Source: Fintech Blueprint

Original Title: Analysis: Learning from 2025 to win big in the 2026 machine economy

Compiled and Edited by: BitpushNews

Structural Issues in the Crypto Market

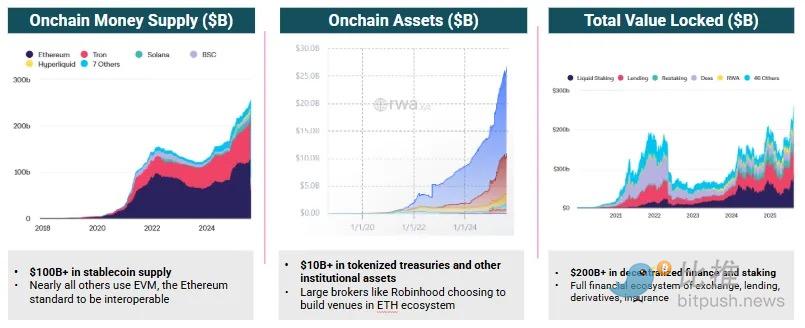

Adoption of on-chain financial instruments and the machine economy trend are booming.

Over the past year, we have seen massive expansion in blockchain-native finance across these five dimensions: (1) stablecoins, (2) decentralized lending and trading, (3) perpetual contracts, (4) prediction markets, and (5) Digital Asset Treasuries (DATs). The regulatory environment in the U.S. has become extremely favorable, driving up both project numbers and risk appetite.

Putting aside uncertainties from tariffs and market structure, a forgiving macro environment has also provided fertile ground for crypto innovation to take root. These trends are well-known and don't require further data elaboration.

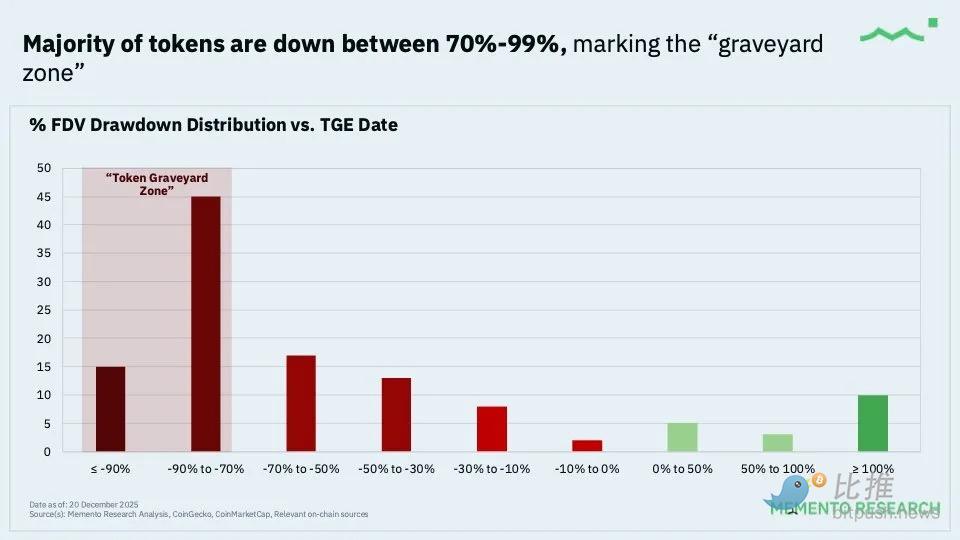

However, 2025 has been an extremely difficult year for long-term investors in tokens and crypto assets other than Bitcoin.

If you were a trader or banker, you might have done alright—we saw record commissions for bringing DATs to market, and massive fee income for exchanges like Binance from their listing processes.

But for those of us with a 3-5 year investment horizon, the market structure has been terrible.

We are completely stuck in a kind of 'negative prisoner's dilemma': token holders, anticipating future selling pressure, sell any and all assets; while market makers and exchanges that support the entire crypto economy take speculative positions focused solely on short-term gains. Token unlock mechanisms and issuance prices often drag projects down before they have achieved profitability or found product-market fit.

Furthermore, the market structural failure on October 10th clearly hit several major players hard, although the losses have not been made public, and the清算 aftermath continues. The correlation between all crypto assets has risen to near 1, indicating industry-wide participant deleveraging, despite their vastly different fundamental logics.

It is easy to retreat and become cynical at this moment.

But we prefer to 'mark-to-market' as clearly as possible in order to plan for future positioning.

The decline in the crypto investment space in 2025 is information, but not the final word. It is likely that 2026 will see large-scale liquidations in the secondary market for private companies, at which point we will analyze how so many Special Purpose Vehicles (SPVs) were issued at high valuations during the crypto boom.

Meanwhile, the vision of programmable finance and 'Robot Money' continues to materialize, and we must continue to work hard to find the best positioning in its inevitable rise.

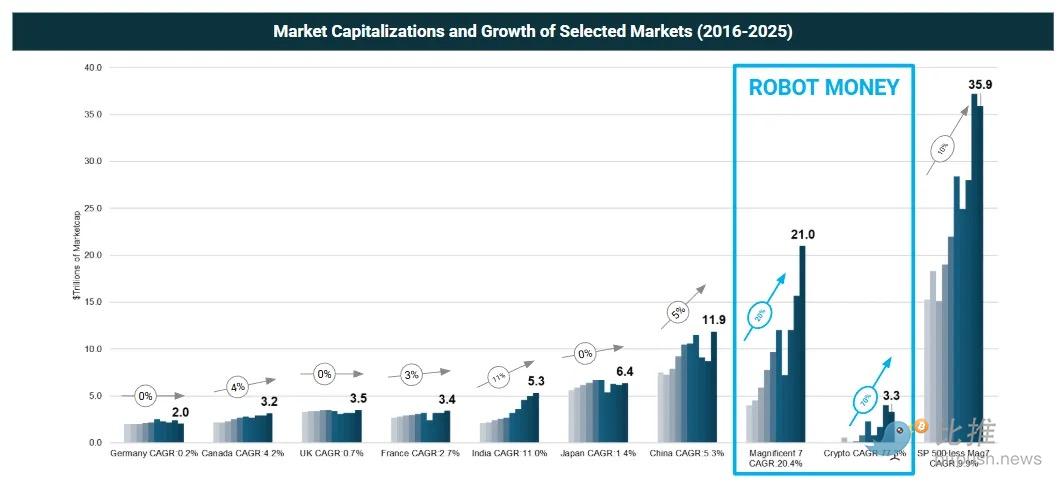

For context, see the chart below. This chart, zoomed out over the past decade, shows市值 creation across several regions and industries.

When we look at this history, the value creation in the cryptocurrency and AI fields is staggering compared to the rest of the world.

European capital markets (~$2-3 trillion per country) have achieved almost nothing, merely maintaining the status quo. You might as well invest in government bonds and earn 3% interest per year, which might create more value. On the right side of the chart, India and China show a 5-10% compound annual growth rate (CAGR), with net market cap growth of approximately $3 trillion and $5 trillion respectively over the same period.

Understanding this scale, look again at what we define as 'Robot Money':

(1) The US 'Magnificent 7' representing tech and AI added about $17 trillion in market cap at a rate of 20% per year;

(2) The crypto asset market, representing modern financial rails, added $3 trillion over the same period, with a staggering 70% CAGR.

This is the future financial center.

But being logically correct is not enough. We must深入细致地 lock onto the parts of the value chain that have not yet been noticed by the world. Think back to talking about robo-advisors in 2009, neobanks in 2011, or DeFi in 2017—the vocabulary and associations were not yet formed at the time, and it wasn't until 2-5 years later that these outcomes hardened into clear business opportunities.

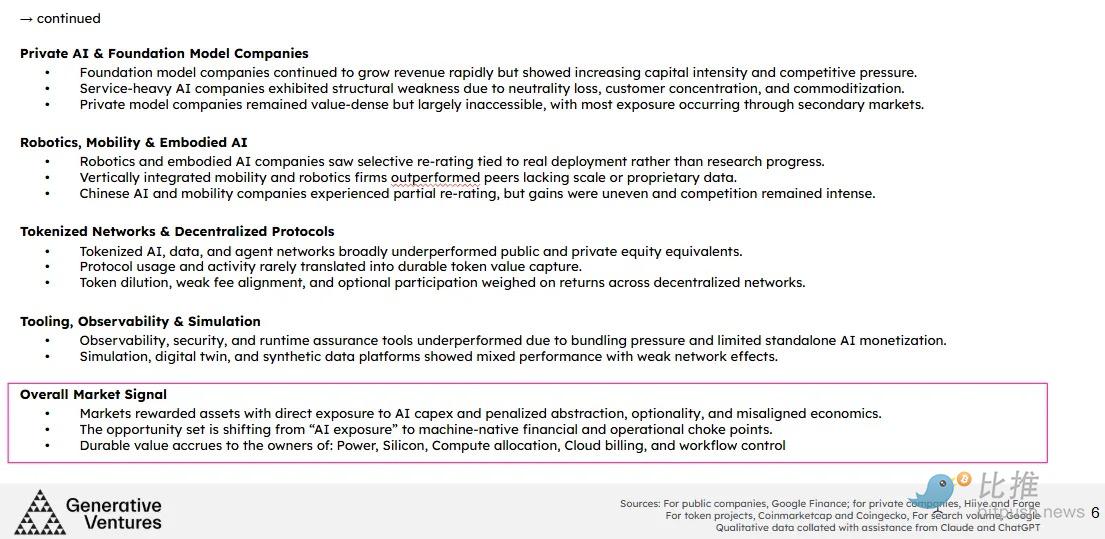

Value Capture in the Machine Economy

As a form of 'masochistic' exercise, we compiled a 158-page summary report covering the most relevant players in the 2025 machine economy.

In public markets, 2025 was a year of 'the strong getting stronger, the weak falling behind'.

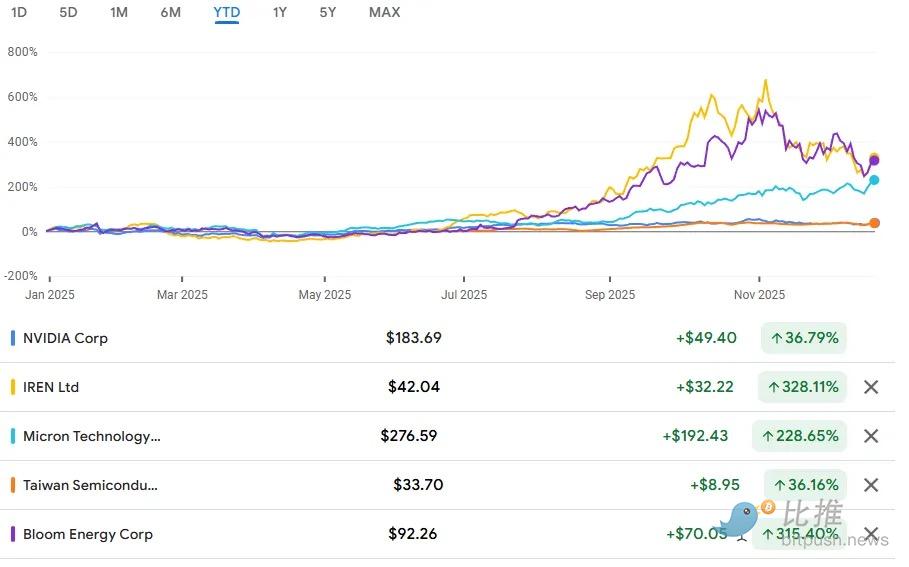

The clear winners were the owners of physical and financial bottlenecks: electricity, semiconductors, and scarce compute power.

Bloom Energy, IREN, Micron, TSMC, and NVIDIA all significantly outperformed the broader market, as capital chases assets that 'machines must pass through'.

Bloom and IREN are typical examples: they stand directly in the path of AI capital expenditure, converting urgency into revenue.

In contrast, traditional infrastructure like Equinix performed sluggishly, reflecting the market's view that the value of general-purpose capacity is far lower than that of power-guaranteed, high-density customized compute.

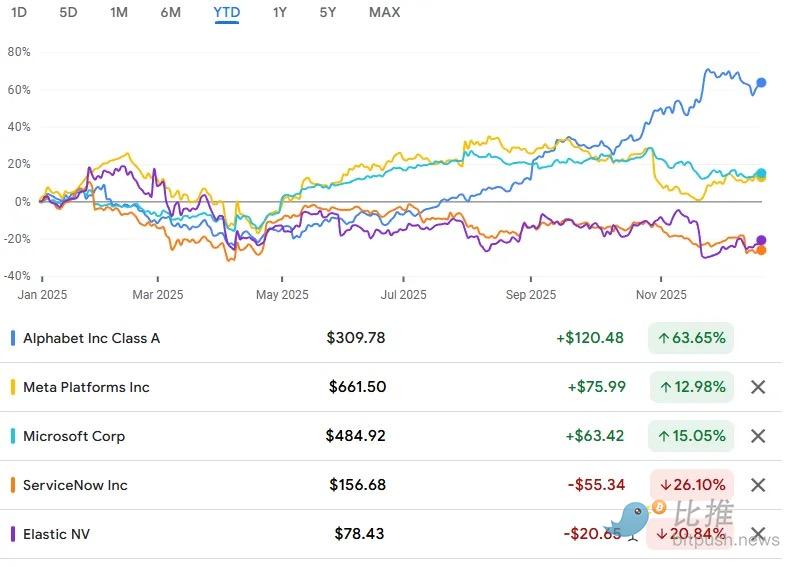

In the software and data领域, performance diverged along another dimension: (1) Mandatory vs. (2) Optional. Platform-like enterprise systems embedded in workflows with mandatory renewals (like Alphabet, Meta) continued compound growth, both rising year-to-date, as AI spending reinforced their existing distribution moats. ServiceNow and Datadog, despite strong products, saw returns dragged down by valuation pressure, bundling pressure from hyperscale cloud providers, and slower AI monetization. Elastic illustrates the不利 case: strong technical capabilities, but squeezed by cloud-native alternatives, with unit economics deteriorating.

The private market also shows a similar screening mechanism.

Foundation model companies are the protagonists of the story, but fragility is increasing. OpenAI and Anthropic have rapid revenue growth, but their neutrality, capital intensity, and margin compression are now clear risks. Scale AI is this year's cautionary tale: a partial acquisition by Meta destroyed its 'neutral' status and triggered customer churn, proving how quickly a heavy-service business model can unravel once trust is broken. In contrast, companies that control value (Applied Intuition, Anduril, Samsara, and emerging fleet operating systems) appear better positioned, even if value realization mostly remains private.

Tokenized networks were the worst-performing sector.

With very few exceptions, decentralized data, storage, agent, and automation protocols performed poorly, as usage failed to translate into token value capture.

Chainlink remains strategically important, but struggles to align protocol revenue with token economics; Bittensor is the biggest bet in crypto AI, but does not yet pose a substantive threat to Web2 lab companies; Giza and similar agent protocols show real activity, but remain trapped by dilution and meager fees. The market no longer rewards 'collaborative narratives' without mandatory fee mechanisms.

Value is accumulating where machines are already paying—for electricity, silicon, compute contracts, cloud bills, and regulated balance sheets—not where they might choose to pay someday in the future.

In 2025, the market rewarded ownership of 'chokepoints' and punished projects with ideals but lacking control over cash flow or compute power. The future core lies in: identifying where economic power already exists, and betting on assets that machines cannot bypass.

Key Revelations:

-

AI value realization is 'one layer deeper' than most people anticipated.

-

Neutrality is now a first-class economic asset (refer to Scale AI).

-

'Platforms' only work when combined with control points, not just as a feature.

-

AI software is deflationary (pricing pressure); AI infrastructure is inflationary.

-

Vertical integration only matters if it can lock in data or economic effects.

-

Token networks are repeatedly experiencing the same market structure tests.

-

Simply having AI exposure is not enough, positioning quality determines everything.

Robotics hardware and software will be the next hype cycle, and we will likely see a similar investment wave and selective winners.

2026 Positioning

Over the past two years, we have built a core portfolio covering the key themes discussed here. Looking ahead to 2026, our positioning and investment execution will be further strengthened.

Next, I will talk about our holding strategy.

Although the long-term vision of autonomous agents, robotics, and machine-native finance is directionally correct, the market is currently in a phase of extremely离谱 valuations in the private AI and robotics space. Aggressive secondary liquidity and implied valuations above $100 billion mark a transition from the 'discovery phase' to the 'exit phase'.

As an early-stage fund with a fintech angle, we must lock onto targets downstream of this spending:

-

Machine Transaction Surfaces: Layers where machines or their operators already carry economic activity, such as payments, billing, metering, routing, and the orchestration of capital or compute, compliance, custody, and settlement primitives. Returns are earned through transaction volume, acquisition, or regulatory status, not speculative narratives. Walapay and Nevermined in our portfolio are examples.

-

Applied Infrastructure With Budgets: Infrastructure that enterprises or platforms are already procuring, such as compute aggregation and optimization, data services embedded in workflows, tools with recurring spend and switching costs. The focus is on ownership of budgets and depth of integration. Examples include Yotta Labs and Exabits.

-

High-Novelty Opportunities: A few asymmetric upside opportunities with uncertain timing: basic research, frontier science, AI-related culture or IP platforms. Our recent investment in Netholabs (a lab dedicated to simulating the complete digital brain of a mouse) fits this characteristic.

Additionally, until the token market structure issues are resolved, we will invest more actively in equity. Previously, our exposure was 40% tokens and 40% equity, with 20% flexible allocation. We believe the token space needs 12-24 months to digest the current difficulties.

Key Takeaways

You don't need to be a venture capitalist to learn from and benefit from this market dynamic.

Massive capital expenditure is flowing from tech giants to energy and component suppliers. A handful of companies are expected to be the multi-trillion-dollar public market winners, but they choose to remain private while spinning off Special Purpose Vehicles (SPVs). Public companies are doing their best to defend. Political power is centralizing and nationalizing these initiatives—whether it's Musk and Trump, or China and DeepSeek—rather than supporting their decentralized alternatives in Web3. Robotics is intertwined with national manufacturing and the military-industrial complex.

In the creative industries (from games to film, music), there is resistance to AI, with people engaged in 'human crafts'排斥 those robots that pretend to do the same thing.

Whereas in the software, science, and mathematics industries, people see AI as a great achievement that can help discover and build efficient business architectures.

We need to stop believing this collective illusion and return to reality. On one hand, dozens of companies have achieved over $100 million in annual revenue by serving users; on the other hand, the market is also filled with大量 falsehoods and scams. Both are true, existing in parallel.

The new year will bring a comprehensive reshuffle, but also contains huge opportunities. Success can only be achieved by walking cautiously on the tightrope of opportunity. Let's meet again on the other side!

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush