Author: Bocai Bocai

DeFi lending has been around for nearly a decade, but the main narrative has essentially been one:floating-rate money markets.

From Aave and Compound to Morpho Blue, interest rates have always been "passively discovered" by utilization.

In May 2026, Morpho released the Midnight whitepaper. It aims to fill the missing piece on this main narrative—fixed rates, fixed terms.

Don't underestimate these two terms.

Fixed income (bonds, notes, credit) is an asset class with a global volume exceeding the stock market, and its entire pricing and risk control logic—predictable funding costs, duration management, a referenceable yield curve—is all built upon "fixed rates and clear terms."

Despite years of on-chain lending, it has remained stuck in floating-rate, perpetual money markets:unable to provide the certainty institutions demand or grow a proper yield curve.

This is precisely one of the structural barriers preventing large-scale adoption of genuine institutional capital and trillion-dollar RWAs on-chain. In other words,Midnight isn't just adding a feature; it's supplying the missing foundational syntax for on-chain credit to connect with the traditional fixed-income market.

This may sound like just "another option," but its real implication is: on-chain credit, for the first time, has a complete language to move from 『money markets』 to 『fixed-income markets』.

I. What is Midnight

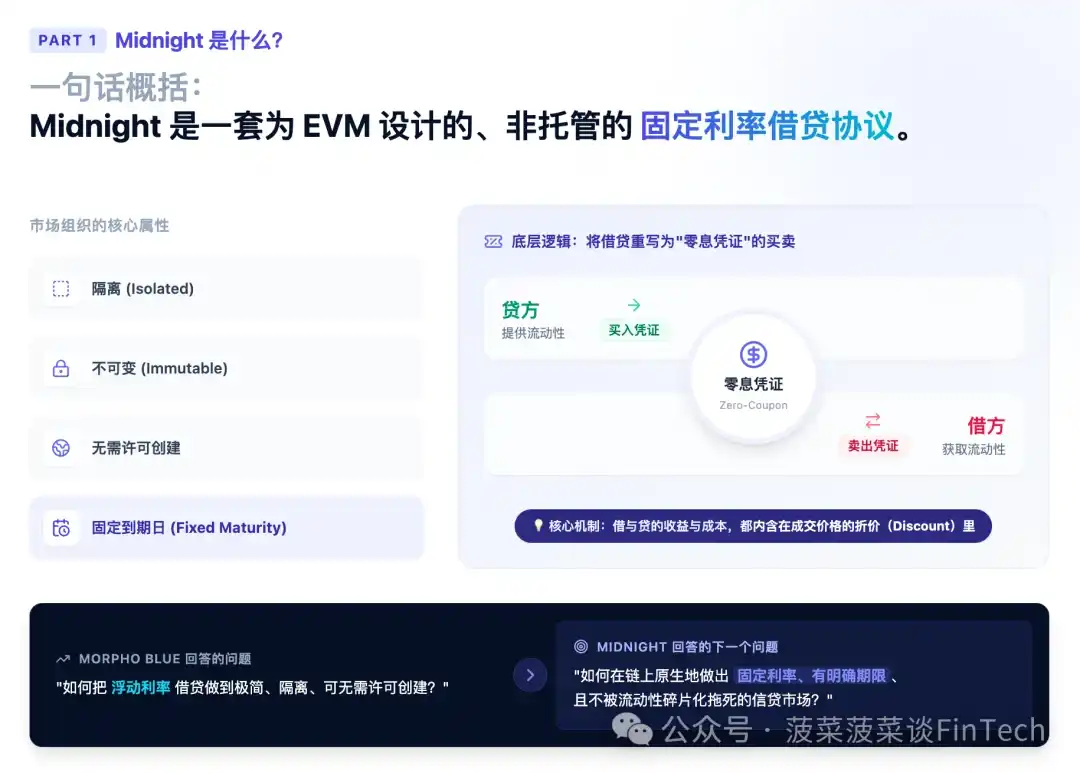

In one sentence:Midnight is a non-custodial, fixed-rate lending protocol designed for EVM.

It is organized around isolated, immutable, permissionlessly creatable markets with fixed maturities,rewriting lending and borrowing as the buying and selling of a "zero-coupon certificate"—lenders buy certificates, borrowers sell certificates, with both parties' returns and costs embedded in the discount of the transaction price.

If Morpho Blue answered "how to make floating-rate lending minimal, isolated, and permissionlessly creatable," then Midnight answers the next question: how to natively implement fixed-rate, definite-term credit markets on-chain without being dragged down by liquidity fragmentation.

Below, we trace the evolutionary thread of Morpho to fully unpack the logic behind this design.

II. From Aave to Blue to Midnight: A Clear Evolutionary Thread

To understand Midnight's design trade-offs, one must first see which thread it stands on.

First Generation: Pooled + Floating Rate (Aave / Compound):

Early lending protocols emerged in an environment of scarce, passive on-chain liquidity and high transaction costs. Under those constraints, pooling all users into a unified, freely enterable/exitable liquidity pool was the optimal solution for maximizing liquidity concentration.

The cost was: the protocol had to make decisions for everyone—not just settlement and accounting, but also critical pricing and risk parameters. This design worked well when user preferences were highly homogeneous. But as the range of assets, users, and credit scenarios expanded, and risk/liquidity/compliance preferences began to diverge, a single pool could not accommodate multiple risk profiles without fragmenting liquidity.

Second Generation: Morpho Blue—Minimal Core + Curation Layer:

Blue proposed a different architecture: based on isolated, immutable, permissionlessly creatable markets. The protocol itself makes no judgment about "which assets deserve credit" or "how capital should be allocated"; these decisions are deliberately left to lenders—they create and choose markets matching their needs.

In practice, most supply comes from vaults built on top of the protocol. Thus, the market layer remains extremely thin, while curation and capital allocation become a fully competitive layer above the protocol. This is the core philosophy of Morpho: the kernel should be as small as possible, complexity pushed up to a competitive outer layer.

Third Generation: Midnight—Bringing Fixed Rates and Terms On-Chain:

Pooled architecture and floating rates are a natural pair: a pool's utilization is adjusted by the interest rate model (IRM), and in turn, rates are "discovered" through utilization. This mechanism is simple but carries several structural costs.

Midnight inherits all of Blue's DNA—markets are still isolated, immutable, permissionlessly creatable, serving as trustless primitives for building independent products and serving different jurisdictional scenarios—but swaps the rate mechanism for fixed rates and introduces fixed maturities and offer-based matching.

Understanding this thread reveals that Midnight is not a random new creation, but a natural extension of Morpho's philosophy of "pushing decision-making from the protocol layer continuously to the market/curation layer": Blue gave rates/allocation back to the market; Midnight goes further by giving "rate discovery" itself back to market offers.

III. Why Fixed Rates + Terms?—Explaining the Underlying Motivation

Many ask: floating rates work fine, why go through so much trouble for fixed rates? Because floating rates have several unavoidable structural issues:

First, interest rate risk is a direct barrier for borrowers.

For borrowers needing predictable funding costs—such as institutions matching on-chain credit with off-chain fixed-income liabilities, RWA borrowers—floating rates themselves are a hurdle.Funding costs fluctuate with utilization, making cash flow matching impossible.

Second, floating rates make it hard to cold-start new credit scenarios.

In small markets, moderate capital inflows/outflows can drastically shift utilization, pushing rates to extremes.This volatility makes it hard for new markets to establish stable expectations.

Third, lenders are forced to constantly monitor.

To keep their allocation aligned with risk-return preferences, lenders must watch utilization changes and adjust positions.

Fixed rates naturally resolve these limitations.

They decouple rates from utilization: rates are no longer a function of utilization but the result of direct offers between buyers and sellers. Borrowers get certain funding costs, lenders get certain maturity yields; neither needs to revolve around a utilization curve.

Fixed rates have been explored in DeFi (e.g., Yield Protocol) but never became a universal base for on-chain lending—that's precisely what Midnight aims to do.

And fixed maturity is the twin prerequisite for fixed rates. Only when positions have a clear maturity date does "borrowing/lending at a certain rate for a certain term" make sense; multiple markets with different maturities form a term structure, i.e., the on-chain version of a yield curve.

IV. Markets and Units: Rewriting Lending as "Trading Zero-Coupon Certificates"

This is the key to understanding all Midnight mechanisms.

4.1 Market Composition

Midnight is organized around isolated, immutable term markets; configurations are immutable once created. Each market specifies three things:

A loan token; a maturity date; a set of acceptable collateral assets and their respective parameters (single or multiple).

4.2 Rewriting Lending with "Units"

Positions within a market are measured in "units," with extremely clean logic:

One debt unit = an obligation to repay one unit of the loan token before maturity;

One credit unit = a claim on those repaid assets.

Thus: Buying units → increases your credit (you become a lender); Selling units → increases your debt (you become a borrower). Interest doesn't need separate setting; it's embedded in the transaction discount. For any transaction price P > 0, the simple interest for the remaining term is:

r = 1 / P − 1

Example: You buy a unit at price 0.95. At maturity, it redeems for 1 unit of loan token, so the return over this remaining term is 1/0.95 − 1 ≈ 5.26%. This is exactly the pricing logic of zero-coupon bonds/T-bills—buy at a discount, redeem at face value, all return in the discount. Midnight completely translates "lending" into "buying and selling zero-coupon certificates," which is the fundamental reason it can express fixed rates so simply: an interest rate is, at its core, a price.

4.3 Fungibility and "Fixed Calendar Maturity": Why Liquidity Doesn't Fragment

This is an easily overlooked but critical design point.

Every trade has a buyer and seller, but the result is a fungible position at the market level, not an ongoing bilateral relationship between the two parties. Credit and debt are accounted at the market level; positions aren't tied to the specific trade that created them. Even better: markets mature on fixed calendar dates, not on a rolling term from the open time. This means—positions opened at different times but with the same maturity date belong to the same market and are completely fungible.

Why is this important?

Because in an isolated market architecture, liquidity's biggest enemy is fragmentation: if each loan creates its own snowflake-like independent instrument based on "open date + term," then even if everyone wants a "90-day" term, capital would be split into countless isolated pools.

Fixed calendar maturity cuts this problem at the root: a "matures on Dec 31" position entered today and one entered yesterday with the same maturity are the same thing; they can trade with each other, offset each other. Thus, liquidity aggregates on the "maturity date" dimension, not scattered by open time.

4.4 Early Exit: Four Trading Scenarios

Since credit and debt are fungible within a market, both lenders and borrowers can reduce their positions early: lenders sell units to reduce credit, borrowers buy units to reduce debt.

The rules have a clean priority—buyers first close their debt before accumulating credit; sellers first close their credit before accumulating debt.

Thus, a trade (buyer ↔ seller), based on each party's initial position, falls into one of four scenarios:

| Seller Increases Debt |

Seller Decreases Credit |

|

| Buyer Increases Credit |

New Debt ↔ New Credit |

New Credit ↔ Seller Closes Credit |

| Buyer Decreases Debt |

Buyer Closes Debt ↔ New Debt |

Buyer Closes Debt ↔ Seller Closes Credit |

Early exit offers users more flexible return curves and, because entry and exit happen within the same unified market, deepens liquidity for all participants.

A detail: Trading is still possible after maturity, with the sole exception that new debt cannot be added after maturity (i.e., the two "Seller Increases Debt" scenarios in the table are prohibited). Allowing post-maturity trading enables closing positions even when liquidation is unprofitable.

V. Offer Mechanism: Midnight's True Innovative Core

If the previous section was "rewriting lending as unit trading," this section is "how to make these units trade efficiently with minimal capital cost." Midnight's answer here distinguishes it from all existing designs.

5.1 Offer: Off-Chain Quotes Without Locked Capital

Market makers (makers) express "I am willing to trade up to a certain size in a certain market at a certain price" via an offer. Note two key points:

- Offers are not broadcast at the protocol layer; they can be distributed via any off-chain or on-channel—the protocol does not maintain an order book.

- An offer itself locks no capital; it is merely an executable intent with a price and size limit.

Takers execute the offer by submitting it to the Midnight contract. Execution can be partial: any size not exceeding the offer's remaining capacity is allowed; an offer can be filled by multiple takers until exhausted. The contract atomically settles against the referenced market—creating, transferring, or destroying corresponding credit/debt units as needed.

Each offer includes a ratifier (approval contract) with embedded verification logic called when the offer is taken. Typically, it verifies a signature by the maker's public key.

This modular design allows makers to use different signature schemes (e.g., passkeys, quantum-resistant) or custom verification logic—laying the groundwork for "one signature approving multiple offers."

5.2 Maker Callback: Fetching Capital Only Upon Execution

This is the soul of the entire mechanism.

An offer can specify a callback executed at the moment of fill, allowing the maker to source the required capital or collateral only when the offer is taken, without preparing the position in advance.

This means: makers can keep the capital backing these offers earning yield elsewhere until the offer is taken.

The whitepaper gives a straightforward example: A lender can keep funds earning yield in a Morpho Blue market while posting a fixed-rate offer on Midnight; once the offer is taken, the callback within the same transaction withdraws the funds from Blue and completes settlement (assuming sufficient liquidity).

Callbacks are also extremely useful for rolling term exposures. A borrower nearing maturity can use a callback to buy back/repay debt in the current market and atomically enter a later-maturity market; lenders can similarly roll credit exposure from one maturity to another, all without first withdrawing idle balances.

5.3 Multi-Market Quotes, Consumption Groups & Merkle Roots: Quoting the Entire Market with One Pool of Capital

Callbacks enable a stronger capability: a maker can use the same pool of liquidity to post multiple offers covering multiple markets simultaneously—a key weapon against liquidity fragmentation.

But an obvious risk arises: if 10 ETH backs three offers of 10 ETH each in markets A, B, and C, could it be filled for 30 ETH?

Of course not.

Midnight solves this with consumption groups:

- Multiple offers belonging to the same consumption group share a fill budget.

- Executing any offer within the group deducts from the remaining budget for all offers in the group.

- Once the budget is exhausted, no offer in the group can be filled further.

Thus, the maker's real exposure is constrained by the budget, not the sum of all signed offer sizes.

An intuitive example from the whitepaper:

A lender has 10 ETH, posts Offer 1/2/3 for markets A/B/C respectively, all sharing a 10 ETH budget. A borrower first fills 3 ETH from market B, budget drops to 7, consumed is 3; another borrower then fills 7 ETH from market A, budget hits zero, consumed is 10—now all three offers are invalid.

One pool of capital, quoting the entire market, exposure controlled.

To make this efficient at scale, a ratifier can support approval of a Merkle root for a set of offers: a maker can use one signature/one interaction to post many offers across many markets; these offers can later be taken by presenting the corresponding Merkle proof.

Signature efficiency + capital efficiency, both unlocked.

Connecting 5.1–5.3 reveals that Midnight essentially eliminates the implicit cost of "posting an order locks capital" in traditional order books.

In traditional designs, providing conditional liquidity ("I'll trade only at a certain rate, within a certain size") requires locking capital upfront. This pre-commitment has a high opportunity cost under the combinatorial explosion of isolated markets × multiple maturities, resulting in reluctance to post large offers and thin liquidity.

Midnight allows liquidity to exist as "quotes without locked capital," fetching funds only upon execution, enabling markets to function before stable trading volume forms—precisely the antidote to the cold-start problem.

5.4 Routing: Off-Chain Search, Not a Centralized Order Book

The protocol does not enforce a quote queue, but routers will naturally sort offers by price. The problem: the protocol layer does not guarantee the executability of any offer (considering callback success, consumption group exhaustion, gas costs, etc.).

Therefore, a taker seeking the "best executable liquidity" among all posted offers faces a genuine search problem. This process is called routing, occurring outside the protocol—anyone can do it.

This fundamentally distinguishes Midnight from a Central Limit Order Book (CLOB):

The protocol does not maintain a canonical order queue; there is no price-time priority at the protocol layer; the protocol layer does not reserve any capital.

In other words, Midnight, like Blue pushing "curation/allocation" to an outer layer, pushes the complex task of "matching/routing" to a competitive solver/router layer outside the protocol.

The kernel is responsible for only one thing:taking a submitted offer and atomically settling it.

5.5 Tick Sizes: Gridding by Rate, Not Price

Midnight prescribes a minimum tick size for offers—like stocks moving by one cent per tick.

The reasoning is straightforward:if prices could be subdivided infinitely, market makers would undercut each other with negligible price differences to get priority, eventually discouraging large orders and killing liquidity.

The real ingenuity lies in: ticks are divided by "rate," not by price.

Why not equally spaced price ticks?

Because the relationship between price and rate isn't rigidly fixed—the same "1% price discount" translates to a very different annualized rate in a market maturing in one month versus one year. That is, equally spaced price ticks would result in uneven "rate" steps, which is what traders actually care about.

When quoting, people think in rates, not prices.

Thus, Midnight makes the rate difference between adjacent ticks change by a fixed ratio (default 2% per tick), so "moving one tick" corresponds to a consistent perceived rate change regardless of term.

This tick system can also scale from coarse to fine: markets start with a 2% coarse tick; as depth and participation grow, they can tighten to 1% or 0.5%. Here's a clean design detail—finer ticks are a "superset" of coarser ones, so when tightening precision, existing ticks remain valid, and posted offers don't become invalid.

Thus, markets can smoothly increase precision without disrupting existing quotes, much like exchanges setting smaller tick sizes for more liquid stocks.

VI. Liquidation Mechanism: More Lenient for Borrowers, Fairer Loss Distribution

Fixed maturity adds several liquidation scenarios Blue didn't need to consider, making Midnight's mechanism worth explaining clearly.

The overall direction is twofold: be more lenient to borrowers during liquidation, and distribute losses more fairly if they occur. Let's go through the core mechanisms—no formulas, just explaining "what it does" and "why."

6.1 When Can You Be Liquidated

How much you can borrow is determined by the "discounted value" of your collateral: each collateral type is discounted by its own factor (LLTV, Loan-to-Liquidation Value); the sum of all discounted collateral values is your borrowing limit. If debt exceeds this limit, the position becomes "liquidatable."

During liquidation, a third party repays part of your debt and takes the corresponding collateral at a discounted price; the repaid debt returns to the market for lenders to claim.

Notably, each collateral type has its own independent price feed and discount factor, allowing different risk settings within the same market.

6.2 How Much Discount a Liquidator Gets Can Be Adjusted Per Collateral

Liquidators are willing to work because they get collateral below market price—this discount is their reward (liquidation incentive).

Midnight's unique aspect: the discount cap isn't a one-size-fits-all protocol parameter but can be set per market based on collateral characteristics (the whitepaper calls this knob the "liquidation cursor," with loose and tight settings).

The logic is direct: a smaller discount leaves more collateral buffer for the borrower, lowering bad debt risk; a larger discount better incentivizes liquidators to handle hard-to-sell, illiquid collateral.

In contrast, Blue uses the same setting for all markets; Midnight increases the precision of this risk dial.

6.3 Liquidate Only to "Just Healthy," Not the Entire Position

When a position is unhealthy, although liquidatable, the amount a liquidator can repay is capped—only enough to bring the position back to "just healthy," not the entire position at once (this limit is called "restorative close-out").

Why is this especially needed in term markets?

Because in Midnight, borrowers must always have sufficient collateral for the "full amount due at maturity." Allowing a liquidator to close the entire position when it just crosses the line would force the borrower to forfeit collateral for the full debt—even though only part of the term has elapsed, an excessive penalty.

The only exception is a residual position too small: if the remaining collateral after liquidation is too insignificant for further liquidation, a full close-out is allowed to avoid leaving an untidy tail.

6.4 Unpaid at Maturity: Incentive "Ramps Up Slowly," Don't Punish Late Borrowers Excessively

After maturity, rules tighten: as long as any debt remains unpaid, even if the position is technically healthy, it can be liquidated—because lenders should get their money back at maturity.

But this scenario is often just the borrower being "late," not insolvent.

Thus, Midnight doesn't start with the full reward but lets the liquidation incentive ramp from zero to the normal cap over about 15 minutes, like a slow Dutch auction.

This ensures someone will eventually close it out without letting liquidators extract excessive value from a merely tardy borrower. (For "truly insolvent" health-based liquidations, the normal mechanism remains available anytime after maturity; lenders' protection remains intact.)

6.5 Bad Debt Accounting Is More Timely, Blocking "Front-Running the Exit"

If collateral drops so much that even full liquidation cannot cover the debt, the shortfall is bad debt, ultimately borne proportionally by lenders. Bad debt itself isn't new; the key difference is the accounting timing.

Blue waits until collateral is fully exhausted before booking the loss. Thus, a clearly insolvent position might hang there with losses unaccounted—informed lenders could withdraw before the loss is recorded, leaving the hole for the less informed.

Midnight does the opposite: the first time a liquidator acts on that position, the uncovered loss is immediately booked, narrowing the "front-running the exit" window to almost nothing.

Ultimately, this is a fairness fix targeting information asymmetry and front-running.

VII. Access Control & Authorization: Interfaces for Compliance & Institutions

7.1 Gate: Two Types of Optional Gating

Midnight is designed to support flexible access control conditions. When creating a market, up to two optional gate contracts can be specified (fixed thereafter); the protocol calls them when attempting gated operations:The enter gate controls who can establish or increase positions, i.e., who is eligible to start lending or borrowing, typically used for KYC, whitelisting, etc. It has a crucial design constraint:gating only applies to "entering," not "exiting." Even if the gate contract denies access, participants can still withdraw loans, repay debt, retrieve collateral—exit paths are always open. The reason is that a gate is an external contract that may evolve over time or even fail; limiting it to entry ensures it can never lock funds in the market, making it an access filter, not a custody risk.The liquidator gate controls who can execute liquidations, restricting liquidation (and consequent bad debt accounting) to a designated set of entities, e.g., only approved liquidators. For RWA and institutional credit, these two gates are key interfaces for compliance implementation:You can directly build compliant markets like "whitelist-only access" or "specified institutional liquidators only" on the same set of immutable primitive, without rewriting the protocol.

7.2 Authorization: Coarse-Grained, Delegable

Midnight provides a single, coarse-grained authorization primitive:an account can authorize another address to act on its behalf within the protocol, eliminating the need for separate signatures per operation. Common uses include:- Authorizing a keeper to roll over positions at maturity;- Authorizing a router or bundling contract to atomically execute "repay, retrieve collateral, enter new market" in one transaction;- And most typically—lenders depositing funds into a vault contract, which then operates on the protocol uniformly.Note that this authorization is global: once granted, the authorized address gains full control over the authorizer's entire Midnight state, not only to roll positions but also to withdraw collateral, take on new debt, and even add/remove other authorizations. The protocol layer does not provide fine-grained permissions per operation or per market. Therefore, authorized parties should only be fully trusted addresses or contracts whose permissions are constrained by code.This embodies the "granularity lies above the protocol, not within it" philosophy. To grant a third party only partial permissions, the only way is to introduce an intermediary contract: this contract itself holds full protocol-level authorization but exposes only a limited set of interfaces externally.A vault is precisely such an intermediary contract—it has full authority over Midnight, but its code dictates that curators/allocators can only rebalance among whitelisted markets and cannot withdraw funds to their own addresses, and depositors can only deposit/withdraw shares. Thus, the fine-grained logic of "who can do what" resides entirely in the vault code, while the Midnight protocol only needs to recognize "full authority / no authority"—again reflecting Morpho's design philosophy of "minimal kernel, complexity pushed outward."

VIII. New Fee Types: Settlement Fee & Continuous Fee

Midnight can charge at most two types of fees at the protocol layer—settlement fee and continuous fee—both capped by contractually written, non-increasable limits, providing participants with permanent certainty about "the maximum the protocol can charge."

Rates are default set per loan token but can be overridden per market; the roles of setting rates and collecting fees are separate.

The settlement fee is charged per executed trade, manifested as a price spread rather than a separate deduction. A tiny spread is inserted between the buyer's and seller's settlement prices, borne by the party initiating the trade (taker). The fee rate is set piecewise linearly with remaining term but has a hard cap—no matter the configuration, annualized it cannot exceed 50 basis points (0.5%).The continuous fee accrues over time on outstanding loan positions, borne by lenders and settled when lenders reduce their credit (i.e., exit or withdraw). It offers lenders an important protection: the applicable rate is locked in at the moment a loan position is established; subsequent protocol rate increases do not affect existing positions. Its cap is 1% annualized.

IX. What It Means: Observations for Practitioners

After explaining the mechanisms, back to "so what." I believe Midnight's significance can be viewed on several levels:

1. It completes Morpho's vision, pushing on-chain credit from "money markets" toward "fixed-income markets." Blue + vaults gave us isolated, immutable floating-rate markets and a curation layer; Midnight adds the missing primitive of fixed rates, fixed terms. Multiple markets with different maturities form an on-chain native term structure / yield curve.

With this step, on-chain finally has the language to converse with traditional fixed-income markets.

2. Its underlying abstraction essentially brings the microstructure of fixed-income markets on-chain.

Zero-coupon discount pricing, calendar-based maturity, fungible secondary liquidity, offer-based matching, off-chain distribution, off-chain routing, tick grids, maturity-specific liquidation—these structures almost one-to-one correspond to traditional bond/note markets.

But Midnight builds this upon Morpho's "isolated/immutable/permissionlessly creatable" DNA, preserving DeFi's trustlessness and composability while borrowing TradFi's mature experience in market microstructure.

3. "Quotes without locked capital, fetching funds only upon execution" is an underappreciated capital efficiency engine.

For professional market makers, this means the same pool of capital can continue earning yield elsewhere while covering quotes across dozens of markets × multiple maturities, with exposure precisely constrained by consumption group budgets. This directly reduces the opportunity cost of providing conditional liquidity, a genuine solution to liquidity fragmentation and cold-start in an isolated market architecture.

Whoever excels at the off-chain routing/solver layer will capture structural advantages.

4. For RWA and institutional credit, this is almost a tailor-made primitive.

Institutional borrowers need predictable funding costs and clear terms—fixed rates + terms hit the bullseye; RWA assets themselves often have term structures, enabling on-chain credit to perform duration matching.

The enter gate and liquidator gate allow compliance requirements and designated liquidators to be directly embedded into markets. KYC, whitelisting, permissioned markets can all be implemented on the same set of immutable primitives, with the "gate entry, not exit" discipline ensuring gating doesn't become a custody risk.

5. For Curators / Vaults, this opens new product spaces.

Just as an entire curation ecosystem grew on Blue, structured credit products—layered by maturity, yield curve strategies, packaging on-chain fixed income for institutions—can be built on Midnight.

Risk curation also expands: beyond collateral due diligence and parameter setting, it now includes managing term structures, maturity rollovers, post-maturity liquidation paths, and other term-market-specific risk dimensions.