Author: Ignas

Compilation: Plain Talk Blockchain

Original Title: Crypto Truth and Lies: A Review of the 2025 Report Card

A year ago, I wrote "Truth and Lies of the 2025 Crypto Market".

At that time, everyone was sharing higher Bitcoin price targets. I wanted to find a different framework to discover where the public might be wrong and to position myself differently. The goal was simple: to seek out ideas that already existed but were overlooked, disliked, or misunderstood.

Before sharing the 2026 edition, here is a clear review of what truly mattered in 2025. What we got right, what we got wrong, and what we should learn from it. If you don't examine your own thinking, you're not investing, you're guessing.

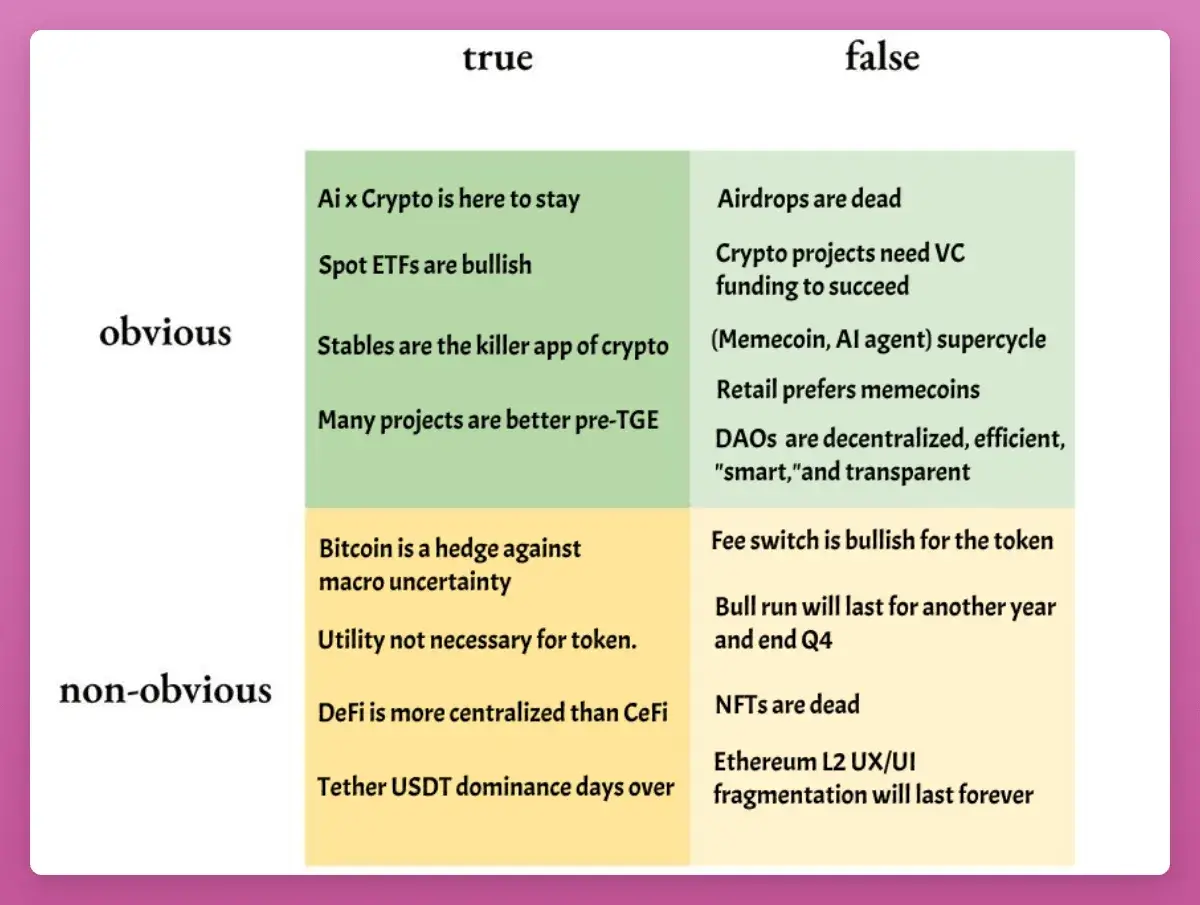

Quick Summary

-

"BTC Peaked in Q4": Most people expected this, but it seemed too good to be true. Turns out they were right, and I was wrong (and paid the price). Unless BTC skyrockets from here and breaks the 4-year cycle pattern, I'll concede this one.

-

"Retail Prefers Memecoins": The truth is, retail doesn't prefer crypto at all. They bought gold, silver, AI stocks, and anything that wasn't cryptocurrency. The supercycle for memecoins or AI Agents also did not materialize.

-

"AI x Crypto Remains Strong": Mixed results. Projects continued to deliver, the x402 standard evolved, and funding continued. But tokens failed to sustain any rallies.

-

"NFTs Are Dead": Yes.

These are easy to review in hindsight. The real insights lie in the following five larger themes.

1. Spot ETFs Are the Floor, Not the Ceiling

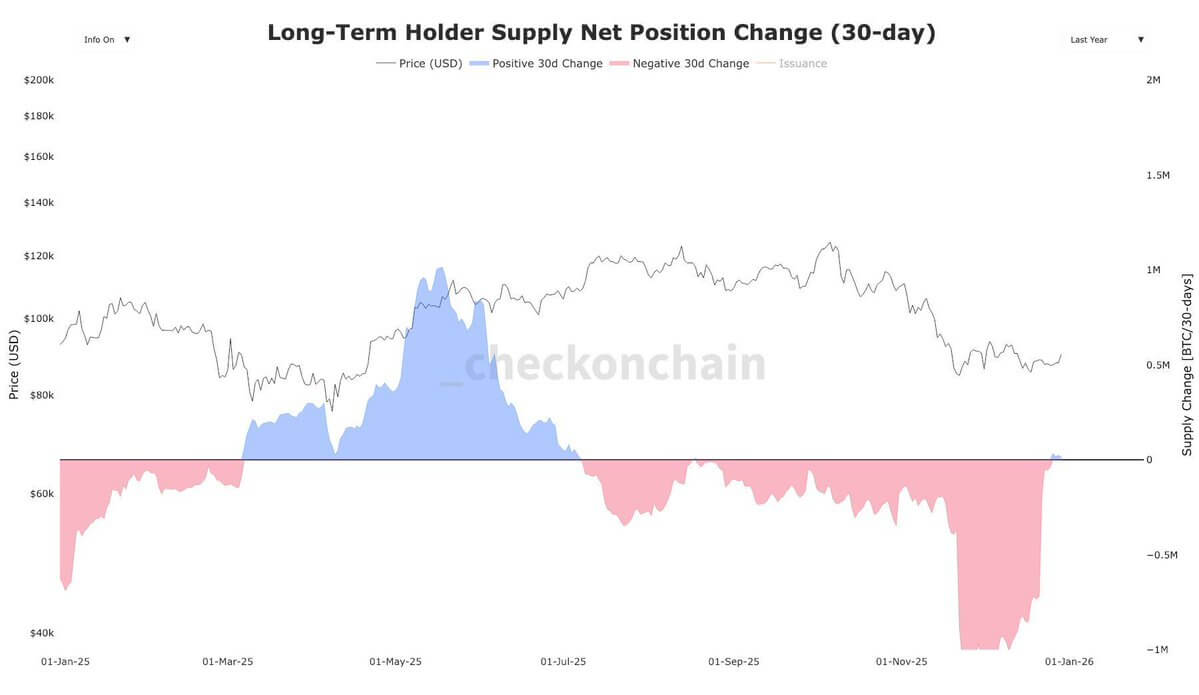

Since March 2024, long-term Bitcoin holders (OGs) have sold approximately 1.4 million BTC, worth about $121.17 billion.

Imagine the bloodbath in the crypto market without ETFs: Despite the decline in price, BTC ETF inflows remained positive ($26.9 billion).

The gap of about $95 billion is precisely why BTC underperformed almost all macro assets. There's nothing wrong with BTC itself; you don't even need to dig deep into unemployment or manufacturing data to explain it—it's just the "great rotation" by whales and "4-year cycle believers".

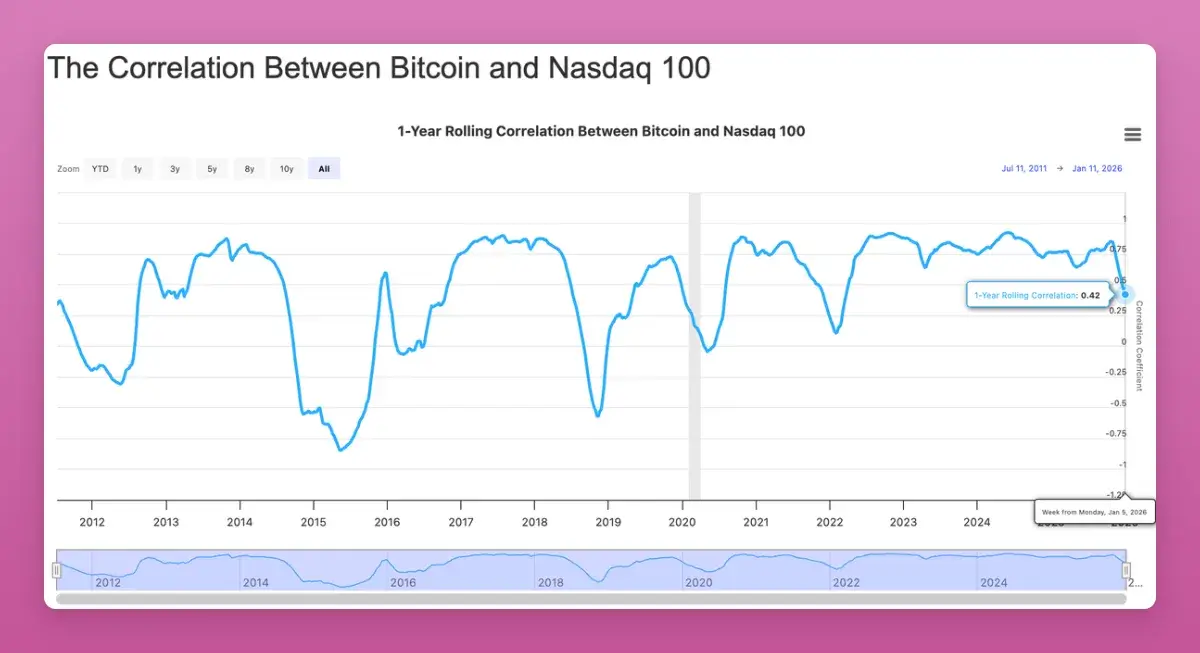

More importantly, Bitcoin's correlation with traditional risk assets like the Nasdaq fell to its lowest since 2022 (-0.42). While everyone hoped for an upward breakout in correlation, in the long run, this is bullish as an uncorrelated portfolio asset sought by institutions.

There are signs the supply shock is over. Therefore, I dare to predict a BTC price of $174,000 for 2026 (equivalent to 10% of gold's market cap).

2. Airdrops Clearly "Did Not" Disappear

The crypto community (CT) once again claimed airdrops were dead. But in 2025, we saw nearly $4.5 billion in large airdrop distributions:

-

Story Protocol (IP): ~$1.4B

-

Berachain (BERA): ~$1.17B

-

Jupiter (JUP): ~$7.91M

-

Animecoin (ANIME): ~$7.11M

The changes are: points fatigue, stronger Sybil detection, and lower valuations. You also need to "claim and sell" to maximize returns.

2026 will be a big year for airdrops, with heavyweights like Polymarket, Metamask, Base(?) preparing to launch tokens. This is not the year to stop clicking buttons, but to stop betting blindly. Airdrop "farming" requires concentrated effort on high-conviction bets.

3. Fee Switches Are Not Price Appreciation Engines, They Are the Floor

My prediction was: Fee switches won't automatically drive token prices up. Most protocols don't generate enough revenue to support their massive market caps.

"The fee switch doesn't affect how high the token can go; it sets a 'floor price'."

Look at the projects ranked by "Holder Revenue" on DeFillama: Except for $HYPE, all high revenue-share tokens outperformed ETH (though ETH is now the benchmark everyone challenges).

The surprise was $UNI. Uniswap finally flipped the switch and even burned $100 million worth of tokens. UNI initially surged 75% but then gave back all its gains.

Three revelations:

Token buybacks set a price floor, not a ceiling.

Everything this cycle is a trade (refer to UNI's pump and dump).

Buybacks are only one side of the story; sell pressure (unlocks) must be considered, as most tokens are still low float.

4. Stablecoins Capture Mindshare, But "Proxy Trading" Is Hard to Monetize

Stablecoins are going mainstream. When I rented a motorbike in Bali, the owner even asked for payment in USDT on TRON.

Although USDT's dominance fell from 67% to 60%, its market cap is still growing. Citibank predicts the stablecoin market cap could reach $1.9 to $4 trillion by 2030.

In 2025, the narrative shifted from "trading" to "payment infrastructure". However, trading the stablecoin narrative wasn't easy: Circle's IPO gave back all its gains after an initial surge, and other proxy assets also underperformed.

One truth of 2025: Everything is just a trade.

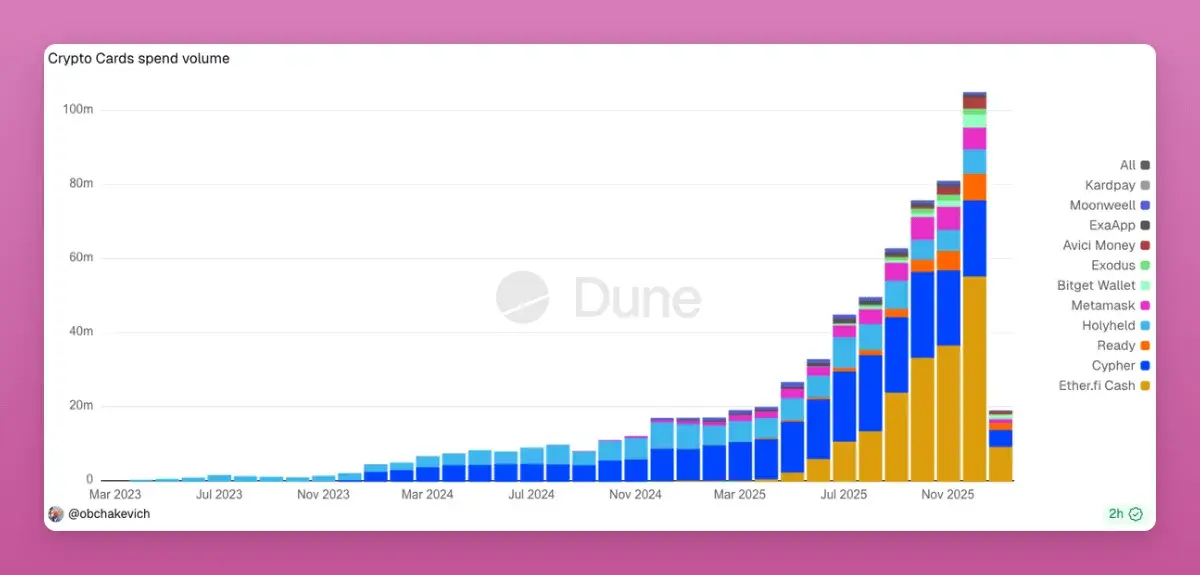

Currently, crypto payment cards are exploding due to their convenience in bypassing strict bank AML requirements. Every card swipe is a transaction on-chain. If direct peer-to-peer payments bypassing Visa/Mastercard emerge in 2026, that would be a 1000x opportunity.

5. DeFi Is More Centralized Than CeFi

This is a bold claim: DeFi's business and TVL concentration is higher than that of traditional finance (CeFi).

Aave commands over 60% of the lending market share (compared to JPMorgan's 12% in the US).

L2 protocols are mostly multi-billion dollar unregulated Multisigs.

Chainlink controls almost all value oracles in DeFi.

In 2025, the conflict between "centralized equity holders" and "token holders/DAO" became apparent. Who truly owns the protocol, IP rights, and revenue streams? The internal dispute at Aave showed that token holders have fewer rights than we thought.

If the "Labs" ultimately win, many DAO tokens will become uninvestable. 2026 will be a crucial year for aligning the interests of equity and token holders.

Summary

2025 proved one thing: Everything is a trade. Exit windows are extremely short. No token has long-term conviction.

As a result, 2025 marked the death of HODL culture, DeFi turned into Onchain Finance, and with improving regulation, DAOs are shedding their "pseudo-decentralized" disguise.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush

Perguntas relacionadas

QWhat was the author's main prediction about Bitcoin's price cycle in 2025, and were they correct?![]()

AThe author predicted that Bitcoin would peak in Q4 of 2025, but they were wrong. The market followed the expected four-year cycle, and the author admitted to paying the price for this incorrect prediction.

QAccording to the article, what was the state of the NFT market in 2025?![]()

AThe article states that NFTs were dead in 2025, confirming the author's previous prediction.

QHow did the performance of tokens with fee switches (like UNI) compare to the author's expectations?![]()

AThe author predicted that fee switches would not automatically drive token prices up but would instead set a price floor. This was confirmed when UNI initially surged 75% after its fee switch was activated but then gave back all its gains, showing that buybacks set a price bottom, not a ceiling.

QWhat significant shift occurred in the stablecoin narrative in 2025?![]()

AThe narrative for stablecoins shifted from 'trading' to 'payment infrastructure' in 2025, as their use for real-world payments grew, exemplified by instances like a Balinese motorbike rental requesting payment in USDT on the TRON network.

QWhy does the author argue that DeFi is more centralized than CeFi?![]()

AThe author argues that DeFi is more centralized due to extreme market concentration: Aave holds over 60% of the lending market share (compared to JPMorgan's 12% in the U.S.), L2 protocols are run by multi-sigs, and Chainlink dominates the oracle market for DeFi.