Author: David, TechFlow Deep Tide

Last Thursday, a new stock appeared on the NYSE with the ticker VCX.

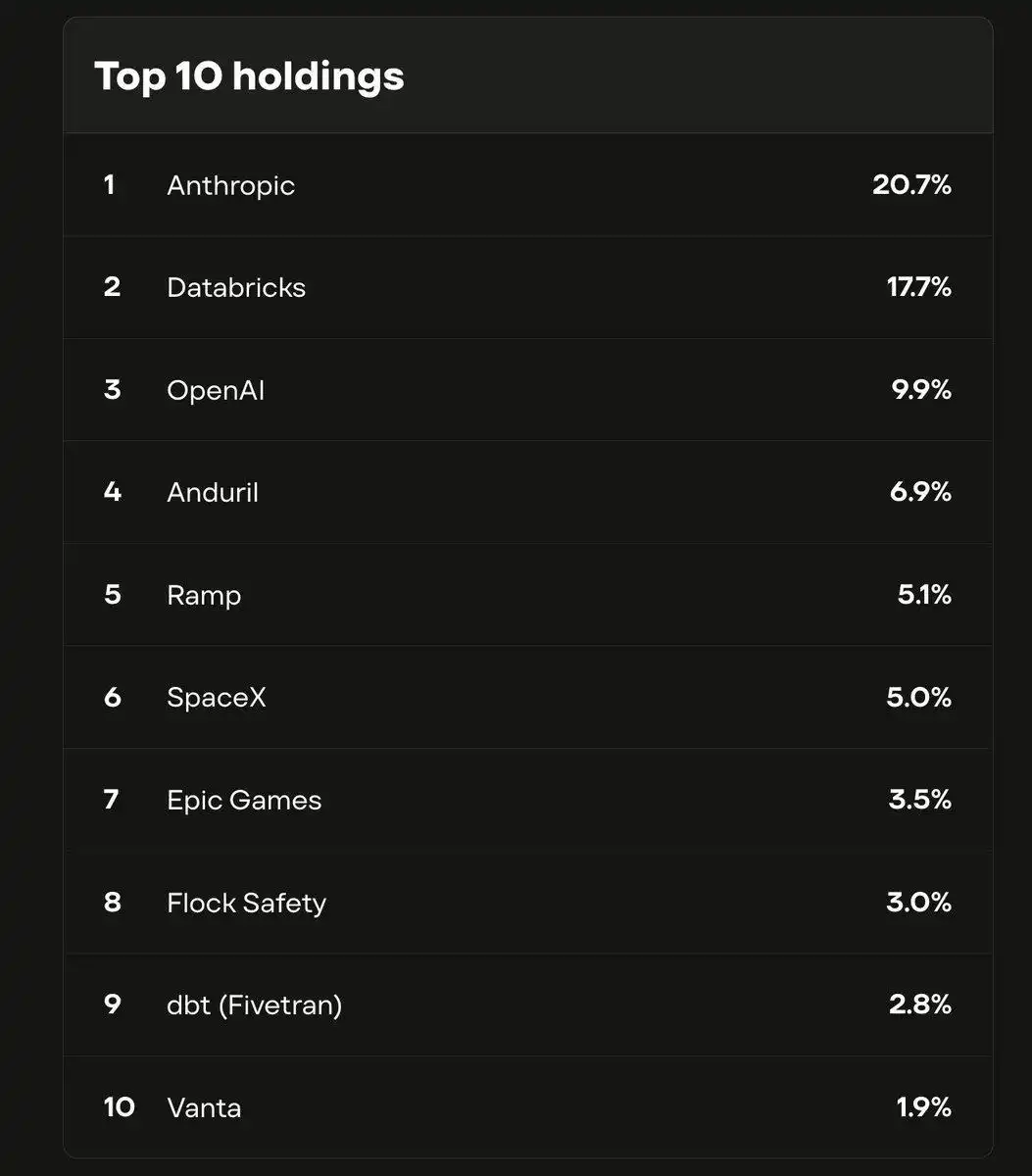

It is actually a fund. The fund holds shares in companies like Anthropic, OpenAI, and SpaceX. Anthropic accounts for 21% and OpenAI for 10%.

These companies have one thing in common: none of them are publicly listed, and ordinary people cannot buy their shares.

VCX is one of the very few vehicles available on the market that allows ordinary investors to indirectly hold shares in Anthropic.

Its net asset value is $19 per share. On the first day of trading, it opened at $42, surged to $125 during the session, and closed at $76. On the fourth trading day, it hit a high of $315 intraday, triggering volatility halts twice.

Four days, from $19 to $315.

Investors are essentially paying 16 times the actual asset value to snap up this fund. Not because the fund manager is exceptionally skilled, but because it contains Anthropic.

A month ago, Anthropic just raised $30 billion at a valuation of $380 billion, making it the second-largest financing round globally this year. Its annualized revenue is $14 billion. But it is not publicly listed, has no stock ticker, and you cannot find it in any brokerage's search box.

If you can't buy the real thing, go for the shadow. VCX is currently the shadow of Anthropic, or rather, the shadow of AI FOMO.

Why is it so expensive?

VCX is not a traditional fund.

With ordinary funds, if you think it's expensive, you can wait for it to drop because the fund manager can issue more shares; supply is elastic. VCX is a closed-end fund. The number of shares was locked at the time of listing and will not increase.

More importantly, the vast majority of shares cannot be sold. Investors who bought before February 20 had their shares locked for six months and cannot trade until September. VCX has over 100,000 investors, but only a very small portion of shares are actually available for trading on the market right now.

What does this mean? Many people want to buy, but very few shares are available to buy. A small amount of buying pressure can twist the price out of shape.

So that 16x premium is essentially pricing "how many people want a piece of Anthropic and how narrow the door is." But this hunger wasn't created by VCX itself.

Chart: Top 10 Holdings of Fundrise's VCX Fund

Over the past decade, a structural change has occurred in the tech industry: the best companies are going public later and later, or not at all.

When Facebook went public in 2012, its valuation was $104 billion, which was an astronomical figure at the time. Today, Anthropic's private valuation is more than three times that of Facebook's IPO, but it previously had no clear plans to go public;

OpenAI is valued at $500 billion and is also not public. News about SpaceX preparing for an IPO has been circulating for over a year, with no confirmed date yet.

A decade ago, a company of this size would have long since rung the bell on the NYSE. Now they don't need to. The private market can provide almost unlimited capital, without the pressure of quarterly reports or dealing with retail investors and short sellers.

For founders, this is a rational choice. For ordinary investors, it means that the fastest-growing companies in history are behind a glass wall, out of reach.

VCX was originally scheduled to list on March 9 but was delayed for ten days due to the Iran war. In those ten days, nothing changed—Anthropic's price didn't go up or down, the fund's holdings didn't change a single share. But the delay itself brewed another ten days of anticipation.

When it finally listed, all the pent-up demand from those ten days squeezed through an extremely narrow passage.

Not all shadows are valuable

There are more ways to gain exposure to shares of unlisted companies than just the VCX fund.

But before discussing these avenues, there's a more fundamental question: Anthropic isn't public, so how did a publicly traded fund get its shares?

The answer is the back door.

Large private companies do a funding round every few months, from Series A to Series G, each time letting new investors in. Anthropic just closed a $30 billion Series G last month, with a long list of participating institutions from GIC to Sequoia to Goldman Sachs. These rounds are usually only open to institutional investors, with minimums often starting in the tens of millions of dollars.

But there is a second path.

Just because a company isn't public doesn't mean its shares can't be traded privately. Early employees and angel investors hold shares, and some of them want to cash out early. This creates a secondary market for private companies—not public, not transparent, but real trades happen.

Fundrise started buying on these two paths back in 2022, when valuations of private tech companies had just experienced a crash and prices were cheap. Over four years, they accumulated a portfolio including Anthropic, OpenAI, and SpaceX. Then they packaged it into VCX, listed it on the NYSE, and now ordinary people can buy it like a stock.

In the same month, at least three similar funds were trading on the NYSE, all selling the same concept:

Selling you, through the front door, what was bought through the back door.

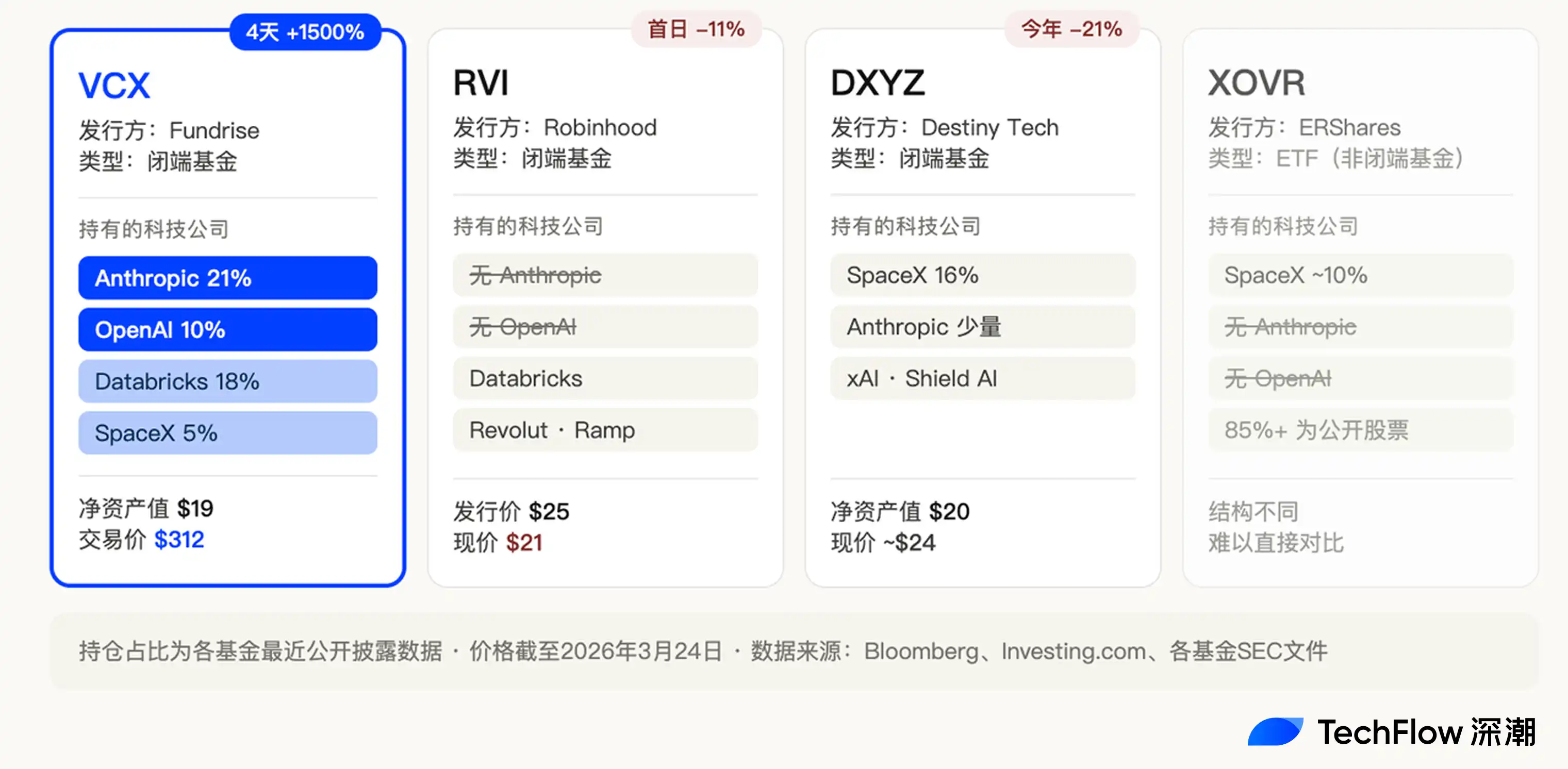

Robinhood created a fund called RVI, listed on March 6 with an issue price of $25. Its holdings include Databricks, Revolut, Ramp—all good private companies. It fell 11% on its first day, closing at $21.

Destiny Tech100, ticker DXYZ, listed in 2024, is a pioneer in this space. Heavily weighted in SpaceX, with a 16% holding. It only added a small exposure to Anthropic indirectly in February of this year. Its price is now hovering around $24.

There's also XOVR, the first ETF approved to directly hold shares of private companies, with SpaceX making up about 21%.

Four funds, similar structures, similar concepts, all trading on the same exchange. But their fates are completely different.

VCX rose 1500% in four days. RVI broke issue price on its first day. DXYZ is lukewarm.

VCX holds 21% Anthropic and 10% OpenAI. RVI's holdings include neither Anthropic nor OpenAI. DXYZ's exposure to Anthropic was added recently and is very small.

This shows that, at least for now, the market isn't chasing "shares in private companies." The market is chasing Anthropic.

Whoever is closest to them is valuable.

That's where Robinhood's RVI lost out. Databricks and Revolut are certainly good companies, but clearly, right now, they are not the name people are willing to pay a 16x premium for.

Shadows also have an expiration date

What are those who bought VCX at $312 betting on?

They are betting that before the door opens, someone else will be willing to pay an even higher price for the privilege of not being able to get Anthropic directly.

However, this door won't stay closed forever.

VCX has over 100,000 investors, and the vast majority of their shares are locked for six months. The lock-up period ends on September 19. At that time, a large number of shares will flood the market, and supply will change overnight from极度稀缺 (extremely scarce) to abundant.

The reason VCX can sell at a 16x premium is half because it contains Anthropic, and half perhaps because so few shares are available to sell. Once the lock-up period ends, the second condition disappears.

There is an even bigger variable.

Anthropic, OpenAI, SpaceX—all three are rumored to be targeting IPOs in the second half of 2026 to 2027. Anthropic just raised $30 billion last month at a $380 billion valuation and has already hired Silicon Valley law firm Wilson Sonsini for IPO preparations. SpaceX's CFO has been communicating with investors about an IPO since the end of last year, targeting mid-year.

Once the real thing goes public, the shadow becomes worthless.

If you can directly type Anthropic's stock ticker into your brokerage search box, why would you pay a 16x premium for a fund that indirectly holds it?

For example, DXYZ also surged wildly when it first listed in 2024, but as SpaceX's IPO was delayed, the hype faded, and its price fell by more than half from its high.

So, VCX investors are experiencing a classic countdown.

What they bought for 16 times the price is not shares in Anthropic, but a ticket with an expiration date. When the door opens depends on when Anthropic decides to go public.

Before that, the premium is maintained by scarcity; after that, the premium goes to zero.

But the phenomenon of shadow stocks itself is not accidental.

Every technological wave creates the same anxiety: you can't buy the most important companies. In the 2000s, before Google's IPO, Goldman Sachs employees fought fiercely internally for allocations. In 2020, it was SpaceX, and secondary market intermediaries in Silicon Valley became the most sought-after connections overnight.

Now it's AI's turn.

And this time the anxiety is deeper. Anthropic and OpenAI may not be profitable now, but they are rewriting the rules. Because of AI's impact, SaaS stocks crashed, security stocks crashed, and IBM lost $31 billion in a day.

Investors see not just "this company is very profitable," but "if I'm not on its side, I might be on the side it runs over."

The 16x premium of VCX isn't pricing just a fund; it's pricing this anxiety itself.

The ticket will expire, the premium will fade. But as long as AI keeps accelerating, as long as the most valuable companies keep their doors closed, there will be people willing to pay irrational prices for the shadow.

Not because the shadow is worth that much, but because the feeling of being locked out is too expensive.