions of $6,000), a positive return of 6%.

These are precisely the problems blockchain is supposed to solve.

A single, shared ledger, updated atomically and visible to everyone simultaneously. If everyone reads from the same on-chain record, corporate actions like stock splits and dividends would propagate instantly throughout the system, eliminating the cumbersome and frantic reconciliation work currently done between isolated intermediaries.

It was this promise that led to a warm market reception when Robinhood (@RobinhoodApp) CEO Vlad Tenev announced the tokenized stock strategy in June 2025.

Six months on, Robinhood's tokens are officially live, and data is flowing. Unfortunately, some issues are beginning to surface.

The Good

Robinhood's announcement acted as a catalyst for the market.

Other issuers quickly moved to launch competing products. Backed Finance (acquired by Kraken) launched xStocks (@xStocksFi) on Solana, followed by Ondo Global Markets (@OndoFinance) launching its tokenized stock product.

RWA.xyz data as of January 23, 2026

Tokenized stocks had a truly breakout year. In the second half of 2025 alone, the asset class grew by 128%, pushing the total asset value to nearly $1 billion.

RWA.xyz data as of January 23, 2026

Robinhood's tokenized U.S. stocks and ETFs are now available to European customers. Each token is issued on the Arbitrum network, fully backed by stocks held by Robinhood, and enables 24/5 trading with zero commission. Relevant data is available on RWA.xyz.

However, accurately capturing the metrics for Robinhood's tokenized stocks has proven more complex than anticipated.

The Bad

Most blockchain data platforms index tokens assuming they follow standard conventions. For ERC-20 tokens, this means tracking mints and burns, accumulating the total supply from zero, and calculating market cap as supply multiplied by price.

This works for thousands of tokens on Ethereum and other EVM networks. But ERC-20 was not designed for securities that undergo corporate actions. The standard does not natively support stock splits, reverse splits, or benchmark adjustments driven by dividends.

Consequently, Robinhood had to use custom contracts to properly handle these events and ensure the rights of its end-users. These tokens work fine within the Robinhood App, but their mechanics are opaque to external data platforms and incompatible with DeFi protocols—both of which assume standard ERC-20 tokens.

When we compare the token supply calculated using standard ERC-20 logic with the actual on-chain data, the discrepancies are too large to ignore. Some tokens are off by a factor of 10, others by as much as 100.

Almost all errors can be attributed to two causes: (1) NAV erosion from dividends and (2) reverse stock splits.

NAV Erosion from High-Yield ETF Dividends

Data as of January 23, 2026

These are high-yield option income ETFs that pay frequent distributions, with 90% or more of the payout classified as "return of capital." Each distribution returns cash to investors, but this is primarily a return of principal rather than investment profits. The number of shares remains constant, while the NAV steadily declines over time.

Robinhood's contracts address this by decoupling "shares" from "tokens." The holder's share count remains the same, but an internal multiplier adjusts the reported token supply downward as return of capital accumulates, reflecting the erosion of the underlying NAV.

However, data platforms following the standard ERC-20 model simply add up mints and burns. This approach fails to capture this re-basing adjustment, overestimating the circulating token supply and thus the reported market cap.

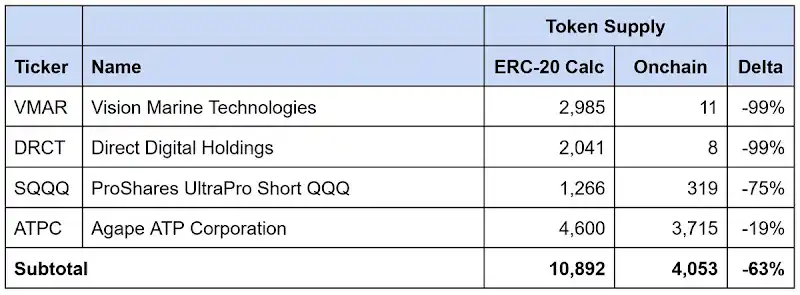

Reverse Stock Splits

Data as of January 23, 2026

The same issue arises with reverse stock splits. Reverse splits increase the per-share price by consolidating shares, often to meet exchange listing requirements. The number of shares is reduced proportionally, but the price per share increases proportionally, leaving the total value unchanged.

Again, Robinhood's contracts adjust the token supply to reflect the reverse split, while third-party platforms following the standard ERC-20 model overestimate the circulating supply and reported market cap.

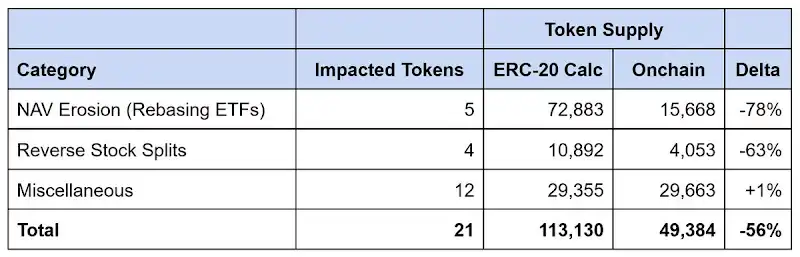

Total Robinhood Data Discrepancy

Data as of January 23, 2026

Among the 21 tokens we identified with data mismatches, the reported supply was overestimated by approximately 64,000 tokens, a discrepancy of up to 56%. NAV erosion from high-yield ETFs accounted for about 90% of this gap, with reverse stock splits explaining the remainder.

Any data platform relying on standard ERC-20 logic to calculate supply will severely overestimate the market cap of Robinhood's tokenized stocks, often by multiples.

The Solution

Tokenized Stock Taxonomy: Models & Infrastructure

Tokenized stock issuers have taken different approaches to handling corporate actions. They can be broadly categorized into two types.

Rebasing Models

Rebasing models maintain现货价格平价 (spot price parity): meaning 1 token should always trade close to the price of 1 underlying share. When a corporate action occurs, token balances are automatically adjusted to maintain this relationship. Issuers using this method fall into two camps based on their relationship with the underlying asset issuer:

- Rebasing (Third-Party): The issuer operates independently of the company whose stock is tokenized. Both xStocks (@xStocksFi, under Backed Finance / Kraken) and Robinhood (@RobinhoodApp) take this approach. Tokens are backed by custodied shares, but due to no direct relationship with the underlying issuer, they replicate economic exposure without conferring legal ownership.

- Rebasing (Direct): The issuer partners with the public company to tokenize its shares. Superstate's Opening Bell (@SuperstateInc) and Securitize (@Securitize) operate as SEC-registered transfer agents and serve as the official shareholder registry. Because tokens are issued in coordination with the company, the tokens themselves are the legal securities, affording holders actual shareholder rights not available in the third-party model.

Both structures require multiplier infrastructure to reflect corporate actions on-chain.

Solana's Token-2022 standard natively provides a scaling UI amount extension. The issuer simply updates a multiplier, which then adjusts the balance displayed in the user interface without changing the raw token amount. For example, a 2-for-1 stock split changes the multiplier from 1.0 to 2.0; wallets显示 double the balance, while the underlying raw token count remains unchanged. As the standard is native to Solana, data platforms can directly query for multiplier changes.

EVM networks currently lack an equivalent standard. Issuers like xStocks and Robinhood have had to build their own multiplier mechanisms. While balances adjust correctly and wallets display prices consistent with the spot price, these implementations are bespoke. Third parties relying on standard ERC-20 calls cannot detect when the multiplier changes or query its current value. Therefore, each issuer's specific implementation must be understood separately.

This is why Chris Ridmann of Superstate and Gilbert Shih of Robinhood co-drafted ERC-8056, a proposed draft standard aiming to introduce a standardized "Scaling UI Amount Extension" for ERC-20 tokens. This would provide data platforms with a unified interface for tracking corporate actions across issuers.