Author: C Labs Crypto Watch

According to unaudited financial reports disclosed by the Financial Times, Telegram, known as the "dark version of WeChat," achieved revenue of $870 million in the first half of 2025, a 65% year-over-year increase, showing a significant leap compared to $525 million in the same period of 2024.

From a "revenue growth" perspective, this is a quite impressive growth curve.

However, the problem lies in the profit side. Telegram recorded a net loss of over $220 million in the first half of 2025, compared to a net profit of $334 million in the same period last year.

The loss did not stem from a collapse in the main business but was due to a significant decline in the value of Toncoin (TON) held by the company in 2025, leading to a write-down of related assets.

PART 01: Telegram's Development History

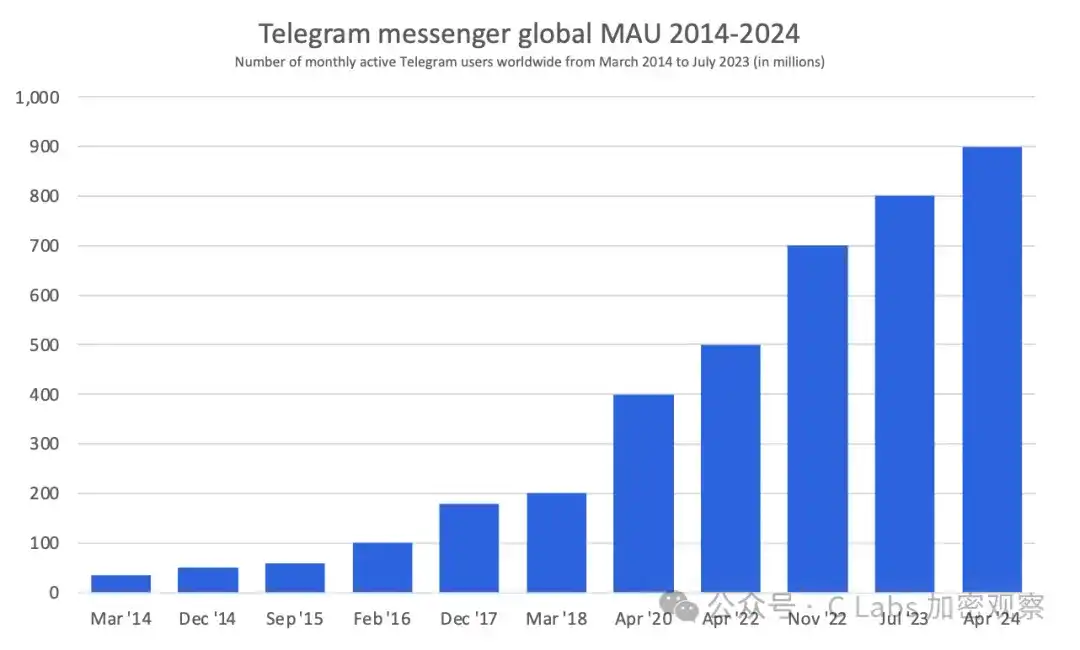

Telegram was founded in 2013 and is one of the world's most important instant messaging platforms.

As of 2025, Telegram's monthly active users have exceeded 900 million, covering Europe, the Middle East, South America, and emerging markets, making it one of the fastest-growing social applications globally.

For crypto users, Telegram has become the de facto "public discussion layer" of the crypto industry: a large number of exchange announcements, project governance, airdrop information, OTC trading, and on-chain communities use Telegram as their core platform.

This gives it the dual attributes of a social platform and financial information infrastructure.

PART 02: IPO Plans Shelved

Although Telegram announced preparations for an IPO, the practical obstacle is that its founder, Pavel Durov, is still under investigation in France (Breaking! TG Founder Arrested, TON Price Plummets).

Telegram has clearly stated that it will not proceed with the listing until related compliance issues are clearer.

Fortunately, Telegram is not short of capital support. In May 2025, the company completed a $1.7 billion convertible bond financing, backed by top institutions including BlackRock and Mubadala.

PART 03: Telegram's Relationship with TON

The relationship between Telegram and TON is also complex.

In 2017, Telegram launched the blockchain project TON (Telegram Open Network), aiming to embed a payment system into the messaging app, and raised approximately $1.7 billion in 2018. However, in 2019, it was forced to halt the project after the SEC deemed it an unregistered securities offering. Telegram settled with regulators and exited the project in 2020.

Subsequently, TON was reborn as a community public chain, and Telegram re-engaged with it in a "non-official but deeply integrated" manner, which saw significant growth in 2024.

Unfortunately, in 2024, after founder Durov was arrested, the rapid progress came to an abrupt halt (TON Chain Crashed? No New Blocks for a Long Time).

Most of the once-popular TON ecosystem projects have now faded, with token prices generally down over 70%:

However, according to the latest financial report, the relationship between Telegram and TON has already gone beyond "official support for a public chain."

Significant Proportion of TON-Related Revenue

The financials show that about one-third of Telegram's revenue (approximately $300 million) comes from exclusive agreements related to TON, including wallet integration, payment functions, and ecosystem collaboration.

At the same time, Telegram is also one of the most significant sources of TON circulation, having sold over $450 million worth of TON since 2025, accounting for about 10% of TON's current market value.

This means that selling coins is Telegram's main business, and simultaneously, Telegram is the biggest whale dumping TON!